The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

Barclays has cut its Brent crude price outlook, citing faster-than-expected output hikes by OPEC+. The bank now sees Brent averaging $66 per barrel in 2025 (down $4) and $60 in 2026 (down $2).

Key takeaways:

OPEC+ ramped up output by 411,000 bpd in June, its second consecutive month of aggressive supply increases.

Saudi Arabia is pressuring under-compliant members like Iraq and Kazakhstan to meet quotas by accelerating production growth.

Barclays expects OPEC+ to fully unwind its voluntary cuts by October 2025 — a year earlier than previously projected.

The bank also downgraded U.S. crude production forecasts, seeing output falling by 100,000 bpd in 2025 and 150,000 bpd in 2026.

Brent crude dropped over $2 in early Monday trade, falling to $59.20 as of 0250 GMT.

Barclays says the faster supply growth could modestly loosen global oil market balances, adding pressure to prices.

Earlier:

***

For interest, and noting this is not what the market is thinking right now, some analysts are arguing that OPEC’s decision to increase oil production is not overly bearish, the main reason being that most of the increase is in the production ceiling, not

production … and is only on paper. It, in effect, legitimises overproduction

that is already in the market.

***

Oil update:

as a ps. Morgan Stanley lowered its oil price forecasts earlier also, cuts it Brent forecast by US$5 / barrel for 2025

May 5, 2025 – Written by Tim Boyer

STORY LINK Pound to Dollar Forecast: Consolation Now, Longer-Term 1.43

Bank of America forecasts that the Pound to Dollar exchange rate (GBP/USD) will strengthen to 1.43 at the end of 2025 with a further advance to 1.54 at the end of next year.

HSBC has lowered its dollar outlook with the end-2025 dollar forecast at 1.32 from 1.23 previously.

GBP/USD hit 3-year highs just below 1.3450 during the week before a retreat to just below 1.3300.

Interest rate decisions will be a key element in the week ahead.

There are strong expectations that the Bank of England will cut interest rates by 25 basis points to 4.25% with expectations that a minority of MPC members will vote for a larger cut. Guidance from the bank will be crucial for the Pound.

Rabobank noted the possibility of dovish guidance, but added; “Given the potential for a hot April CPI print, the MPC may prefer to keep its options open and stick to its current guidance of careful and careful cuts. We therefore hesitate to call for a follow-up cut in June, but a cold CPI print could change that.”

According to ING; “The Bank of England is poised to cut rates at its 8 May meeting, and markets are pricing a faster pace of easing thereafter. We’re less convinced the Bank will deviate from its once-per-quarter cutting rhythm, but we do think it could cut rates to a lower level than investors are currently expecting.”

![]()

Rabobank is wary over overall UK fundamentals; “The UK’s current account deficit can leave GBP exposed when UK fundamentals are weak. Currently, soft growth and a high level of indebtedness in the UK will not endear the pound to investors.”

The bank also has a 12-month GBP/USD forecast of 1.32.

The Federal Reserve is not expected to cut interest rates on Wednesday with the Fed Funds rate held at 4.50%.

Markets see no real chance of a cut at this meeting while there is a 60% chance of a June move.

There will be no updated forecasts at this meeting.

Guidance from Chair Powell will be crucial for the dollar, especially given the strong political pressure from the US Administration.

The US labour-market data was slightly stronger than expected with an increase in non-farm payrolls of 177,000 for April and unemployment held at 4.2%.

![]()

GDP, however, contracted at an annualised rate of 0.3% for the first quarter while consumer confidence dipped further to 5-year lows with the expectations element at a 14-year low.

The extent of dollar confidence will be a crucial element with a focus on trade, Fed independence and capital flows.

HSBC commented; “There are questions about its structural properties that we have not had to take more seriously for some time. We do not believe there is enough evidence to fully embrace those concerns but we cannot discount them either. Putting these together tells us that the DXY will be in a softer position over the coming quarters.

It added; “We could see some reweighting back towards our previous USD framework that laid the grounds for a healthier USD. For now though, we are sailing away from the currency.”

SocGen notes the importance of data; “The lag between policy announcements and their impact on the US economy is however significant and the fall in the dollar (and US equity indices) is now pausing/correcting. It will resume when/if economic data confirm market fears that the US is in for a period of slower growth and higher inflation.”

Standard Chartered commented; Our baseline expectation is that the USD will be slightly weaker versus current spot but basically stable through year-end. The US administration seems to be making its most determined effort in months to reassure markets on tariffs and other policies. But even after the administration’s positive announcements on tariff progress and equity market gains, the USD has not traded very firmly.”

It added; “This makes us think that the adjustment of USD positions is continuing and could take the USD a bit lower.”

The bank has increased its end-2025 GBP/USD forecast to 1.35 from 1.26.

International Money Transfer? Ask our resident FX expert a money transfer question or try John’s new, free, no-obligation personal service! ,where he helps every step of the way,

ensuring you get the best exchange rates on your currency requirements.

The Gold price (XAU/USD) trades in positive territory near $3,245 during the early Asian session on Monday. The renewed concerns over the US recession and US-China trade relations provide some support to safe-haven assets like Gold. The US ISM Services Purchasing Managers Index (PMI) for April will be in the spotlight later on Monday.

While the Chinese Commerce Ministry indicated Beijing was considering an offer from the US to hold talks over US President Donald Trump’s 145% tariffs, the two sides still seem far apart. Trump avoided answering the question if there will be trade deals this week, saying there ‘could’ be. The uncertainty surrounding tariff boosts the safe-haven flows, benefiting the precious metal.

The rising bets that the Fed will cut its interest rate in June raise non-yielding bullion’s appeal. “The labor report leaves little doubt that the FOMC will keep rates on hold this week, and the bar for cutting is now even higher for June,” said Michael Feroli, head of U.S. economics at JPMorgan.

Nonfarm Payrolls (NFP) in the United States (US) rose by 177K in April, according to the US Bureau of Labor Statistics (BLS) on Friday. This figure followed the 185K increase (revised from 228K) seen in March and came in above the market consensus of 130K. Additionally, the Unemployment Rate remained unchanged at 4.2% in April, as expected, while the Average Hourly Earnings held steady at 3.8% YoY in the same reported period.

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

On the other hand, improved market sentiment and a risk-on trade could drag the yellow metal lower and lead to some profit-taking in Gold’s safe-haven. Trump eased tensions with the US Fed, saying that he will not remove Jerome Powell as Fed Board Chairman before his term ends in May 2026. Nonetheless, Trump reiterated his belief that the Fed should cut interest rates at some point

The EUR/USD pair stayed under mild selling pressure for the second consecutive week, but settled on Friday at around 1.1350, pretty much unchanged from the opening. Investors are still wary about the US Dollar (USD) given the White House’s tariffs policy potential effects on the local economy.

Additionally, United States (US) data released in the last few days indicated a slowing performance throughout the first quarter of the year, also a result of trade-war concerns. On the contrary, European Union (EU) macroeconomic figures were unimpressive but painted a better picture.

As the week comes to an end, investors shift the focus to global trade developments and the upcoming Federal Reserve (Fed) monetary policy announcement.

The EU released the April Economic Sentiment Indicator, which contracted to 93.6 from 95.00 in March. Additionally, the Union released the preliminary estimate of the Q1 Gross Domestic Product (GDP), indicating the economy grew by 1.2% on a yearly basis and by 0.4% in the quarter, beating expectations of 1.0% and 0.2%, respectively. Finally, the Harmonized Index of Consumer Prices (HICP) rose by more than anticipated in April, according to preliminary estimates, up 2.2% year-on-year (YoY) vs the 2.1% expected.

Meanwhile, Germany released March Retail Sales, down on a monthly basis by 0.2%, better than the -0.4% anticipated by market players. The German Q1 (GDP) showed the economy grew 0.2% in the quarter, according to preliminary estimates. The figure matched expectations, while improving from the Q4 2024 reading of -0.2%. Inflation in the country, as measured by the HICP, increased by 2.2% year-on-year (YoY), down from the previous 2.3% but above the 2.1% expected.

Tepid EU data kept the door open for additional rate cuts. European Central Bank (ECB) officials delivered dovish messages, supporting the case for another 25 basis points (bps) rate cut when they meet in June.

Among others, ECB policymaker Olli Rehn stated on Monday that the central bank may need to lower interest rates below the neutral level to support the economy, given materializing downside risks. He even called for larger interest rate cuts. Also, ECB Philip Lane noted he would not pre-commit to any path and said the growth forecast would see only a moderate markdown.

A fragile economy and persistent trade tensions leave no room for anything other than further cuts.

Unimpressive US data limited USD advances despite the de-escalation of global trade tensions.

Consumer Confidence, as measured by CB, fell to 86 in April, its lowest since October 2021. Also, the preliminary estimate of the US Q1 Gross Domestic Product (GDP) also missed expectations, as the economy contracted at an annualized pace of 0.3% against the anticipated 0.4% expansion, and sharply down from the previous 2.4%. The April ISM Manufacturing Purchasing Managers’ Index (PMI), on the contrary, posted 48.7, down from the 49 posted in March, but better than the 48 expected.

Inflation in the US, as measured by the change in the Personal Consumption Expenditures (PCE) Price Index, edged lower to 2.3% on a yearly basis in March from 2.5% in February. The figure missed expectations of 2.2%. The core annual PCE Price Index rose 2.6%, down from the 3% increase reported in February and in line with analysts’ estimates.

Employment-related figures were tepid, although the April Nonfarm Payrolls (NFP) report brought a positive surprise ahead of the weekly close.

Earlier in the week, the US released the April ADP Employment Change report, which showed that the private sector added measly 62K new job positions, much worse than the 108K expected, while below the previous 147K. Also the number of job openings in the country on the last business day of March stood at 7.19 million, as reported in the Job Openings and Labor Turnover Survey (JOLTS), easing from the previous 7.48 million openings (revised from 7.56 million) reported in February and below the market expectation of 7.5 million. Finally, Initial Jobless Claims for the week ended April 26 rose by 241K, worse than the 224K anticipated and the previous weekly figure of 223K.

On Friday, the NFP showed the country added 177K new job positions in April, surpassing the expected 130K and not far from the 185K posted in March. The Unemployment Rate held steady at 4.2% as expected, while annual wage inflation, as measured by the change in the Average Hourly Earnings, held steady at 3.8%, below the 3.9% expected.

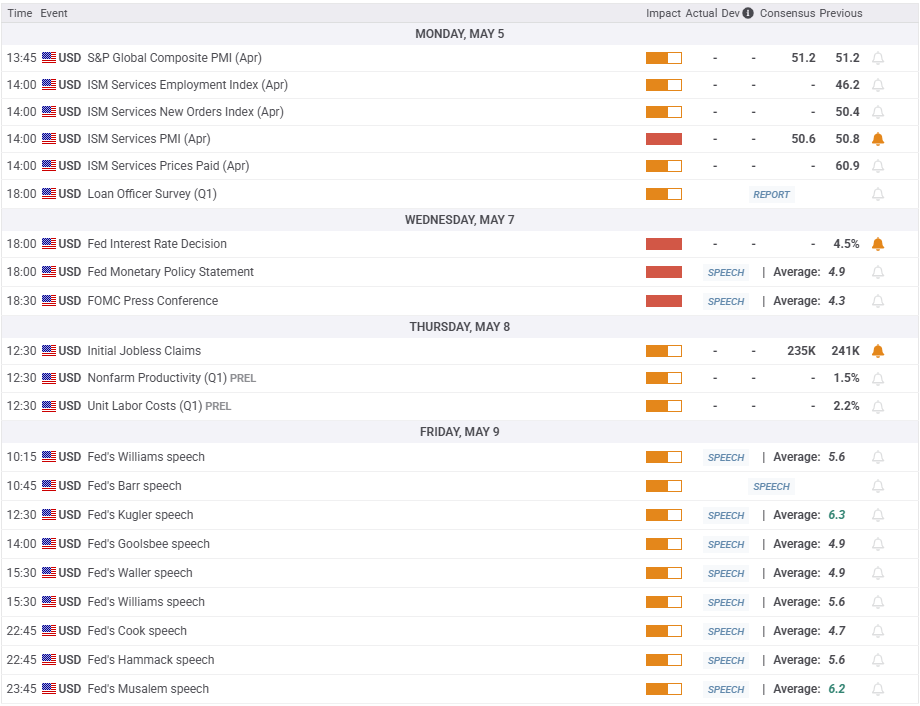

The macroeconomic calendar has little relevant to offer in the upcoming days. The US will release the April Services PMI, foreseen at 50.6, down from the March reading of 50.8. As for the EU, the focus will be on Germany Factory Orders, seen increasing by 2.2% in March, and EU Retail Sales for the same period.

The Fed will gather all the attention, announcing the monetary policy decision on Wednesday. Fed officials are widely anticipated to keep the benchmark interest rate on hold this time, floating between 4.25% and 4.50%. Uncertainty related to trade tensions translates into potentially higher inflation coupled with a slowdown in economic activity, forcing policymakers to stay put ahead of a clearer picture emerges.

Chairman Jerome Powell is expected to repeat the need to wait and see, with the focus on progress towards the 2% inflation goal. Questions about his relationship with President Donald Trump within the press conference are likely, yet Powell will likely dodge those as usual.

In the meantime, global trade tensions continue, impacting the market’s mood. Headlines were mostly discouraging throughout the first half of the week, as headlines coming from China indicated no negotiations were underway. As days went by, back and forth between Washington and Beijing continued, with both sides waiting for the opposite one to take the first step, something that has not yet happened.

Still, comments from Trump pointing to ongoing negotiations with other major trade counterparts brought some relief to financial markets. On Thursday, US President Trump noted progress on talks with some Asian countries, including India and Japan. Regarding China, Trump stated that there’s a “very good” chance of making a deal with China, yet added that any deal with Beijing has to be in US terms. Meanwhile, a Beijing-backed outlet reported that United States officials have contacted their Chinese counterparts for talks.

Finally, White House trade advisor Peter Navarro down-talked data, saying, “I got to say just one thing about today’s news, that’s the best negative print I have ever seen in my life,” while saying he likes “where we’re at now.”

The mood improved ahead of the weekly close thanks to the optimism related to such headlines.

The weekly chart for the EUR/USD pair shows extreme conditions continue to recede, while the bearish potential seems well-limited. Technical indicators retreated from their recent highs, but remain within overbought territory, with the Relative Strength Index (RSI) indicator consolidating around 70. At the same time, the pair develops above all its moving averages, with a bullish 20 Simple Moving Average (SMA) extending its advance below the 100 and 200 SMAs. The longer one stands at around 1.0830, which is too far away to be considered a relevant support, yet at the same time, it reflects EUR/USD bullish momentum.

The daily chart shows EUR/USD bounced from a bullish 20 SMA currently at around 1.1300. The 100 and 200 SMAs grind north over 500 pips below the current level, in line with the dominant bullish strength. Finally, technical indicators are stuck around their midlines, barely bouncing while losing the bearish strength from the previous sessions. Overall, it seems the downward correction is complete and EUR/USD may soon resume its upward strength.

Immediate resistance can be found at around 1.1400, followed by the 1.1470 region, ahead of the yearly peak at 1.1573. A clear break below the latter should see EUR/USD extending gains well beyond the 1.1600 mark. Support, on the other hand, comes at around 1.1300, followed by the 1.1260 price zone. A break below the latter could open the door for a decline towards the 1.1160/70 price zone.

The Federal Reserve (Fed) deliberates on monetary policy and makes a decision on interest rates at eight pre-scheduled meetings per year. It has two mandates: to keep inflation at 2%, and to maintain full employment. Its main tool for achieving this is by setting interest rates – both at which it lends to banks and banks lend to each other. If it decides to hike rates, the US Dollar (USD) tends to strengthen as it attracts more foreign capital inflows. If it cuts rates, it tends to weaken the USD as capital drains out to countries offering higher returns. If rates are left unchanged, attention turns to the tone of the Federal Open Market Committee (FOMC) statement, and whether it is hawkish (expectant of higher future interest rates), or dovish (expectant of lower future rates).

Next release:

Wed May 07, 2025 18:00

Frequency:

Irregular

Consensus:

–

Previous:

4.5%

Source:

Federal Reserve

Generally speaking, a trade war is an economic conflict between two or more countries due to extreme protectionism on one end. It implies the creation of trade barriers, such as tariffs, which result in counter-barriers, escalating import costs, and hence the cost of living.

An economic conflict between the United States (US) and China began early in 2018, when President Donald Trump set trade barriers on China, claiming unfair commercial practices and intellectual property theft from the Asian giant. China took retaliatory action, imposing tariffs on multiple US goods, such as automobiles and soybeans. Tensions escalated until the two countries signed the US-China Phase One trade deal in January 2020. The agreement required structural reforms and other changes to China’s economic and trade regime and pretended to restore stability and trust between the two nations. However, the Coronavirus pandemic took the focus out of the conflict. Yet, it is worth mentioning that President Joe Biden, who took office after Trump, kept tariffs in place and even added some additional levies.

The return of Donald Trump to the White House as the 47th US President has sparked a fresh wave of tensions between the two countries. During the 2024 election campaign, Trump pledged to impose 60% tariffs on China once he returned to office, which he did on January 20, 2025. With Trump back, the US-China trade war is meant to resume where it was left, with tit-for-tat policies affecting the global economic landscape amid disruptions in global supply chains, resulting in a reduction in spending, particularly investment, and directly feeding into the Consumer Price Index inflation.

Barclays has cut its Brent crude price outlook, citing faster-than-expected output hikes by OPEC+. The bank now sees Brent averaging $66 per barrel in 2025 (down $4) and $60 in 2026 (down $2).

Key takeaways:

OPEC+ ramped up output by 411,000 bpd in June, its second consecutive month of aggressive supply increases.

Saudi Arabia is pressuring under-compliant members like Iraq and Kazakhstan to meet quotas by accelerating production growth.

Barclays expects OPEC+ to fully unwind its voluntary cuts by October 2025 — a year earlier than previously projected.

The bank also downgraded U.S. crude production forecasts, seeing output falling by 100,000 bpd in 2025 and 150,000 bpd in 2026.

Brent crude dropped over $2 in early Monday trade, falling to $59.20 as of 0250 GMT.

Barclays says the faster supply growth could modestly loosen global oil market balances, adding pressure to prices.

Earlier:

***

For interest, and noting this is not what the market is thinking right now, some analysts are arguing that OPEC’s decision to increase oil production is not overly bearish, the main reason being that most of the increase is in the production ceiling, not production … and is only on paper. It, in effect, legitimises overproduction that is already in the market.

***

Oil update:

as a ps. Morgan Stanley lowered its oil price forecasts earlier also, cuts it Brent forecast by US$5 / barrel for 2025

Crude oil markets took a fresh hit this weekend after OPEC+ stunned traders by announcing a larger-than-expected output increase for June. In a virtual meeting on Saturday, key producers led by Saudi Arabia and Russia agreed to raise collective output by 411,000 barrels per day (bpd), nearly triple the volume originally scheduled.

The move follows a similar surge announced for May and signals a sharp reversal from OPEC+ efforts to defend oil prices. Instead, Riyadh appears to be embracing a low-price strategy, aiming to discipline overproducing members like Kazakhstan and Iraq. Both nations have repeatedly exceeded their quotas, with Kazakhstan surpassing its March target by 422,000 bpd.

“OPEC+ has just thrown a bombshell to the oil market,” Jorge Leon of Rystad Energy told Bloomberg. “With this move, Saudi Arabia is seeking to punish lack of compliance and also ingratiate itself with President Trump.”

President Donald Trump has loudly demanded lower oil prices, and with fresh tariffs rattling global markets, OPEC+ appears to be aligning with Washington’s inflation-fighting agenda. Trump is set to visit the Middle East this month, and closer energy cooperation may be on the table.

Oil prices had already been under pressure, with Brent trading near $61 a barrel on Friday, a four-year low. The OPEC+ decision sent prices tumbling another 6%, compounding bearish sentiment triggered by trade war fears and weakening economic data.

Goldman Sachs responded by slashing its December 2025 oil forecast by $5 to $66 for Brent and $62 for WTI, citing both rising OPEC+ supply and Trump’s tariff barrage. “We no longer forecast a price range,” Goldman said, “because price volatility is likely to stay elevated on higher recession risk.”

Standard Chartered joined the chorus of bearish revisions, slashing its 2025 Brent forecast by $16 to $61 a barrel, and trimming its 2026 outlook to $78. The bank warned that the Trump administration’s tariff-heavy approach is fueling recession fears and eroding market confidence—especially after a downbeat U.S. economic report this week.

JPMorgan also raised its global recession odds to 60% for the year, while S&P Global warned that oil demand growth could drop by as much as 500,000 bpd.

OPEC+ justified the output hike by citing “continuing healthy market fundamentals,” though many see the move as an effort to assert market share and enforce compliance. Analysts like Helima Croft argue that by opening the taps, Saudi Arabia is reasserting control over rogue members while signaling readiness to let prices fall to discipline the market.

The eight members behind the increase—Saudi Arabia, Russia, Iraq, the UAE, Kuwait, Kazakhstan, Algeria, and Oman—will reassess in June. But for now, the message is clear: OPEC+ is no longer defending high prices, and oil markets should prepare for more volatility ahead.

By Tom Kool for Oilprice.com

More Top Reads From Oilprice.com

At the same time, U.S. economic signals painted a mixed picture: GDP shrank by 0.3% in Q1 and core PCE was flat in March, while jobless claims rose to 241,000. Yet April’s jobs report offered just enough resilience to keep the Fed on the sidelines for now, limiting gold’s near-term upside.

This week, all attention turns to the Federal Reserve. The FOMC is expected to hold rates steady on Wednesday, but Chair Powell’s press conference may carry outsized impact. Political pressure has intensified, with President Trump and Treasury Secretary Bessent openly criticizing the Fed and urging preemptive cuts. However, with Friday’s jobs report showing no clear labor market deterioration, Powell may strike a cautious tone—potentially reinforcing higher-for-longer rate expectations unless inflation or employment data worsen.

Gold enters the week with a bearish tilt. A firmer dollar, muted physical demand, and reduced expectations for near-term Fed cuts are all headwinds. Unless Powell surprises with dovish guidance, bullion is likely to remain under pressure.

The broader macro picture—rising fiscal stress, policy uncertainty, and central bank accumulation—still supports long-term upside. But near-term, a lack of fresh catalysts favors sellers unless Fed rhetoric or incoming data reignites rate cut speculation. Traders should brace for volatility around Wednesday’s FOMC announcement and Powell’s post-meeting remarks.

More Information in our Economic Calendar.

The GBP/USD weekly forecast is slightly bearish as strong US labor sector validates the Fed’s cautious tone.

The GBP/USD price ended the week down after climbing to new highs. Initially, the pound rallied against the dollar amid downbeat US economic data. However, this changed after robust employment figures at the end of the week.

-Are you looking for forex robots? Check our detailed guide-

US figures on job vacancies, pirate employment and jobless claims pointed to a faster-than-expected economic decline. However, business activity in the manufacturing sector was better than expected. Moreover, the nonfarm payrolls report revealed 177,000 new jobs in April compared to estimates of 138,000.

Next week, market participants will focus on the Fed and Bank of England policy meetings. Economists expect the Fed to keep interest rates unchanged, while the Bank of England will likely cut rates by 25-bps.

The Fed has maintained a cautious tone, with Powell saying there was no hurry to cut interest rates. However, recent downbeat economic data might push the central bank in June. Meanwhile, the BoE is aware of the likely impacts of Trump’s tariffs. Weaker global and UK growth will likely push policymakers to consider a faster easing cycle.

On the technical side, the GBP/USD price has paused after reaching the 1.3401 key resistance level. Moreover, the price trades above the 22-SMA and the RSI is above 50, suggesting a bullish bias. GBP/USD has maintained a bullish trend, making higher highs and lows. At the same time, the price has respected a trendline as support.

-Are you looking for the best CFD broker? Check our detailed guide-

The most recent swing started at the support trendline and the 1.2702 level. However, the move slowed near the 1.3401 level. Bulls tried twice to break above the level but failed. Meanwhile, the RSI made a slight bearish divergence, signaling a looming pullback.

The price might be ready to retest the 22-SMA. A deeper retreat would retest the support trendline. The bullish bias will remain if the price stays above the SMA or the trendline. Meanwhile, the uptrend will continue with a break above the 1.3401 resistance.

Looking to trade forex now? Invest at eToro!

67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

The Pound Sterling (GBP) witnessed a downside correction against the US Dollar (USD) after the GBP/USD pair faced rejection again near the 1.3450 barrier.

King Dollar regained its throne, booking the third weekly gain, due to receding tariff war fears and optimism emerging from potential trade deals between the United States (US) and its major Asian trading partners.

US President Donald Trump and some of his colleagues stuck to their rhetoric that trade negotiations continued with China even though Beijing dismissed such talks. Trump said during the week that he has “potential” trade deals with India, South Korea and Japan and that there is a very good chance of reaching an agreement with China.

China eventually confirmed in the latter part of the week, with the Chinese Commerce Ministry stating that “the US has recently sent messages to China through relevant parties, hoping to start talks with China. China is currently evaluating this.”

Optimism on the trade front allayed fears of a likely slowdown in the US economic growth, keeping the USD recovery intact. The first look of the US annualized Gross Domestic Product (GDP) showed on Wednesday that the US economy contracted by 0.3% in the first quarter of 2025 as US firms frontloaded to get ahead of the US levies, resulting in an import surge.

However, Thursday’s ISM Manufacturing PMI eased US growth concerns. The index fell to 48.7 in April from 49.0 in March, against expectations for a bigger fall to 48.

Therefore, the sustained USD demand remained the primary driver behind the GBP/USD pair’s moves as the Pound Sterling finally gave in to the Greenback’s resurgence. The pair hit a fresh three-year high at 1.3445 at the start of the week before setting off a correction to near 1.3250 heading into the release of the US employment report on Friday.

The US Bureau of Labor Statistics (BLS) reported that Nonfarm payrolls (NFP) rose by 177,000 in April, surpassing the market expectation of 130,000. In this period, the Unemployment Rate held steady at 4.2% and annual wage inflation, as measured by the change in the Average Hourly Earnings, remained unchanged at 3.8%. GBP/USD struggled to gain traction after the US labor market data and remained in the lower half of its weekly range heading into the weekend.

Following a US economic data-dominated week, the upcoming week is relatively light, notwithstanding the Fed and BoE monetary policy decisions.

On Monday, the US ISM Services PMI will be of note for the major as the UK markets will remain closed in observance of May Day. Tuesday lacks any top-tier UK or US macro news, so all eyes turn toward Wednesday’s Fed interest rate decision.

The Fed is widely expected to hold rates following the May policy meeting. Still, Chairman Jerome Powell’s words on the potential impact of US tariffs on the economic and inflation outlook will hold the key and impact the USD performance across the board.

The BoE will steal the spotlight on ‘Super Thursday’as the Bank’s Monetary Policy Report (MPR) and Governor Andrew Bailey’s press conference will throw fresh hints on the timing of the next interest rate cut.

Later that day, the US will publish its weekly Jobless Claims data.

BoE Governor Bailey will make his second public appearance of the week on Friday, speaking at the Reykjavík Economic Conference in Iceland. Fed policymakers will also return to the rostrum after the ‘blackout period’.

That said, potential trade deals between the US and its major trading partners and developments on the tariff front will continue playing a pivotal role in the week ahead.

Amid a Golden Cross and a bullish 14-day Relative Strength Index (RSI) on the daily chart, risks remain skewed to the upside for the GBP/USD pair in the short term.

The 50-day Simple Moving Average (SMA) crossed above the 200-day SMA on a daily closing basis on April 17, providing conviction to the bullish streak.

Meanwhile, the 14-day Relative Strength Index (RSI) has turned north while above the midline, currently near 59.

The pair must close the week above the critical 1.3350 psychological barrier to negate the corrective bias. The next powerful resistance aligns at the three-year high of 1.3445.

Acceptance above that level will likely kick off a fresh uptrend toward the February 2022 high of 1.3644.

Alternatively, if the correction gathers steam, the 1.3200 round level will be tested initially, below which the immediate support of the 21-day SMA at 1.3184 will be tested.

A sustained break below the 21-day SMA will target the 50-day SMA at 1.3007, followed by the 200-day SMA at 1.2845.

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data.

Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates.

When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money.

When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP.

A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

West Texas Intermediate (WTI) Oil price advances on Friday, early in the European session. WTI trades at $59.21 per barrel, up from Thursday’s close at $58.71.

Brent Oil Exchange Rate (Brent crude) is also up, advancing from the $61.79 price posted on Thursday, and trading at $62.30.

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 12 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

Price Forecast: Can Dovish Fed Signals Reverse the Bearish Setup?")