Category: Forex News, News

Copper Near $12,000, Cobalt Quotas, UBS Downgrade, and Key 2026 Dates to Watch

Updated: 13 December 2025

Meta description: Glencore plc shares are being pulled between a red‑hot copper market, fresh operational guidance, Congo’s cobalt export quotas, and shifting analyst calls. Here’s the latest news, forecasts, and what could move GLEN in 2026.

Glencore plc stock is back in the spotlight heading into mid‑December, with investors trying to reconcile two very Glencore‑ish realities at once:

- Copper is ripping—fueled by AI data‑center power demand, grid upgrades, and tight supply.

- Operational execution still matters—and Glencore has trimmed near‑term copper guidance even as it talks up a long runway of growth.

Add in Congo’s restarted cobalt export system, a UBS downgrade on valuation, ongoing buybacks, and a freshly published 2026 corporate calendar, and you’ve got a busy setup for anyone tracking Glencore shares (LSE: GLEN; Reuters ticker GLEN.L). [1]

Glencore share price snapshot as of 13.12.2025

Because 13 December 2025 is a Saturday, the most recent full session is Friday, 12 December. Glencore shares were around the mid‑370p level at the latest close, after trading in a wide intraday band. Data providers show ~375.5p as the latest price, with the day’s range roughly 375.5p to 384.6p. [2]

That matters for context because several broker notes published this week peg price targets in the low‑400p to mid‑400p region—implying upside, but not unlimited room if the stock is already near the top of its recent range.

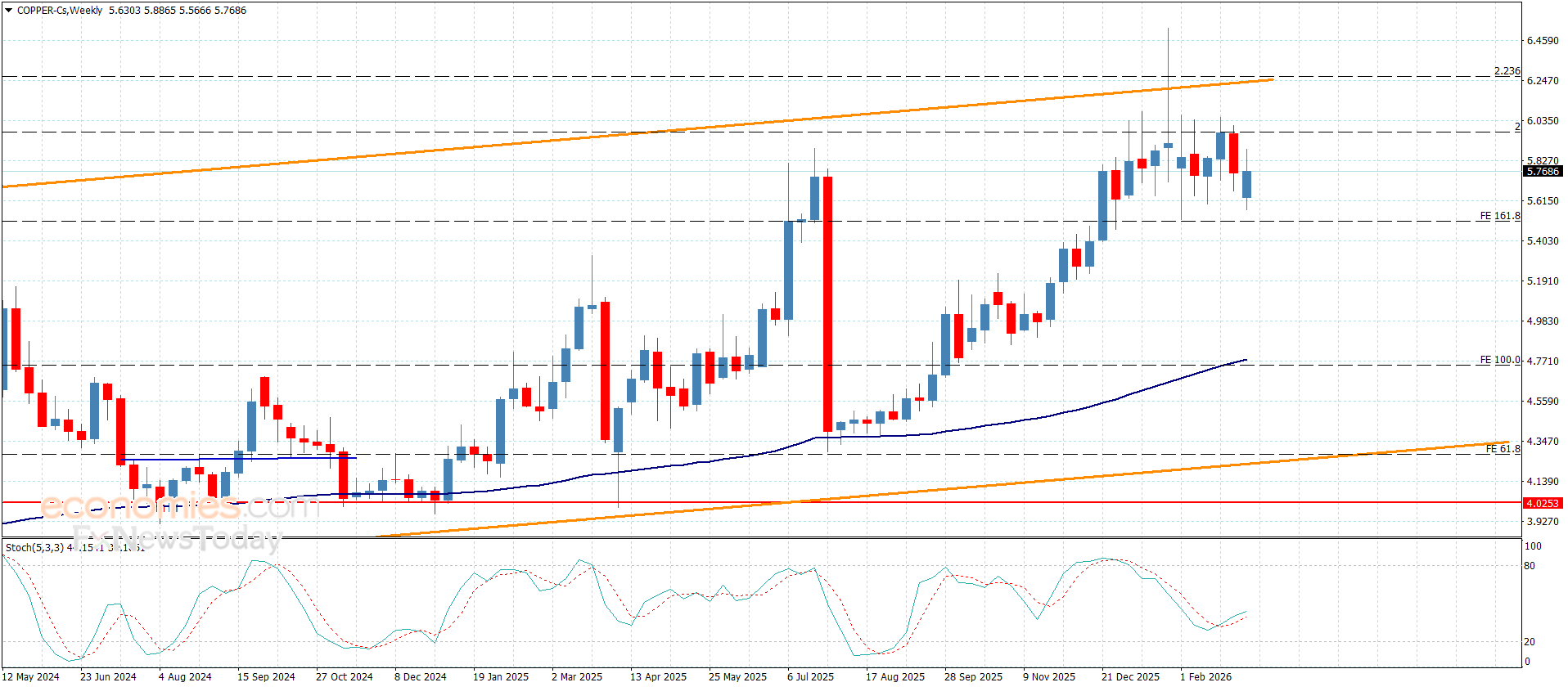

The macro tailwind: copper is nearing $12,000—and AI is part of the story

One of the biggest external drivers for Glencore right now is simply this: copper prices are flirting with $12,000 per metric ton, after a strong 2025 rally. Reuters points to a collision of tight supply and surging demand tied to electricity infrastructure, renewables, EVs—and increasingly AI data centers, which require massive, reliable power delivery (and therefore a lot of copper). [3]

Reuters also referenced expectations for market deficits (shortfalls) in copper in 2025 and 2026, alongside demand growth projections (including China and ex‑China demand). [4]

For Glencore investors, this is the core narrative: if copper is structurally tight for years, copper‑levered miners should benefit—and Glencore has been positioning itself to look more “copper-forward” over time.

Glencore’s big strategic message: a pathway to 1 million tonnes of copper by 2028—and 1.6 million by 2035

At its Capital Markets Day (3 December 2025), Glencore laid out a copper growth strategy that is ambitious even by mining’s long‑cycle standards:

- A pathway to ~1 million tonnes of annual copper production by the end of 2028

- A longer‑range target of ~1.6 million tonnes by 2035

- An expected 4% compound annual growth rate in “copper equivalent” production from 2026–2029, with copper production expected to grow faster over that period [5]

Management also emphasized that many projects are brownfield (expansions/optimizations at existing sites), which the market often prefers because it can be more capital efficient and less “bet-the-company” than a brand‑new mega‑mine. [6]

Glencore also used the event to reiterate the importance of its marketing (trading) business, describing it as continuing to perform well—an important point, because Glencore’s valuation is often a tug‑of‑war between “miner multiple” and “trading house multiple.” [7]

The catch: near-term copper guidance was cut for 2026—Collahuasi is the issue

Here’s where the plot thickens.

Despite long‑term optimism, Glencore has lowered its 2026 copper output expectations, with multiple industry sources attributing the change largely to challenges at Collahuasi in Chile (a joint venture). Fastmarkets reports Glencore guiding around ~840,000 tonnes of copper output in 2026 versus earlier plans near ~930,000 tonnes, citing lower grades and water constraints at Collahuasi. [8]

Crucially, that same reporting indicates Glencore expects a rebound: ~930,000 tonnes in 2027 and a return to the 1 million‑tonne level in 2028, assuming recovery and ramp-ups proceed as planned. [9]

Argus also frames it as short‑term pain for long‑term gain, noting the 2026 guidance cut and describing how development work at Collahuasi supports longer‑term output growth, even if it weighs on the immediate run‑rate. [10]

In plain English: Glencore wants to be a bigger copper story—but the bridge to that future still runs through operational bottlenecks.

Alumbrera restart in Argentina: a long-dated, but meaningful growth lever

Glencore also says it plans to restart operations at Alumbrera in Argentina, a mine that previously operated until 2018. Reuters reported that Glencore plans a restart of operations by the end of 2026, with production likely beginning in the first half of 2028. Reuters also noted Glencore pointing to Argentina’s investment/tax framework (including the RIGI incentive regime) and the outlook for copper and gold as part of the rationale. [11]

This is not a “next quarter” catalyst. It’s the kind of project markets typically discount heavily until the permitting, capex, and execution risk starts to compress. But it fits the broader thesis: Glencore is trying to stack future copper optionality while copper fundamentals look structurally supportive.

Chilean smelter partnership with Codelco: a downstream move with strategic logic

Glencore isn’t only talking mines. It is also stepping into strategic processing capacity discussions.

Reuters reported that Codelco and Glencore signed an initial agreement to collaborate on a smelter project in Chile’s Antofagasta region. Under the outline:

- Glencore would build a smelter with capacity around 1.5 million tonnes per year of concentrate

- Codelco would supply up to 800,000 tonnes annually for at least a decade

- Investment estimates cited by Reuters were $1.5–$2.0 billion

- Timeline: pre‑feasibility now; finalize agreement targeted for H1 2026; construction potentially 2030, operations 2032–2033 [12]

Why should equity investors care about something that far out?

Because processing is a geopolitical and industrial chokepoint. Reuters highlighted how treatment charges have been pressured in a tight concentrate market and how Chile wants to build more domestic smelting capacity rather than rely heavily on offshore processing. [13]

This is less about next week’s share price and more about where Glencore wants to sit in the copper value chain over the next decade.

Congo cobalt export quotas: Glencore ships first cargo under the new system

Glencore’s battery‑materials exposure also moved back onto center stage this week.

Reuters reported that Glencore became the first miner to export cobalt under the Democratic Republic of Congo’s new cobalt export quota system, sending a small initial shipment as a pilot. The system includes a 10% royalty, quarterly quotas, and (from 2026) an annual export cap. Reuters also reported that traders who originally expected shipments to restart earlier have pushed expectations out, with the first full‑sized cargo now expected later—Reuters mentioned April for the first full‑sized shipment expectation from Congo. [14]

Reuters also cited cobalt prices trading around $24/lb, sharply above earlier‑year lows, reflecting how export constraints can reprice the market fast. [15]

For Glencore stock, this is a double‑edged driver:

- Higher cobalt prices can be supportive for cobalt‑linked earnings.

- Regulatory friction and procedural ambiguity (royalties, compliance, approvals) inject uncertainty into volumes, timing, and working capital dynamics. [16]

Operational streamlining: Glencore cuts ~1,000 roles

On the cost and execution front, Reuters reported on 3 December that Glencore eliminated about 1,000 roles as it streamlines its industrial operating structure. [17]

Glencore’s own Capital Markets Day statement also flagged a streamlined operating structure with an emphasis on accountability and operating performance—so the staffing move lands as part of a broader “tighten the machine” narrative rather than a one‑off headline. [18]

Markets often like cost discipline, but they also ask the uncomfortable question: is this optimization, or is it a response to underlying operational strain? The answer usually shows up in production reports and unit costs over time.

South Africa: Eskom support discussions for Glencore-Merafe chrome venture

Reuters also reported that South Africa’s Eskom announced an agreement (MoU) with Samancor Chrome and the Glencore‑Merafe Chrome Venture, with the energy regulator reviewing an interim tariff adjustment. Reuters said the companies committed to suspend layoffs and restore part of furnace capacity if interim pricing relief is approved, while longer‑term solutions are explored. [19]

This matters because power pricing is often the difference between “cash machine” and “cash fire” in energy‑intensive processing assets.

Australia: strike risks reappear at Mount Isa and Townsville operations

On 13 December, Australian media reported that union members backed potential industrial action at Glencore’s Mount Isa copper smelter and Townsville refinery following wage negotiations. The reports reference the context of the A$600 million government support package announced earlier in 2025 and the sensitivity around pay, inflation, and operating viability. [20]

Investors should treat this as a site‑level risk variable: industrial action can pressure output and costs even when commodity prices are favorable.

Buybacks: Glencore continues to retire shares ahead of 2025 results

Glencore’s capital return program remains an important support pillar for the equity.

An RNS filing carried by the Financial Times market feed detailed an off‑market purchase of 6.4 million shares from UBS (dated 5 December 2025), with shares bought for cancellation. The RNS also stated this forms part of Glencore’s existing buyback programme, expected to be completed around the release of full‑year 2025 financial results in February 2026. [21]

In a market that’s increasingly allergic to vague promises, buybacks are a concrete signal: management is willing to convert cash into fewer shares outstanding.

Analyst forecasts and price targets: consensus still leans “Buy,” but valuation debates are heating up

The consensus view

According to Investing.com’s analyst snapshot:

- 18 analysts tracked

- Consensus rating: “Buy” (with 12 Buy and 6 Hold)

- Average 12‑month price target: ~417.8p

- Range of targets: roughly ~323p (low) to ~473p (high) [22]

Notable recent broker moves

- UBS: downgraded Glencore from Buy to Neutral, while raising its price target to £4.25 (425p), citing valuation concerns after the rally and arguing Glencore’s copper leverage is less direct than some investors assume. [23]

- Other firms listed on the Investing.com compilation show several Buy stances and targets in the mid‑400p range, including Barclays (Buy), Jefferies (Buy), and Citi (Buy), while JPMorgan is shown as Hold (per the same compilation). [24]

The interesting subtext: the debate isn’t “is copper bullish?” It’s “what’s the cleanest way to own that theme?” UBS’s framing suggests some strategists prefer pure‑play copper miners over diversified miners/traders when the market is paying up for copper exposure. [25]

The 2026 catalyst calendar: dates that can move GLEN quickly

Glencore published a 2026 corporate calendar that effectively puts “known volatility points” on the map. Key dates include:

- 29 January 2026: Production Report (12 months ended 31 Dec 2025) + Resources & Reserves report

- 18 February 2026: Preliminary Annual Results 2025

- 30 April 2026: Q1 Production Report

- 28 May 2026: AGM [26]

For many investors, the January production report is the first big checkpoint: it will help validate whether the “stronger second half” production narratives and guidance ranges are translating into real delivered tonnage.

What could drive Glencore stock next

Glencore is one of those companies where the share price can feel like it’s being steered by a committee of invisible forces. But heading into 2026, a few drivers look especially “load-bearing”:

1) Copper price direction (and deficit credibility)

If copper remains near cycle highs, Glencore benefits—but the market will still discount execution risk at assets like Collahuasi. [27]

2) Proof points on copper volume recovery

The bull case gets cleaner if 2026 looks like a temporary dip that reliably rebounds into 2027–2028 targets. [28]

3) Congo cobalt rulebook clarity

As quotas restart, the key question is whether process friction becomes “normal admin” or “persistent disruption.” [29]

4) Capital returns vs. reinvestment

Buybacks support the stock—but large future copper growth projects are capital hungry. Markets will watch how Glencore balances shareholder returns with risk‑managed growth and partnerships. [30]

5) Operational and labor stability

Australia wage disputes and energy‑intensive asset economics (South Africa) are reminders that mining isn’t only geology—it’s also politics, power prices, and people. [31]

Bottom line

As of 13 December 2025, Glencore plc stock sits at an interesting crossroads:

- The macro tape (copper strength, electrification, AI infrastructure demand) is supportive. [32]

- The company narrative is increasingly copper‑centric over the long haul—targeting 1 million tonnes by 2028 and 1.6 million by 2035. [33]

- The near‑term reality is messier: trimmed 2026 copper guidance, complex operating jurisdictions, and valuation debates that triggered at least one high‑profile downgrade. [34]

In other words, Glencore is doing what it always does: offering investors a bundle of upside themes wrapped in execution risk—like a gift box filled with copper wire and geopolitical paperwork.

References

1. www.reuters.com, 2. stockanalysis.com, 3. www.reuters.com, 4. www.reuters.com, 5. www.glencore.com, 6. www.glencore.com, 7. www.glencore.com, 8. www.fastmarkets.com, 9. www.fastmarkets.com, 10. www.argusmedia.com, 11. www.reuters.com, 12. www.reuters.com, 13. www.reuters.com, 14. www.reuters.com, 15. www.reuters.com, 16. www.reuters.com, 17. www.reuters.com, 18. www.glencore.com, 19. www.reuters.com, 20. www.couriermail.com.au, 21. markets.ft.com, 22. www.investing.com, 23. www.investing.com, 24. www.investing.com, 25. www.investing.com, 26. www.glencore.com, 27. www.reuters.com, 28. www.fastmarkets.com, 29. www.reuters.com, 30. markets.ft.com, 31. www.couriermail.com.au, 32. www.reuters.com, 33. www.glencore.com, 34. www.fastmarkets.com

Source link

Written by : Editorial team of BIPNs

Main team of content of bipns.com. Any type of content should be approved by us.

Share this article: