Category: Forex News, News

EUR/USD Forecast: US employment data to test US Dollar strength

The EUR/USD pair fell sharply for a second consecutive week, trading as low as 1.1324 before recovering towards the current 1.1410 price zone. The US Dollar Index (DXY) peaked at 101.80, its highest in little over a year, extending the positive momentum triggered by the Federal Reserve’s (Fed) hawkish hold and easing Middle East tensions. By the end of the week, the Greenback retains most of its gains, with the ongoing modest retracement seen as corrective.

War progress?

Over the last few days, the near-term inflationary outlook improved as progress in the Iran-United States (US) deal has sent Oil prices sharply lower. Still, the chaos from the previous three months is still spilling into global economies, and the Middle East war is far from a closed chapter. A sticky point is Iran’s nuclear power. The Memorandum of Understanding (MoU) signed a couple of weeks ago said that the US and Iran “have agreed to resolve the disposition of stockpiled, enriched material pursuant to a mechanism that will be mutually agreed upon,” yet the International Atomic Energy Agency (IAEA) has repeatedly called for verification to ensure Tehran does not develop nuclear weapons.

Another point of conflict is the passage through the Strait of Hormuz. Sure, at the time, traffic seems almost normal, and the US has begun retreating from the area, yet Iran wants full control of the critical area and demands charging taxes on vessels going through. The Iranian Revolutionary Guard warned that passage through the strait “is only possible via routes announced by Iran.”

The last one is the continued tensions between Israel and Lebanon, with the former still occupying part of southern Lebanon as a buffer zone against Hezbollah.

Markets seem optimistic, as the 60-day pause to allow negotiation is underway. Still, if there are no definitions of those three major issues, there’s a good chance tensions will re-escalate once the truce is over.

Trouble in the Old Continent

The Hamburg Commercial Bank (HCOB) released the preliminary estimates of the June Purchasing Managers’ Indexes (PMIs), which showed that business output remained in contraction territory in the month, with the Composite PMI printing at 49.5, slightly better than the 48.5 posted in May, still worrisome.

Comments from European Central Bank (ECB) officials were mixed. On the one hand, Member of the Executive Board Isabel Schnabel noted that the ECB is not done tightening yet. Schnabel said that based on current conditions, further rate hikes will likely be needed to bring inflation back to the central bank’s goal of 2%. On the other hand, President Christine Lagarde noted that while the inflation shock is too significant to ignore, it remains insufficient to drive up long-term inflation.

United States resilience

US data, on the other hand, supported the USD rally by indicating that the world’s largest economy remains strong despite continued headwinds. The S&P Global Composite PMI came in at 52.2 in June, better than the 51.5 posted in May. Growth was reported in both main sectors, as manufacturing output improved to 55.7 from the previous 55.1, while the Services PMI printed at 51.3, above the 50.7 posted in May.

More relevant, the country published the Personal Consumption Expenditures (PCE) Price Index, the Fed’s favorite inflation gauge, which climbed to 4.1% YoY in May from 3.8% in April, as expected. Not good news as inflation doubles the Federal Reserve’s (Fed) 2% goal, but at least in line with expectations. The annual core PCE Price Index also met expectations, printing at 3.4%. Also, the final revision to the Q1 Gross Domestic Product (GDP) indicated that the economy expanded faster than previously anticipated, with the figure coming in at 2.1%, better than the previous estimate of 1.6%.

What’s next in the docket

In the coming days, Germany will release May Retail Sales and the preliminary estimate of the Harmonized Index of Consumer Prices (HICP) for June, forecast at 2.7% YoY. The EU will also publish the June HICP, with annualized inflation, according to the index, expected at 3%, easing from the 3.2% posted in May.

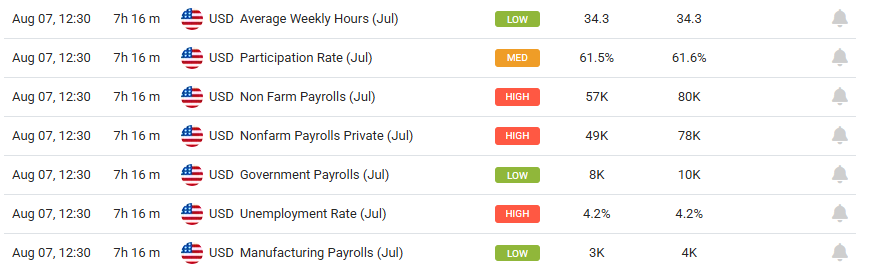

Across the pond, the focus will be on employment. The US will publish May JOLTS Job Openings, the June ADP Employment Change survey, and Challenger Job Cuts for the same month ahead of the Nonfarm Payrolls (NFP) report scheduled for Thursday. Other than that, the ISM Manufacturing PMI is scheduled on Wednesday.

ECB President Christine Lagarde and Fed Chair Kevin Warsh, among other major central bank leaders, will participate in the ECB’s Forum on Central Banking in Sintra, Portugal, and their words will be closely followed for hints on the inflation perspective and future monetary policy.

EUR/USD Technical Outlook:

From a technical perspective, the daily chart for EUR/USD indicates that the bearish trend remains in place despite the latest bounce. Spot holds below the 20-day Simple Moving Average (SMA) at 1.1517 and remains capped by the 100-day and 200-day SMAs at 1.1646 and 1.1662, respectively. The shorter one gains bearish traction below the longer ones, reflecting prevalent selling pressure. At the same time, the Relative Strength Index (RSI) indicator hovers around 36, recovering from oversold territory, while the Momentum indicator aims marginally higher, still below its midline and far from suggesting additional gains ahead.

In the weekly chart, EUR/USD’s bearish case is even clearer. The pair trades beneath the 20-week SMA at 1.1634 and slowly approaches a bullish 100-week SMA at 1.1291, the next downward inflection point. Technical indicators maintain their firm downward momentum within negative levels and far from oversold territory, supporting the case for lower lows ahead.

On the topside, initial resistance is located at the 20-day SMA cluster near 1.1517, with further barriers at the 100-day SMA around 1.1646. The weekly low at 1.1324 provides support ahead of the 100-week SMA at 1.1291. A break below the latter will likely put on the table the psychological 1.1000 mark.

(The technical analysis of this story was written with the help of an AI tool.)

Written by : Editorial team of BIPNs

Main team of content of bipns.com. Any type of content should be approved by us.

Share this article: