The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The recapture of both moving averages marks a swift rebound after silver spent 14 days below them. Lower correction targets included the 50-day average at $46.53, now rising and converging with the channel centerline confirmed at $45.55—suggesting the pullback may be complete and the bull trend poised to resume.

Conviction from the $45.55 reversal will be measured against the mid-October $54.49 peak; exceeding that level confirms continuation. Today’s strength reduces odds of an immediate second top, with the bullish hammer and inside week on the weekly chart adding validation.

The four-week high at $52.78 emerges as the immediate upside objective. Today’s breakout already triggered the inside week and hammer setup, with confirmation likely on a daily close above the three-week high of $49.38.

Silver operates within a rising trend channel that saw a late September breakout above the top line. The recent pullback briefly dipped below but respected the line as support on multiple occasions, including the $49.38 minor swing high test of resistance.

Today’s $50.56 high returned silver above the top channel line—another bullish signal. A successful retest of the line as support will confirm a second channel breakout and open higher measured targets.

Silver’s rapid recovery and channel re-breakout favor bull trend continuation toward $52.78 and potentially $54.49. Watch for support confirmation at the top channel line on any pullback; sustained trade above $49.38 keeps momentum intact, while failure below $45.55–$46.53 would reopen correction risks.

Gold surged to $4,085 per ounce, extending last week’s recovery as investors priced in a near 70% chance of a December rate cut by the Federal Reserve. The rally comes amid weakening U.S. labor data, falling consumer sentiment, and signs of a possible end to the historic government shutdown — a combination that’s undermining the U.S. Dollar Index (DXY) and pushing safe-haven demand sharply higher.

The Senate’s 60–40 vote to reopen federal agencies reduced near-term political risk while triggering broad risk-on flows across markets. Yet, gold’s strength shows investors are betting that fiscal relief will lead to a weaker dollar and renewed liquidity — a classic setup that supports precious metals.

Fresh macro data from October revealed deep cracks in the U.S. job market. Over 150,000 layoffs were reported, marking the largest October job-cut total in over two decades. Meanwhile, the University of Michigan Consumer Sentiment Index plunged to 50.3, the lowest since mid-2022 and well below the forecasted 53.2.

The downturn reinforced investor conviction that the Fed will deliver another 25 basis point cut at the December meeting, reducing rates to the 3.50%–3.75% range. For XAU/USD, lower rates directly translate to reduced opportunity costs, making the metal more attractive than yield-bearing assets.

Traders note that the recent slowdown in Non-Farm Payroll growth, averaging just 95,000 per month in 2025 versus 200,000+ in 2023–2024, signals fading momentum across multiple sectors. These data points continue to anchor bullish sentiment around gold, as rate-sensitive investors hedge against further U.S. economic weakness.

Central bank accumulation remains one of the most powerful undercurrents in gold’s rally. According to the World Gold Council, global central banks — led by China, India, and Turkey — have collectively added over 800 tonnes of gold in 2025 through Q3.

Emerging markets continue to diversify reserves away from U.S. Treasuries and into gold amid persistent currency volatility. This structural trend has created a floor under gold prices near the $3,900–$4,000 range, insulating the market from deeper corrections.

Institutional flows confirm similar behavior, with ETFs recording three consecutive weeks of inflows totaling over $3.1 billion. This surge reflects renewed conviction that XAU/USD remains undervalued relative to its inflation-hedge appeal and central bank hoarding pace.

Technically, gold has re-established its bullish trajectory. After bouncing off the 20-day EMA near $3,981, buyers defended the $4,000 psychological level and pushed prices toward the $4,085 zone, confirming renewed upward strength.

Key resistance now stands near $4,100–$4,130, with an extension target of $4,265, last month’s high. If momentum persists, the market could retest the October record near $4,380, before a broader advance toward $4,400–$4,500.

On the downside, immediate support is positioned at $4,025, followed by $3,900 at the 50-day EMA. Momentum indicators remain constructive — the RSI at 54 and a bullish MACD crossover signal a continued upward bias.

While the Senate’s move to end the shutdown temporarily boosts investor confidence, the fiscal implications could paradoxically support gold further. Reopened federal spending raises long-term deficit projections, adding to structural debt concerns that historically fuel gold accumulation.

Analysts emphasize that the shutdown’s resolution is not inherently bearish for gold. Although it may cause a short-lived USD bounce, broader market interpretation leans toward higher fiscal outflows, delayed growth, and lower yields — all favorable for gold’s medium-term outlook.

Traders are now watching how the Treasury market absorbs the $125 billion in new issuance this week. Should yields remain subdued despite supply expansion, XAU/USD could see another leg higher toward $4,200 before mid-November.

Markets continue to price a 64%–70% chance of a December rate cut as inflation slows and growth data weaken. Fed officials’ tone has softened, with policymakers hinting that policy tightening has achieved sufficient disinflation.

Lower real rates historically create a twofold benefit for gold: they diminish the relative yield advantage of bonds and weaken the dollar’s purchasing power. The current DXY range around 99.5 underscores fading demand for the greenback, with multiple analysts projecting further downside toward 98.7 in Q4.

The bond market reinforces this narrative — the 10-year Treasury yield (BX:TMUBMUSD10Y) holding near 4.11% reflects stable nominal yields against falling inflation expectations, creating the ideal backdrop for sustained XAU/USD strength.

Institutional traders are increasingly using bull call spreads and put-sell combinations to capture upside while managing volatility. With volatility metrics subdued and implied skew favoring calls, options desks indicate rising appetite for $4,200–$4,400 strike exposure through December.

Funds also appear to be rotating from equities into commodities — particularly gold and silver — amid valuation concerns in AI and tech sectors. Silver, gold’s industrial counterpart, has gained 1% this week, hovering near $50 per ounce with 65% year-to-date performance, reflecting broader precious metal strength.

Market data shows speculative long positions in COMEX gold futures increasing by over 8% week-on-week, the largest net build since March. These leveraged inflows align with strong ETF demand, confirming synchronized institutional optimism.

Despite the brief recovery in risk assets, the dollar-devaluation trade remains the key macro narrative supporting gold. Analysts highlight persistent deficits, rising interest costs, and expanding debt-to-GDP ratios as the primary long-term drivers for gold’s appreciation.

Experts warn that even a temporary delay in the next rate cut won’t derail the bullish thesis, as the underlying real yield compression and fiscal imbalance maintain structural support for precious metals.

Forecasts from leading institutions reinforce this trajectory — Goldman Sachs targets $5,055, Bank of America $5,000, and UBS $4,700 under its upside scenario by 2026. Consensus targets for Q1 2026 cluster around $4,200–$4,400, implying moderate upside but strong retention above current levels.

After analyzing labor weakness, rate expectations, central bank accumulation, and technical resilience, TradingNews maintains a decisive BUY outlook on Gold (XAU/USD). Support at $4,000 remains firm, while upside potential stretches toward $4,200–$4,400 in the short term and $5,000+ over the next 12 months.

Gold continues to stand as the preferred macro hedge in an environment of dovish monetary policy, fiscal expansion, and dollar devaluation. Unless the Fed surprises with hawkish rhetoric or DXY rebounds above 100.3, the path of least resistance remains upward.

The technical and fundamental alignment — from Fed expectations to central bank flows — confirms that gold’s bullish cycle remains intact, positioning XAU/USD as one of the most resilient trades heading into 2026.

The ongoing US government shutdown and the divergent market expectations for the future policies of the US Federal Reserve continue to heavily influence the trajectory of the US Dollar against other major currencies, as well as the rest of the global financial markets. The US government shutdown is preventing the release of US jobs figures, which are the most important economic data affecting market expectations for the future of Federal Reserve policy. In addition to that report, US inflation readings are due to be announced this week.

Prior to that, the EUR/USD pair attempted to recover from its three-month lows when it plunged to the 1.1468 support level last week, but the cautious upward rebound gains did not exceed the 1.1592 resistance level before closing the week stabilized around the 1.1560 level.

According to Forex currency trading experts’ forecasts, the bearish outlook for the EUR/USD pair was confirmed by its stabilization below the 1.1600 support. As I mentioned before, this opens the door for further downward pressure on the currency pair, which has happened. The continuation of the bearish outlook does not rule out a drop to the 1.1400 support level, especially since the technical indicators, which have turned bearish, have room to move downward before reaching the oversold zone. Currently, the 14-day Relative Strength Index (RSI) is around a reading of 44, below the neutral line, and at the same time, the MACD indicator lines are steadily leaning downward.

Conversely, on the same timeframe, the daily chart indicates a strong bullish scenario for the EUR/USD pair, requiring a move towards the psychological resistance level of 1.1800. Today’s EUR/USD trading is not focused on any major US economic releases; the only anticipated indicator is the Sentix Eurozone Consumer Confidence Index, due at 11:30 AM Cairo time.

The EUR/USD gains will remain vulnerable to rapid collapse until investor confidence returns to the market, which could happen with the end of the US government shutdown.

The future of US central bank policy is becoming increasingly uncertain.

The prospects for US monetary policy remained ambiguous following the recent wave of statements from Federal Reserve officials. Divisions among Fed policymakers persisted in the wake of last Wednesday’s US interest rate cut, raising doubts about their ability to agree on another cut at their anticipated meeting on December 9-10. While some officials openly supported further monetary easing, others expressed reluctance, if not opposition, to cutting US interest rates again next month.

In short, the overall tone of official statements on Thursday and earlier this week reinforced Federal Reserve Chair Jerome Powell’s assertion that a December US interest rate cut is “not a given.”

John Williams, President of the New York Fed, one of Powell’s most prominent aides as Vice Chair of the policy-making FOMC, had been supportive of policy easing in recent weeks to address labor market weakness, but last Thursday he limited his comments to saying the bank must adhere to its 2% inflation target and strive for “price stability.”

Meanwhile, Austin Goolsbee, president of the Federal Reserve Bank of Chicago, who voted for rate cuts in September and October, appeared less insistent on another rate cut on Thursday, particularly given the lack of economic data from the closed federal government. He saw “stabilization” in the labor market and expressed deep concern about inflation in the absence of statistics. Meanwhile, Beth Hammack, president of the Federal Reserve Bank of Cleveland, who will join the Federal Open Market Committee (FOMC) voting line next year, was more vocal in her opposition to another near-term rate cut, arguing that inflation is a greater concern than the struggling labor market and emphasizing the need for monetary policy to remain “in a fairly restrictive position to achieve the right balance of our objectives.”

Overall, for the second consecutive meeting, the FOMC lowered the US interest rate by 25 basis points on October 29 to a target range of 3.75% to 4.0%. However, in an unusually split decision, Federal Reserve Governor Stephen Miran opposed a 50-basis point cut, while Kansas City Fed President Jeffrey Schmid opposed the decision, favoring keeping rates unchanged.

In addition to this easing move, the FOMC moved faster than many expected to halt “quantitative tightening” by the end of this month. The FOMC had cut the interest rate by the same amount on September 17 to a target range of 4.0% to 4.25%. In its revised Summary of Economic Projections, published in September, FOMC participants anticipated another 25 basis points of monetary easing at the Committee’s final meeting in 2025.

Despite 25 basis points remaining in the September “dot plot,” Powell stressed in his October 29 press conference that a rate cut on December 9-10 “is not a foregone conclusion, far from it.” He noted “sharp differences in views on how to proceed in December.” He added that the FOMC has cut the federal funds rate by 150 basis points since it began easing monetary policy in September 2024, making policy now “150 basis points closer to neutral.” He added that this prompts some officials to “pause” and “wait” before easing policy further, while others wish to “move forward” with more easing.

Powell said the FOMC “will resume monetary easing at some point,” but added that it is trying to deal with a “difficult” and “complex” situation that requires “balancing” the two-sided risks—either in favor of inflation or in favor of jobs. In this climate, he said it is appropriate to be “cautious.” He added that if there is a “high degree of uncertainty” on December 10, “that might justify caution about moving.”

Ready to trade our EUR/USD daily forecast? Here’s a list of some of the top forex brokers in Europe to check out.

The EURJPY pair affected by stochastic positivity, form bullish waves to retest the barrier at 177.85, to settle below it to keep the chances of activating the bearish corrective track, note that the initial corrective target in the current trading near 177.05 level, by providing negative momentum that might help it to reach near 175.85 support.

While confirming regaining the bullish bias requires forming a new bullish rally, to open the way a new chance to press on the top at 178.70. surpassing it will make it record new gains by its rally towards 179.30 and 180.00.

The expected trading range for today is between 177.00 and 178.15

Trend forecast: Bearish.

Image © Adobe Images

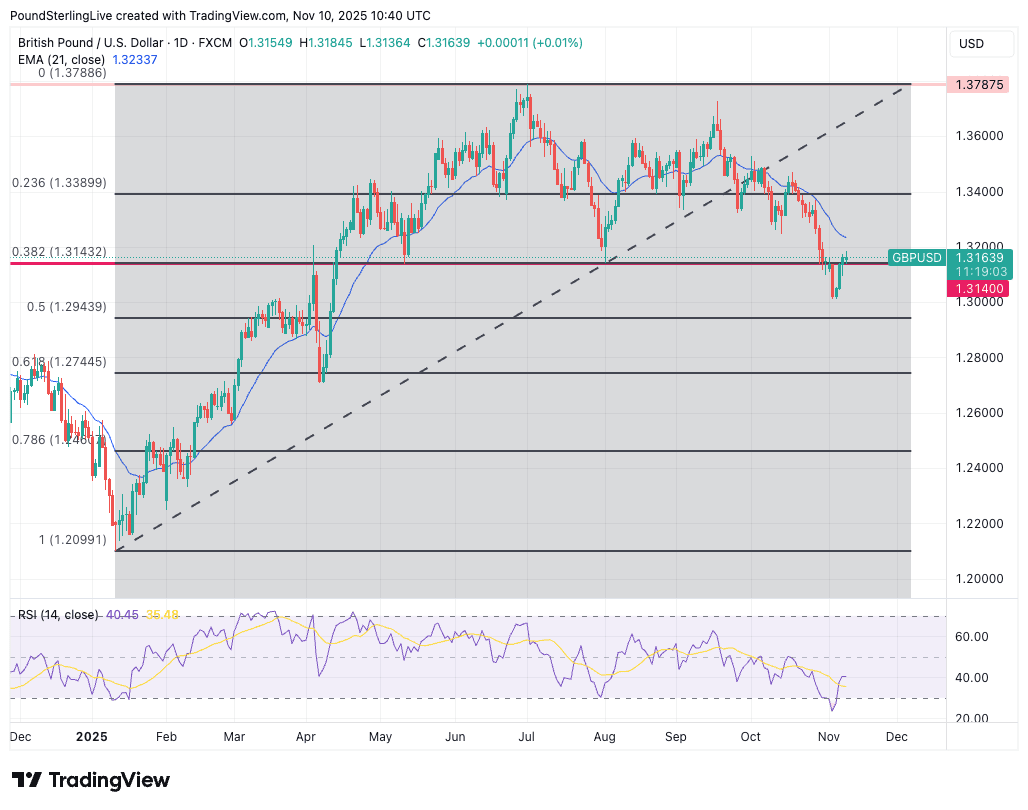

The pound to dollar exchange rate (GBP/USD) reached its lowest level since April last week at 1.3010, but has since recovered to 1.3170.

The recovery is shallow and lacks the vigour that would normally be associated with a bottoming pattern, leaving us wary of a continuation of the selloff.

This is why we would characterise the current rally as a mean reversion, and not the start of a renewed push higher.

The pair looks to be recovering from the oversold conditions seen at the start of the month, the culmination of the steady selling pressure seen through the course of October.

The RSI – lower panel in the chart – had fallen below 30, which triggers caution and indicates that those oversold conditions must unwind.

Exchange rates tend to mean-revert, and we are seeing that in GBP/USD. The week ahead forecast looks for that to play out a little further, targeting a move to the 21-day exponential moving average at 1.3235.

Above: GBP/USD looks to be eyeing a return to the 21-day EMA (blue line). Note the bounce out of oversold on the RSI in lower panel.

However, while below this EMA the pair is in a downtrend and the relief could attract more sellers, ready to target new multi-month lows.

1.3010 is the new post-April low, and below here is a potential support region; the 50% Fibonacci retracement of the Q1-2025 rally.

How far GBP/USD can travel will depend on Tuesday’s UK labour market data, where the unemployment rate is expected to have fallen to 4.9% in October from 4.8% in September, owing to rising unemployment and inactivity.

A more severe deterioration in the headline employment numbers would trigger a selloff in the pound, undermining our tactical expectation for a short-term recovery.

Also, keep an eye on the wage figures, as this is closely associated with inflation. The figure to beat is 4.6%.

Quarterly GDP is due Thursday, where the consensus looks for a 0.2% increase in Q3. The UK economy has actually been doing OK this quarter, according to the PMI surveys and retail sales data.

This means a beat on expectations can’t be ruled out. If it happens, then GBP/USD can end the week above 1.3235.

Stateside, there will be no official U.S. data owing to the government shutdown, which deprives us of a previously scheduled inflation data release.

This is one of the two marquee economic calendar events in any given month, the other being non-farm payroll data.

Nevertheless, “attention this week will turn to remarks from several Fed officials, which could provide new clues on how the central bank is balancing softening consumer confidence with a fragile labour market,” says Konstantinos Chrysikos, Head of Customer Relationship Management at Kudotrade.

Above: The Fed’s Waller speaks Wednesday.

“Dovish remarks could weigh on both the dollar and yields,” he adds.

Markets see a 65% probability of a December rate cut, which signals ample scope for a repricing in either direction, based on the tone of upcoming commentary and non-official data releases.

The weekend saw some progress towards ending the record-long government shutdown, with Senate Democrats voting through a procedural measure to advance a bill to pass funding.

“It looks like we’re getting closer to the shutdown ending,” President Donald Trump said Sunday.

Senate Majority Leader John Thune said over the weekend that a bipartisan budget framework is taking shape.

There’s no clear timeline for the reopening, which means the Fed’s December policy meeting will happen without official data to assess.

However, sentiment would receive a boost on a reopening of government, setting the scene for a recovery in stocks, which would weigh on the dollar.

The Federal Reserve has held rates steady since September, but the combination of softer employment data and declining business confidence has prompted speculation that policymakers may ease monetary conditions to support demand heading into 2026.

The latest labor data underscored the fragility of the US job market. Private employers cut 153,000 jobs in October, the steepest monthly decline in over two decades. Layoffs in the government and retail sectors, coupled with an uptick in corporate cost-cutting, heightened fears of a broader slowdown.

Consumer sentiment also dropped to its lowest level in nearly three and a half years, according to a University of Michigan survey, as Americans grew increasingly concerned about inflation, fiscal uncertainty, and the prolonged government shutdown.

These developments have pushed investors toward precious metals, which tend to perform well in times of economic uncertainty and falling interest-rate expectations.

Silver followed gold higher, supported by its dual role as both a safe-haven and an industrial metal. Analysts at Metals Focus noted that expectations of weaker Treasury yields and a potential rebound in manufacturing activity could sustain silver’s momentum.

With market attention turning to Fed speeches and upcoming inflation data, traders are closely watching whether policymakers confirm growing market bets on a softer monetary path through year-end.

– Written by

Tim Boyer

STORY LINK Euro to Dollar Forecast: EUR/USD Set for Gains in Early 2026

The Euro to Dollar exchange rate (EUR/USD) dipped to three-month lows at 1.1470 during the week, but has since recovered to around 1.1575 amid concerns over the US government shutdown and the US labour market.

Forecasts from SocGen and MUFG suggest EUR/USD will strengthen to 1.20 in early 2026, but the outlook remains clouded by ongoing uncertainty over the US economy.

Foreign exchange strategists at SocGen forecast that the Euro to US Dollar rate will strengthen to 1.20 in the first quarter of 2026, but won’t be able to sustain the gains with a retreat to 1.14 by the end of 2026.

MUFG also expects EUR/USD will strengthen to 1.20 early next year but expects dollar weakness will continue during the year with a third-quarter forecast of 1.26.

EUR/USD dipped to 3-month lows at 1.1470 during the week before a recovery to around 1.1575 amid fresh concerns surrounding the US labour market.

At this stage, markets are pricing in just over a 65% chance that the Federal Reserve will cut interest rates again in December.

Get better rates and lower fees on your next international money transfer.

Compare TorFX with top UK banks in seconds and see how much you could save.

There is, however, major uncertainty over the outlook with the on-going government shutdown amplifying the lack of clarity and increasing reservations.

MUFG comented; “There is no end in sight to the shutdown and the longer this drags on the bigger the economic implication will be.”

It expects; “Renewed USD depreciation by yearend and in 2026.”

Challenger reported that layoffs in October surged 175% from a year ago to 153,074, the highest October figure for 20 years. For the first 10 months of the year, layoffs have increased 65% from the previous year to around 1.1mn.

ADP, however, did register an increase in private payrolls of 42,000 for October after a revised 29,000 decline the previous month.

The dollar will be notably vulnerable if there is evidence of serious labour-market deterioration. The narrative will, however, be different if the economy is resilient and growth holds firm.

SocGen commented; “If the growth differential returns to wider levels, more in line with the average of the last decade, why would the euro not drift back towards that longer-term average? It will get some support from narrower rate differentials, but even those suggest EUR/USD ought to be lower than it is today.”

According to ING; “We think it’s too early to call time on the dollar bear trend and the EUR/USD rally. The house call is for three more Fed rate cuts, and there is much uncertainty over both the shape of the US labour market and whether political pressure will bear down on the Fed next year.”

The bank added; “Our 1.20 forecast for EUR/USD for the end of this year is now a bit of a stretch. But year-end seasonality and the true state of the US jobs market should be supportive. And some modest gains next year are still the preferred call.”

International Money Transfer? Ask our resident FX expert a money transfer question or try John’s new, free, no-obligation personal service! ,where he helps every step of the way,

ensuring you get the best exchange rates on your currency requirements.

TAGS: Euro Dollar Forecasts

No news for copper price by forming weak sideways trading, to keep its stability near $5.000 level due to the contradiction between the main indicators, which might force it to delay the main bullish rally.

Notet that the stability of the current trading below $5.2000 level might force it to provide some bearish corrective trading, to target the initial support level at $4.7500, while breaching the barrier will reinforce the chances of recording extra gains by its rally towards $5.3200 initially.

The expected trading range for today is between $4.9000 and $5.1500

Trend forecast: Fluctuated within the bullish track

The British pound has rallied a bit against the Japanese yen during trading on Friday as the market continues to see a lot of volatility in general. We are sitting right around the 50-day EMA, which of course, is an indicator that a lot of people will pay close attention to. It’s worth noting that the last couple of days have broken below the 200 yen level.

The 200 yen level is an area that is a large, round, and psychologically significant figure, but it was also the beginning of the gap that we just filled. By filling this gap, it does look like we’re doing everything we can to continue the uptrend, and with the Bank of England showing a little bit of hesitation to cut rates, this gives us more of a reason to think that the pound may actually be okay by the time it’s all said and done.

Keep in mind that the Japanese yen is very weak in general, and I think that’s the main driver of what happens here. The Japanese yen has been extraordinarily weak, and I don’t see that changing anytime soon, given the fact that the Bank of Japan has no real shot at trying to tighten monetary policy. Short-term pullbacks at this point in time should continue to be buying opportunities, and I do think that eventually we’ll go looking to the 204 yen level.

If we broke down below the 199 yen level, then we would test the 200-day EMA, which is a major indicator as well. Anything below there really opens up the downside, and we could see this market completely fall apart.

Want to trade our USD/JPY forex analysis and predictions? Here’s a list of forex brokers in Japan to check out.

Christopher Lewis has been trading Forex and has over 20 years experience in financial markets. Chris has been a regular contributor to Daily Forex since the early days of the site. He writes about Forex for several online publications, including FX Empire, Investing.com, and his own site, aptly named The Trader Guy. Chris favours technical analysis methods to identify his trades and likes to trade equity indices and commodities as well as Forex. He favours a longer-term trading style, and his trades often last for days or weeks.

Gold price (XAU/USD) jumps to near $4,075 during the early European trading hours on Monday. The precious metal edges higher amid uncertainty over the US economic outlook. Traders ramped up bets on a US rate cut following weak US private jobs data and a downbeat University of Michigan (UoM) Consumer Sentiment Index survey. Lower interest rates could reduce the opportunity cost of holding Gold, supporting the non-yielding precious metal.

On the other hand, signs that the US government shutdown may end could undermine safe-haven assets such as Gold. US senators are voting on a deal on Monday that could end the longest government shutdown in history. Furthermore, easing trade tensions between the US and China, the world’s two largest economies, could also drag the yellow metal lower in the near term.

Traders will closely monitor the US October Consumer Price Index (CPI) inflation data later on Thursday. The headline CPI is expected to show an increase of 0.2% MoM in October, while the core CPI is projected to show a rise of 0.3% MoM during the same period. The US Retail Sales will be in the spotlight on Friday.

Gold price trades in positive territory on the day. According to the daily chart, the positive outlook of the precious metal remains in play as the price holds above the key 100-day Exponential Moving Average. The path of least resistance is to the upside, with the 14-day Relative Strength Index (RSI) standing above the midline near 55.0. This displays the bullish momentum for the yellow metal in the near term.

Sustained trading above the October 22 high of $4,161 could send the yellow metal toward the $4,200 psychological level. Further north, the next hurdle to watch is the upper boundary of the Bollinger Band at $4,325.

If we start seeing bearish candlesticks and consistent trading below $4,000, that could signal that sellers are back in control. In that case, XAU/USD might return to the lower limit of the Bollinger Band of $3,835, followed by the 100-day EMA of $3,705.

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money.

When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions.

The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Price Forecast: .56 14-Day High Recaptures 20-Day MA")

")

& Silver Price Forecast: Fed Dovish Turn Lifts ,000 and Outlook")

")