The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The Italian bank says expectations that Andy Burnham will appoint a fiscally conservative Chancellor have created a potential “wind of change” for UK assets, easing concerns over public finances and providing support for the Pound.

GBP/USD was trading around 1.3450 on Friday after rising more than 1.7% in July, recovering from June’s decline and moving back above the 1.35 area earlier in the week.

UniCredit says Sterling’s recent strength has been driven by expectations surrounding the incoming UK government and, in particular, the choice of Chancellor.

Reports that current Home Secretary Shabana Mahmood is the frontrunner for the role have reduced market concerns that Burnham could pursue a more expansionary fiscal approach.

The bank argues that fiscal credibility has become a crucial factor for investors following recent concerns over rising UK borrowing needs.

A more conservative approach to government finances could reduce pressure on gilt markets and improve confidence in Sterling.

UniCredit highlights the reaction in UK government bonds as an important indicator of improving market sentiment.

Following reports on the expected Chancellor appointment, gilts rallied, with the 10-year UK yield falling below 4.92% after reaching close to 5.20% in May.

The bank notes that concerns over UK fiscal policy had previously pushed gilt yields higher and weighed on the Pound.

However, current market conditions are very different from the September 2022 mini-budget crisis, when unfunded tax cuts triggered a sharp sell-off in UK assets and sent GBP/USD to record lows.

UniCredit believes the recent improvement in sentiment could allow further Sterling gains if expectations around the new government are confirmed.

The bank notes that GBP/USD has already moved above 1.35 for the first time since May, while EUR/GBP has fallen below 0.85 to multi-year lows.

Technical indicators suggest GBP/USD could target 1.37 if positive sentiment continues.

However, UniCredit cautions that it is still too early to determine whether this represents a lasting shift in investor positioning or simply a short-term reaction to political developments.

Another factor supporting Sterling is the possibility that markets continue pricing a Bank of England rate increase later this year.

UniCredit says that if expectations of a November rate hike remain in place, the summer period could prove far less damaging for Sterling than political uncertainty earlier in the year had suggested.

A combination of improved fiscal confidence, stronger gilt performance and supportive rate expectations could therefore provide further support for the Pound.

UniCredit sees scope for GBP/USD to extend its recovery if the improving political backdrop is sustained.

The bank highlights 1.37 as the next potential target for the pair, while acknowledging that further gains depend on continued investor confidence in the new UK government’s fiscal approach.

With GBP/USD currently near 1.3450, Sterling has already recovered significantly from its June lows, but UniCredit believes the recent political shift could provide further upside momentum.

Why is UniCredit positive on the Pound?

UniCredit believes expectations of a fiscally conservative UK Chancellor could improve investor confidence, support gilts and reduce concerns over government borrowing.

What is UniCredit’s GBP/USD target?

The bank highlights 1.37 as a potential next target for GBP/USD if positive market sentiment continues.

Why are UK gilts important for Sterling?

Gilt yields and demand from investors are closely linked to confidence in UK fiscal policy. Stronger gilt performance can support the Pound by reducing concerns over government finances.

Could political uncertainty still hurt GBP/USD?

Yes. UniCredit says it is too early to confirm whether the recent move represents a lasting change in sentiment, meaning Sterling remains sensitive to developments surrounding the new government.

The central bank of Chile, the world’s largest copper producer, recently lowered its 2026 economic growth forecast, but it raised its average copper price forecast to US$5.90 per pound. The change reflects strong global demand and limited mine supply. It also shows that copper remains one of the world’s strongest commodity markets, even as economic growth slows.

As the biggest producer, Chile has a major influence on global copper supply. Copper is essential for power grids, electric vehicles (EVs), renewable energy, battery storage, and AI data centers. Higher prices could benefit mining companies while supporting the industries driving the global energy transition.

Chile’s latest forecast shows confidence in the copper market. The central bank expects copper to average US$5.90 per pound in 2026, before easing to US$5.20 in 2027 and US$5.00 in 2028.

Even with slower economic growth, officials believe demand will stay strong because the world still needs more copper for clean energy and new technology.

Chile’s Copper Commission (Cochilco) shares that view. Earlier this year, it also raised its copper price outlook. The agency said prices are being supported by tight global supply and growing demand from renewable energy, electric transport, and digital infrastructure.

Copper prices have seen some ups and downs over the past year. However, they remain well above their historical average. Analysts say the market is now being driven more by long-term demand than by short-term economic swings.

Copper has become one of the world’s most important metals.

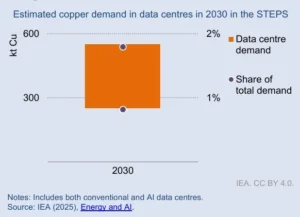

According to the International Energy Agency (IEA), power grids will create the largest increase in copper demand over the coming decades. Countries need thousands of kilometers of new transmission lines to connect renewable energy projects and meet rising electricity demand.

Electric vehicles also use much more copper than traditional cars. The IEA estimates that a battery-powered EV needs about 2.5x more copper than a gasoline-powered vehicle. Wind turbines, solar farms, and battery storage systems also require large amounts of the metal.

Artificial intelligence is adding even more demand. AI data centers need transformers, substations, cooling systems, backup power, and large networks of electrical cables. All of these use copper.

The IEA expects electricity use by data centers around the world to more than double by 2030, reaching about 945 terawatt-hours (TWh) each year. That is roughly equal to Japan’s total annual electricity use today. Most of the increase will come from AI.

As companies like Google, Microsoft, Amazon, and Meta build more AI data centers, demand for copper will keep growing.

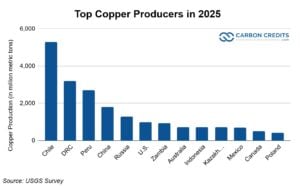

Chile remains the world’s biggest copper producer.

According to the U.S. Geological Survey (USGS), Chile produced about 5.3 million metric tonnes of copper in 2025. That was about one-quarter of global mine production.

The country’s biggest mines include Escondida, Collahuasi, and Codelco. Together, they supply copper to manufacturers around the world.

Cochilco expects Chile’s annual copper production to reach about 5.54 million metric tonnes by 2034. However, growth is likely to be slow. Many older mines now produce lower-grade ore. New mining projects are also becoming more expensive and take longer to develop.

Chile’s state-owned miner Codelco recently said its production is expected to stay close to current levels over the next few years instead of reaching its long-term target of 1.7 million metric tonnes a year by 2030.

Bernardo Fontaine, Codelco Chairman, remarked:

“It is very possible that it sits at a production rate quite similar to the one it has today.”

The company is still recovering after output fell to its lowest level in more than 20 years during 2022 and 2023. Production from its own mines reached 1.33 million metric tonnes last year.

Fontaine further said several major expansion projects have faced unexpected delays and higher costs as it works to offset declining ore grades. The company also sees the El Abra mine, where it owns a 49% stake alongside Freeport-McMoRan, as a promising project for future investment. Freeport plans to invest US$7.5 billion to expand the mine.

With demand rising and supply growing slowly, many analysts believe copper prices could remain strong for years to come.

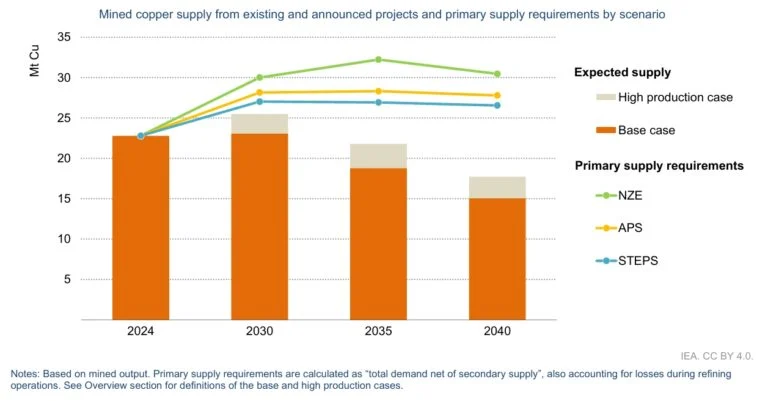

While demand keeps growing, copper supply is not rising as fast.

Many of the world’s largest copper mines are getting older. As ore grades fall, companies must process more rock to produce the same amount of copper. That increases both costs and energy use.

New mines also take a long time to build. According to the IEA, developing a new copper mine can take 15 to 20 years from discovery to production. Permitting, financing, and environmental reviews all add time to the process.

The International Copper Study Group (ICSG) expects global mine production to increase over the next few years. However, many analysts believe that growth will still fall short of future demand because of project delays, lower ore grades, and rising costs.

Copper is now at the center of the clean energy transition.

The IEA estimates that clean energy technologies could account for almost half of global copper demand by 2040 under a pathway that reaches net-zero emissions by 2050. That includes electric vehicles, renewable power, battery storage, electricity networks, and hydrogen projects.

Power grids will need the biggest investment. The World Bank estimates that global electricity networks must expand rapidly to support cleaner energy and growing electricity demand. Every new transmission line, transformer, and substation requires large amounts of copper.

The rapid growth of AI is adding another layer of demand. New data centers require huge amounts of electrical equipment before they can even begin operating. As more countries build AI infrastructure, copper demand is expected to remain strong.

Strong copper prices may also encourage companies to invest in new projects. The challenge is timing.

Even if companies approve new projects today, many will not begin producing copper until the next decade. That means supply could remain tight while demand continues to grow.

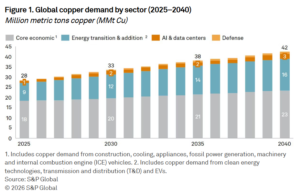

According to S&P Global, global copper demand could nearly double, from 28 million metric tons a year in 2025 to 42 million metric tons by 2040. This is driven mainly by electrification, clean energy, AI, and digital technologies. Meeting that demand will require major investment across the mining sector.

Copper’s long-term outlook remains positive, but risks still exist. A weaker global economy could reduce industrial demand in the short term. Trade tensions and changing government policies may also create periods of price volatility.

However, most market analysts expect the long-term trend to remain strong because the world cannot expand clean energy without more copper.

Chile’s latest forecast reflects that reality. Even as economic growth slows, the country expects copper prices to stay well above historical levels because demand continues to outpace supply.

As countries build more renewable power, modernize electricity grids, expand AI infrastructure, and produce more electric vehicles, demand for copper is likely to remain strong for many years. That is why many analysts believe today’s high prices may be part of a much longer market cycle rather than a short-term rally.

The article covers the following subjects:

Consider long positions from corrections above 161.55 with a target of 166.50–170.00.

Breakout and consolidation below 161.55 will allow the pair to continue declining to the levels of 159.86–158.90.

On the weekly time frame, an ascending third wave of larger degree 3 has formed, a downward correction has been completed as the fourth wave 4, and the fifth wave 5 is developing. On the daily chart, the third wave of smaller degree (3) of 5 appears to be developing, with wave 3 of (3) forming as its part. On the H4 time frame, wave i of 3 has formed, a local correction has been completed as wave ii of 3, and wave iii of 3 is developing. If the presumption is correct, USD/JPY will continue to rise to 166.50–170.00. The level of 161.55 is critical in this scenario as a breakout below it will enable the pair to continue declining to the levels of 159.86–158.90.

This forecast is based on the Elliott Wave Theory. When developing trading strategies, it is essential to consider fundamental factors, as the market situation can change at any time.

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.

At 5:50 a.m. Eastern Time today, oil was priced at $86.09 per barrel with Brent serving as the benchmark (we’ll explain different benchmarks later in this article). That’s an increase of $1.45 compared with yesterday morning and around $16 higher than the price one year ago.

It’s impossible to forecast oil prices with detailed precision. Many different elements affect the market, but ultimately it boils down to supply and demand. When worries about economic recession, war, and other large-scale disruptions increase, oil’s path can shift fast.

Gas prices at the pump don’t only track crude oil. They also include what it takes to refine and move that fuel, the taxes layered on top, and the extra markup your local station adds to stay in business.

Since crude oil generally makes up a majority of the per-gallon cost, changes in its price have an outsized impact. When oil surges, gas prices typically rise in tandem. But when oil retreats, gas prices often lag on the way down, a trend sometimes described as “rockets and feathers.”

In case of emergency, the U.S. has a store of crude oil known as the Strategic Petroleum Reserve. Its primary purpose is energy security in case of disaster (think sanctions, severe storm damage, even war). But it can also go a long way toward softening crippling price hikes during supply shocks.

It’s not a long-term answer and is more meant to provide temporary relief, assisting consumers and keeping critical parts of the economy running, like key industries, emergency services, public transportation, etc.

Both oil and natural gas are key sources of the energy we use every day. Because of this, a big change in oil prices can affect natural gas. For example, if oil prices increase, some industries may swap natural gas for some segments of their operations where possible, which increases demand for natural gas.

To gauge oil’s performance, we often turn to two benchmarks:

Between these two, Brent better represents global oil performance because it prices much of the world’s traded crude. And, it’s often the best way to track historical oil performance. In fact, even the U.S. Energy Information Administration now uses Brent as its primary reference in its Annual Energy Outlook.

Looking at the Brent benchmark across several decades, oil has been anything but steady. It’s seen spikes due to factors such as wars and supply cuts, and it’s also seen crashes from global recessions and an oversupply (called a “glut”). For example:

All to say, oil’s historical performance has been anything but smooth. Again, it’s hugely affected by wars, recessions, OPEC whims, evolving energy initiatives and policies, and much more.

Looking to stay up-to-date regarding the latest energy developments? Check out our recent coverage:

The current price of oil per barrel depends largely on supply and demand, including news about potential future supply and demand (geopolitics, decisions made by OPEC+, etc.). In the U.S., prices also move based on how friendly an administration is to drilling, as it can affect future supply. For example, 2025 saw the Trump administration move to reopen more than 1.5 million acres in the Coastal Plain of the Arctic National Wildlife Refuge for oil and gas leasing, reversing the Biden administration’s policy of limiting oil drilling in the Arctic.

The price of oil updates constantly when the “futures” markets are open. A futures market is effectively an auction where people agree to buy or sell oil in the future. As long as people and companies are trading contracts, the oil price is changing.

In short, shale is rock that contains oil and natural gas. Think of shale as energy yet to be tapped. The more shale the U.S. accesses, the more energy we’ll have—and the more easily oil prices can keep from spiking as much thanks to a greater supply.

When oil is expensive, it tends to make everyday items cost more. This can be related to energy (your heating, gas utilities, etc.), but it’s also due to the logistics involved with making those items accessible to you. Shipping, for example, can affect the price of things at the grocery store, as it’s more expensive to get those products from warehouses and farms onto the shelf.

The GBPJPY pair lost the bullish momentum yesterday after recording 219.25 level, which forces it to activate the attempts of gathering gains, forming some negative corrective trading by reaching 218.45.

The price keeps forming corrective trading, attempting to test 217.90 level reaching the bullish channel’s support at 217.65, it will not affect the main bullish scenario, depending on forming main support at 216.30 level against the bullish trading.

The expected trading range for today is between 217.90 and 219.20

Trend forecast: Fluctuating within the bullish trend.

The article covers the following subjects:

Consider long positions from corrections above 70.40 with a target of 91.80–105.17.

Breakout and consolidation below 70.40 will allow the asset to continue declining to the levels of 62.00–58.50.

A descending correction appears to have formed as the second wave of larger degree (2) on the weekly chart, with wave C of (2) completed as its part. On the daily time frame, an ascending third wave (3) is likely developing. Within it, the first wave of smaller degree 1 of (3) has formed, a downward correction has been completed as the second wave 2 of (3), and wave 3 of (3) has started forming. Wave i of 3 is likely forming on the H4 chart, with wave (iii) of i unfolding as its part. If the presumption is correct, WTI will continue to rise to 91.80–105.17. The level of 70.40 is critical in this scenario as a breakout below it will enable the asset to continue declining to the levels of 62.00–58.50.

This forecast is based on the Elliott Wave Theory. When developing trading strategies, it is essential to consider fundamental factors, as the market situation can change at any time.

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.

The Euro has been very choppy against the Japanese yen on Thursday, continuing the overall sideways action that we have seen for weeks. The interest rate differential continues to be an issue that moves the market as well.

The Euro has been very quiet against the Japanese Yen during trading here on Thursday as we are reaching the top of the overall consolidation area that we’ve been in for basically 6 weeks. That being said, we now have a situation where traders are trying to sort out whether or not we can finally break above the 186.50 Yen level. If we can break above there, then I think that is a very good sign, and it could have this market streaming towards the 188 Yen level given enough time.

Short-term pullbacks, I think, continue to look at the 50-day EMA and the 185 Yen level. Both offer quite a bit of support. Ultimately, this is a market that I don’t have any interest in shorting because, quite frankly, the interest rate differential favors the Euro over the Japanese Yen. And of course, the Japanese Yen simply cannot seem to get a break in general. This seems to be a situation that the Bank of Japan cannot ignore.

While we are at the top of a range and I fully recognize that it is possible traders will look at this as a potential barrier, if we do break out, then I think we get a bigger move again to the 188 Yen level, possibly the 190 Yen level. I like the idea of buying short-term dips, and I recognize that the Japanese Yen in general is in trouble against multiple currencies, not just this one. So, I think this is more of an indictment of the Yen itself.

Begin trading our daily forecasts and analysis. Here is a list of Forex brokers in Japan to work with.

Christopher Lewis is a technical analyst and market commentator at DailyForex with more than two decades of trading experience in Forex and other leveraged markets. Based in Columbus, Ohio, he specializes in chart-based analysis of major currency pairs, stock indices, commodities, and energy markets, focusing on clear support and resistance levels, trend structure, and risk management. Christopher produces daily written and video analysis for traders who rely on technical setups to navigate volatile market conditions

As seen on: Pairs Of Aces Podcast,The Trader Guy, FXEmpire

Coffee price lost its bullish momentum in its last trading, forcing it to provide some bearish corrective trading by targeting 324.50 level, note that the contradiction of the main indicators might push the price to provide mixed sideways trading, however the main stability above 275.90 level forms an important support level that makes us keep the bullish scenario in the near and medium period trading.

The price needs a new bullish momentum, to step above 320.00 level, reinforcing the chances of forming new bullish waves, targeting 333.60 level initially, repeating the pressure on the barrier at 350.00.

The expected trading range for today is between 310.50 and 333.60

Trend forecast: Bullish

– Written by

James Fuller

STORY LINK Pound to Dollar Forecast: GBP Tests 1.34 as Mixed US Economic Data Clouds Fed Outlook

The Pound to Dollar exchange rate (GBP/USD) rebounded towards the 1.3400 level after a mixed batch of US economic data failed to extend the US Dollar’s recent gains.

Headline US retail sales rose 0.2% in June, matching expectations, while the closely watched control group increased a stronger-than-expected 0.5%, pointing to resilient underlying consumer demand. However, core retail sales excluding autos unexpectedly fell 0.2%, tempering enthusiasm for the Dollar despite a further decline in weekly jobless claims that reinforced the strength of the US labour market.

Investors continue to weigh evidence of resilient US economic activity against signs that consumer spending is becoming more selective, while expectations for Federal Reserve policy and developments in the Middle East remain key drivers of Dollar sentiment.

The Pound to Dollar (GBP/USD) exchange rate has continued to trade around 1.3400 and is currently trading just below this level with no attempt to break key resistance.

Scotiabank noted; “the GBP’s recovery from its June 24 low (~1.3150) looks to have stalled over the past week or so, with apparent resistance above 1.3400.”

It added; “We see dense resistance ahead of 1.3500, and we look to a near-term range bound between 1.3350 and 1.3450.”

Get better rates and lower fees on your next international money transfer.

Compare TorFX with top UK banks in seconds and see how much you could save.

ING has a 3-month GBP/USD target of 1.31 as the dollar makes headway.

Following today’s retail sales report, markets remain divided over whether resilient consumer demand will be enough to keep the Federal Reserve on a hawkish path, particularly after softer CPI and PPI inflation data earlier this week.

ING commented; “While soft US CPI data has taken the sting out of the dollar’s upside, it is probably too early to look for a much lower dollar just yet.”

According to MUFG; “Despite the muted FX reaction, the scale of weakness in the CPI report certainly helps weaken the key pillar of support for the dollar – the prospect of a near-term hike. That can open up scope for further dollar depreciation. However, it is difficult to trade with conviction given the re-escalation in the conflict in the Middle East and the 13% surge in crude oil prices this week.”

In testimony to the House Financial Services Committee on Tuesday, new Fed Chair Warsh maintained a generally hawkish stance.

He stated that the central bank has “no tolerance” for persistently elevated inflation, and vowed to “do my job” if challenged by U.S. President Donald Trump.

He also stated that he is committed to the dual mandate of 2% inflation and maximum employment.

MUFG commented; “The testimony from Fed Chair Warsh looks to have curtailed the move weaker for the dollar. Just like following his first FOMC meeting, Warsh spoke with conviction in relation to the Fed achieving its 2% inflation goal. The CPI print was not “mission accomplished” and he wasn’t going to “cherry pick” data.

The bank added; “We don’t really view this as “hawkish” given he is merely promising to focus on what is the legal mandate of the Federal Reserve. However, he again is emphasising his inflation fighting credentials.”

According to Scotiabank; “We remain of the view that Fed tightening risks this year are mispriced and soft CPI data this morning (plus the soft NFP report for June) may act to curb some of the market’s enthusiasm for rate hikes.”

International Money Transfer? Ask our resident FX expert a money transfer question or try John’s new, free, no-obligation personal service! ,where he helps every step of the way,

ensuring you get the best exchange rates on your currency requirements.

TAGS: Pound Dollar Forecasts

Platinum price kept its negative stability below the extra barrier at $1690.00, keeping the bearish corrective scenario, forming strong bearish waves, to settle near $1585.00.

Providing negative momentum by the main indicators will increase the chances of surpassing $1560.00 level, reinforcing the chances of reaching $1532.00, where surpassing it will open the way for reaching new bearish stations that begin at $1490.00 and $1440.00.

The expected trading range for today is between $1530.00 and $1620.00

Trend forecast: Bearish

")

{kind=link}