The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The (ETHUSD) price witnessed fluctuated trading in its last intraday levels, due to the stability of the key support at $4,250, gaining the bullish momentum that helped it to settle temporarily, as the price is under negative pressure that comes from its trading below EMA50, amid the dominance of the bearish correctional trend on the short-term basis, and its trading alongside a bias line, besides the emergence of the negative signals on the (RSI), after reaching overbought levels.

Get high-accuracy trading signals delivered directly to your Telegram. Subscribe to specialized packages tailored for the world’s top markets:

Full VIP signals performance report for August 25–29, 2025:

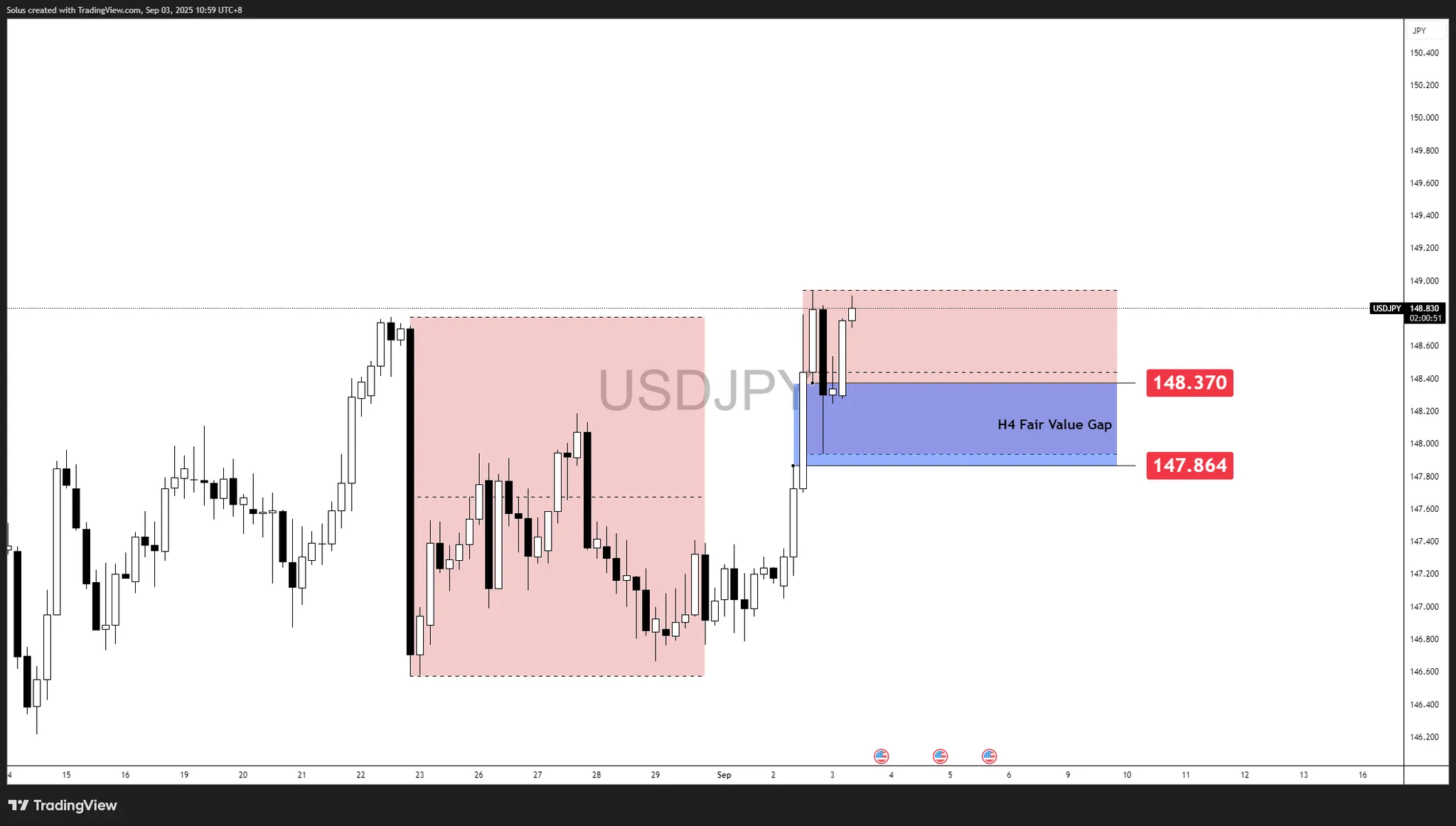

Dollar-yen is trading heavy-on-the-upside: U.S. yields remain comparatively firm and the BoJ continues to signal patience on policy normalization, reinforcing the positive carry in favor of USD.

The BoJ remains deliberately cautious, emphasizing the need for sustained wage-led inflation before meaningful tightening. With JGB 10-year yields near ~1% versus much higher U.S. Treasury yields, the carry incentive favors holding dollars over yen. That yield differential is a persistent structural tailwind for USD/JPY, keeping dips shallow and making pullbacks into demand zones (like your H4 FVG) buyable until the BoJ signals a firmer path to normalization.

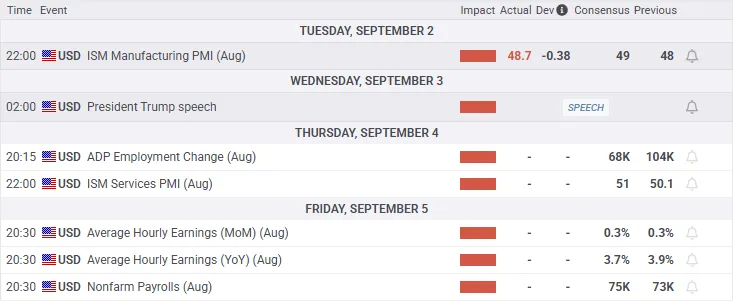

ISM Manufacturing PMI (Aug) printed 48.7, a touch below 49.0 forecast – but above the previous 48.0. Markets read that as stabilization rather than deterioration, and the USD caught a bid despite the “contractionary” label. This is a good reminder that direction of change often beats the absolute level.

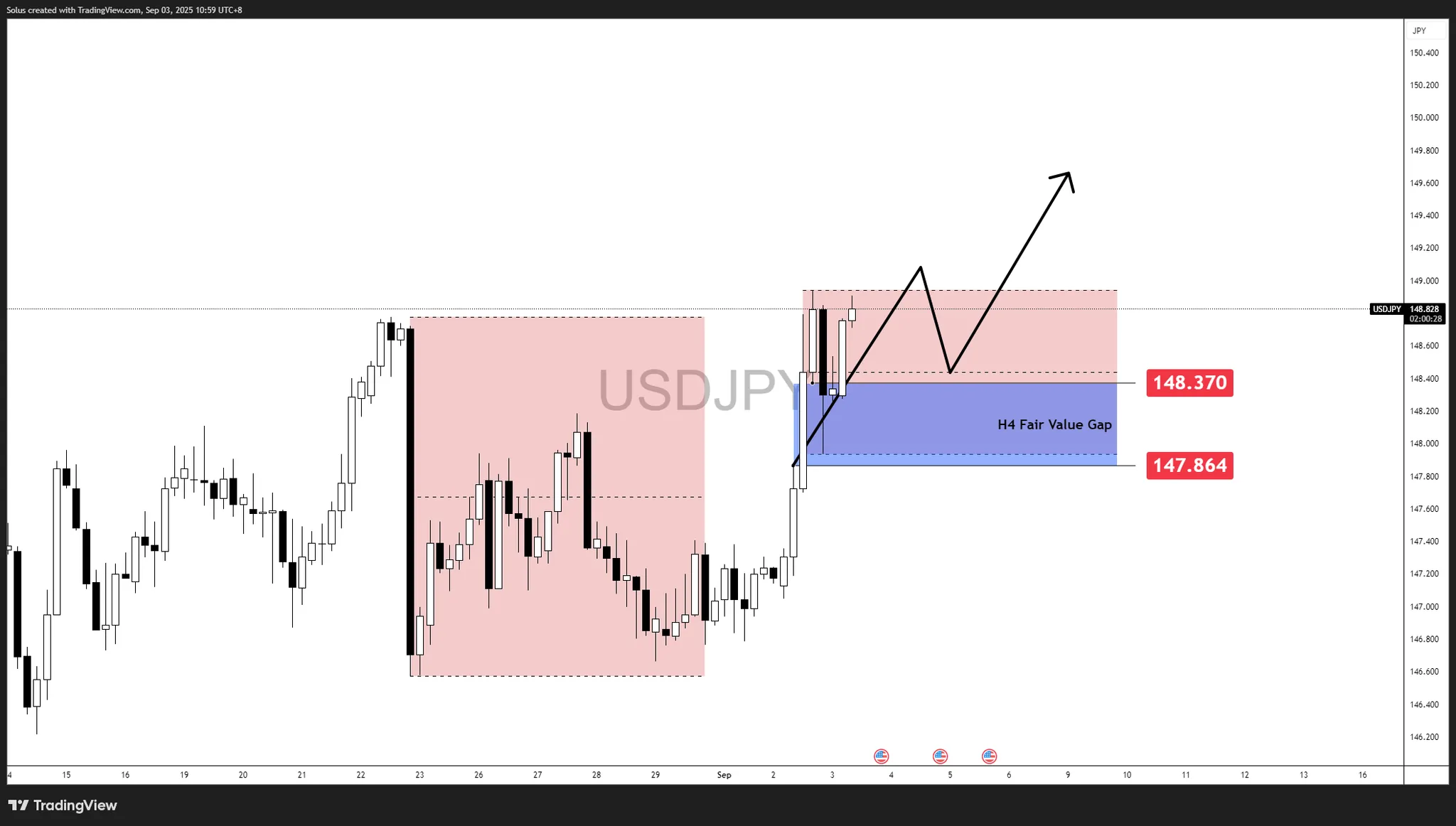

USD/JPY has bounced off the H4 FVG (147.864–148.370) decisively and pressing back into 148.80–149.00, where supply capped prior attempts. That reaction confirms active demand inside the gap and keeps the bullish structure intact into Friday’s data.

On the chart, price reacted cleanly from the H4 Fair Value Gap (147.864–148.370), confirming it as a demand zone. That bounce carried USD/JPY back into the 148.80–149.00 resistance band, where sellers capped momentum previously. If bulls can force a breakout above this zone, the path toward the psychological 150.00 handle opens up.

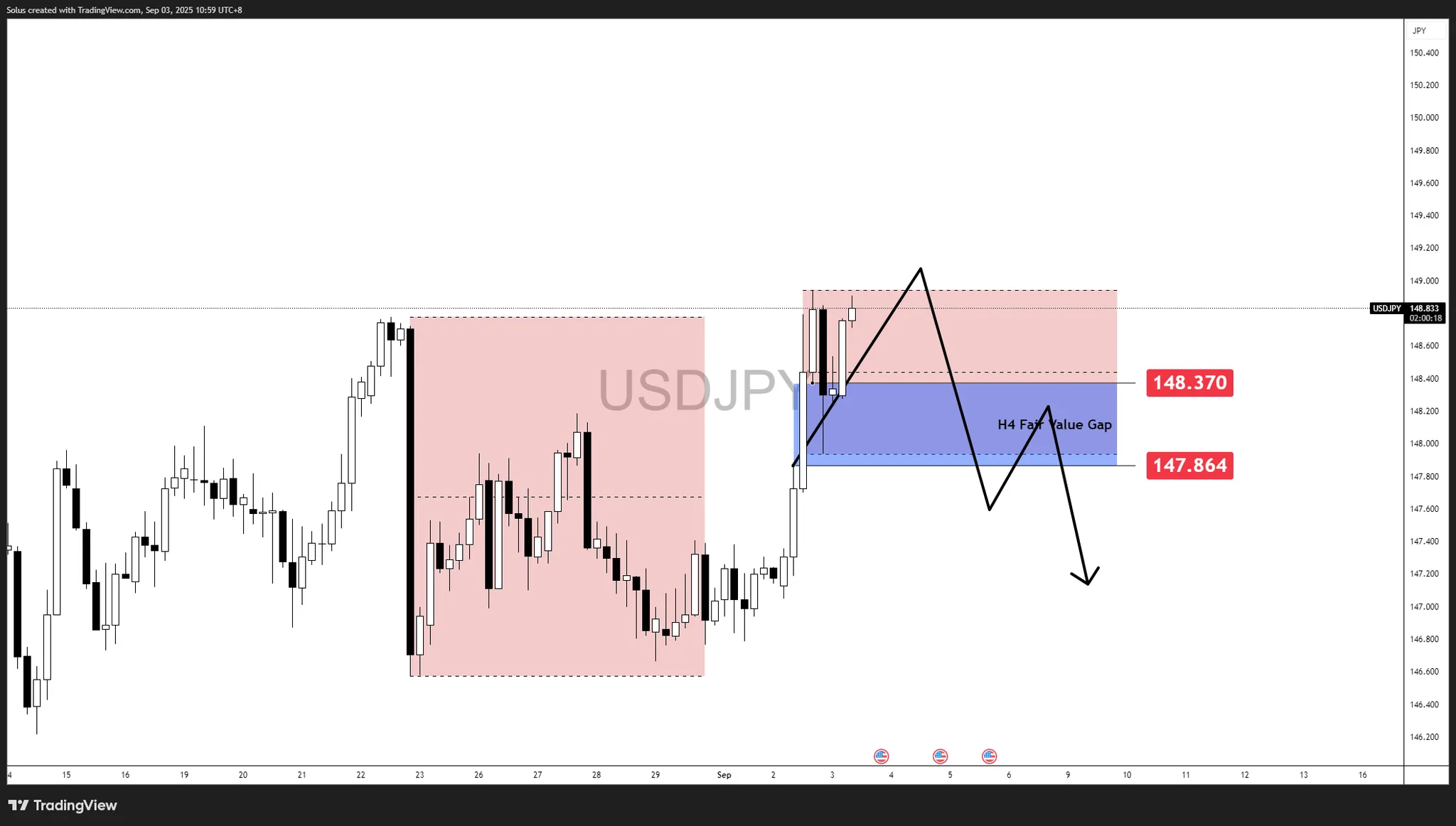

The same chart also highlights the risk: 149.00 is still acting as firm resistance. If price fails to clear this zone and prints rejection wicks or bearish engulfing patterns, sellers may regain control. That would likely send USD/JPY back into the H4 FVG (147.864–148.370) to test demand again.

Friday’s Nonfarm Payrolls (NFP) and Unemployment Rate will likely act as the catalyst that decides whether USD/JPY breaks cleanly above 149.00 or falls back into the H4 Fair Value Gap (147.864–148.370).

If headline NFP beats expectations (>75K) and unemployment holds steady or drops:

If NFP misses (<75K) and unemployment ticks up (>4.3%):

The chart highlights measured moves that preceded the triangle breakout, producing targets that match percentage gains of 11.4% and 18.4%, or price increases of $356 and $543. Using the $3,423 high as the breakout level, projected measured move targets sit at $3,779 and $3,966 based on price. These align with the continuation potential implied by the triangle formation.

Gold is now advancing toward the first target zone at $3,563 to $3,603, derived from a long-term 223.6% Fibonacci extension and a rising ABCD projection. Given the strength of the current trend, this zone may not provide significant resistance, though interim pauses cannot be ruled out. Key support rests at the prior breakout point of $3,500, followed by former swing highs at $3,451 and $3,439. Holding above these levels maintains the breakout structure and preserves bullish momentum.

Beyond the $3,603 zone, traders should watch for potential resistance around $3,664 to $3,668, where two indicators converge. While the higher measured move target near $3,966 could be reached longer term, shorter-term resistance zones may provide reaction points and consolidation phases along the way.

Gold confirmed a long-term bullish breakout last week, closing at its highest monthly level ever after overcoming resistance from the past two months. The last comparable rally out of consolidation produced four consecutive weeks of gains. With this being the first week of a new breakout phase, historical precedent suggests further upside is favored before the current move exhausts.

For a look at all of today’s economic events, check out our economic calendar.

The gold market is surging with an intensity not seen in years, smashing through the $3,500 level and printing a new all-time record. Spot gold (XAU/USD) peaked at $3,516.31 per ounce during Asian hours, surpassing April’s previous high of $3,500.05, before stabilizing near $3,491.47 in New York, still higher on the day. U.S. gold futures for December delivery advanced to $3,554.30, while intraday trades briefly touched $3,580. With prices up more than 33% year-to-date, bullion has doubled since early 2023, cementing itself as the market’s strongest performing safe-haven asset.

The rally is underpinned by the conviction that the Federal Reserve is preparing its first rate cut in nine months. Markets are pricing a 90% probability of a 25 bps cut on September 17, with some speculation of a 50 bps move if nonfarm payrolls later this week miss estimates. Trump’s repeated attacks on Fed Chair Jerome Powell and his attempt to oust Governor Lisa Cook have escalated fears of compromised independence. A federal appeals court ruling that Trump’s global tariffs were illegally imposed has further rattled confidence in the U.S. economic outlook. Analysts warn that the political overhang, combined with inflationary risks if the Fed bows to pressure, has created a near-perfect environment for higher gold.

Beyond macro policy, structural demand from sovereign buyers is reinforcing the surge. Central banks in India, China, Turkey, and Poland have been expanding reserves, with 2024 marking the year gold overtook the euro as the second-largest global reserve asset after the dollar. This “de-dollarization” trend continues into 2025, with foreign central banks’ U.S. Treasury allocations shrinking while gold holdings rise. SPDR Gold Trust (GLD), the world’s largest gold-backed ETF, reported a 1.01% increase in holdings last week to 977.68 tons, its highest since 2022. Indian pension funds are also seeking approval to add gold ETFs to portfolios, a sign that institutional allocations remain strong even at record levels.

Gold’s explosive rise reflects a confluence of geopolitical and macroeconomic risks. Trump’s escalating tariffs and rhetoric against trading partners have reignited global trade tensions, while the dollar index languishes near one-month lows. With the greenback under pressure, overseas buyers find gold cheaper, reinforcing momentum. European bond markets mirror this trend, with U.K. 30-year gilt yields hitting a 27-year high, French 30-year yields at a 16-year high, and German 30-year bonds at their costliest since 2011. Investors are fleeing sovereign debt, turning instead to gold and silver as defensive hedges. Geopolitical backdrops—from Russia’s war in Ukraine to ongoing Middle East volatility—layer additional urgency for diversification into bullion.

The timing of this breakout coincides with gold’s seasonally strongest demand window. Analysts at Standard Chartered project average prices of $3,500/oz in Q3 and $3,700/oz in Q4, underscoring that momentum may extend into year-end. China and India, historically price-sensitive, are seeing jewelry buyers pivot into investment-grade coins and bars instead of exiting at high prices. This shift keeps Asian consumption steady even at elevated levels. Combined with robust ETF inflows, the demand profile suggests current prices are not discouraging participation but rather reinforcing gold’s role as the asset of choice during uncertainty.

The surge in gold is mirrored by strength in silver, platinum, and palladium. Silver (XAG/USD) touched $40.64/oz, its highest since 2011, before settling near $40.48. Platinum trades at $1,389.75 and palladium at $1,121.75, both lower on the day but still supported by safe-haven flows. With the gold-silver ratio still above its historical range of 60–80, analysts argue silver has greater upside potential in relative terms. The synchronized rise in precious metals reinforces broad investor hedging strategies against monetary and geopolitical shocks.

Strategists from UBS, BNP Paribas, and Goldman Sachs see this as more than a seasonal move. Projections range from $3,700 by mid-2026 to $4,000 per ounce if Fed rate cuts multiply or political crises deepen. BNP’s David Wilson stressed that Trump’s overt challenge to Fed independence combined with U.S. fiscal deficits provides the “perfect setup” for further gold appreciation. Goldman Sachs highlighted ETF inflows as the hidden accelerant that could sustain the rally, projecting $4,000 in the next 12 months. The resilience of gold above $3,500 suggests markets are already positioning for this upper range.

Friday’s nonfarm payrolls is now the most critical data point. A weak print could reignite speculation of a 50 bps cut, fueling additional gains in XAU/USD. Even without such an aggressive move, the structural bid from central banks, ETF flows, and retail demand provides a strong base. Investors remain highly sensitive to Trump’s next move on Fed governance, with the market interpreting every headline as another justification to add bullion exposure.

With spot prices near $3,491.47 and futures around $3,554.30, gold has broken key technical resistance and entered uncharted territory. Strong central bank buying, ETF inflows, and macro uncertainty support continued upside. Risks lie in a potential Fed surprise of no cut, which could temporarily cap momentum, but structural demand and political instability provide a solid floor above $3,400.

Verdict: Buy. Gold’s trajectory toward $3,700 by Q4 2025 and possible tests of $4,000 in 2026 positions XAU/USD as the strongest hedge in global markets, with silver offering leveraged upside in parallel.

Image © Adobe Images

RBC Capital Markets expects the pound to remain resilient in the short term, with forecasts showing GBP/USD and GBP/EUR holding firm before edging higher into year-end.

“Sterling is not without challenges, but near-term resilience is underpinned by relative rate support,” RBC wrote in its August currency report.

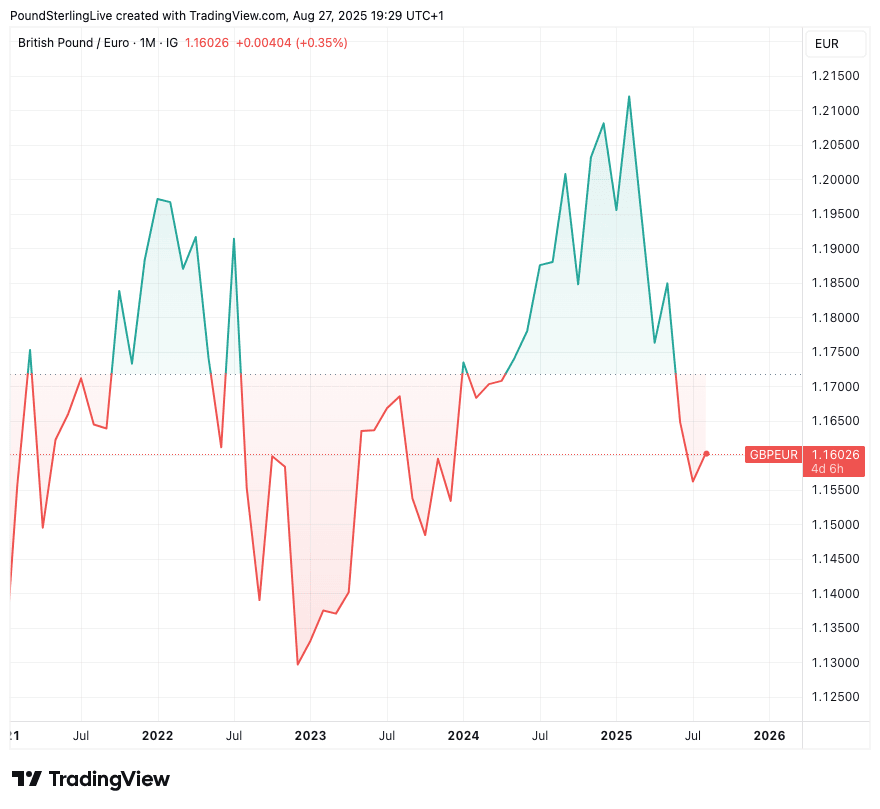

The Pound entered 2025 as the second-best performing G10 currency in the two previous years, and analysts had expected further outperformance over this year.

However, that strength failed to materialise and the consensus forecast for the third and fourth quarters of the year has been lowered.

Pound Sterling Live consistently delivers stronger rates than major UK banks.

In July, you could have saved up to €1,720 on a £50,000 transfer thanks to our competitive pricing.

Based on average GBP/EUR rates observed in July.

A run of disappointing economic data that includes rising unemployment and inflation are key culprits behind the GBP’s failure to live up to earlier expectations.

But, by RBC’s reckoning, disappointing economic growth is now well understood by the market and incorporated into the price of Pound Sterling.

“Markets are prepared for weaker UK activity, which limits the scope for a significant repricing lower in GBP,” the report added.

The report argues that resilience seen through August reflects the Bank of England’s more cautious approach to policy easing compared with peers, with money markets now showing investors no longer see another interest rate cut at the Bank of England on the menu for the remainder of the year.

RBC adds that positioning is favourable, with a neutral market position (sell and buy contracts in the options market roughly similar) leaves room for fresh Sterling inflows if global sentiment steadies.

RBC expects the pound to outperform higher beta G10 currencies like AUD and NZD if global growth weakens in line with forecasts.

The bank now forecasts the Pound to Dollar exchange rate at 1.37 by the fourth quarter of 2025, compared with 1.36 currently, reflecting relative monetary policy support.

Against the euro, RBC expects EUR/GBP to ease to 0.85 by the fourth quarter, consistent with sterling retaining relative strength over the coming months.

This translates into a Pound to Euro exchange rate of 1.1765, up from the level of 1.16 at the time of writing. (You can book your target rate with an automatic order).

“We think GBP has relative defensive value within G10, which should allow it to outperform the more cyclical FX bloc,” the report said.

Above: After two years of gains, GBP/EUR has entered a period of softer trade.

Longer term, however, the bank remains cautious on sterling’s prospects, citing structural economic weaknesses.

“Near-term resilience does not change our longer-term view that structural imbalances will weigh on GBP,” RBC concluded.

The bank also warns that higher energy prices or looser fiscal policy could revive downside risks for the currency.

“Energy costs remain a structural vulnerability for the UK economy and could cap sterling upside if they flare again,” RBC wrote.

As of Wednesday, GBP/USD was trading at 1.3602 (+0.05%), EUR/GBP at 0.8574 (-0.02%), and GBP/JPY at 198.95 (+0.08%).

The British pound collapsed against the U.S. dollar, with GBP/USD falling as much as 1.2% intraday and erasing all the gains it posted after Jerome Powell’s dovish Jackson Hole speech on August 22. At the core of the decline sits the violent repricing of UK sovereign debt, where the 30-year gilt yield spiked to 5.69%, a level not seen since March 1998. That surge reflects growing concern over Chancellor Rachel Reeves’ heavy borrowing plans, ballooning deficits, and the heightened risk premium demanded by investors. The market drawdown draws strong parallels with the 2022 gilt crisis triggered by Liz Truss’s “mini-budget,” where unsustainable fiscal policy shattered confidence and sparked a sterling free-fall.

On the technical front, GBP/USD slipped under its key moving averages, with the pair now trading below both the 20-day and 50-day levels. The 4-hour RSI sits deep in oversold territory, below 30, yet momentum remains bearish. Bears are targeting the medium-term pivotal zone between 1.3315 and 1.3280, defined by the 61.8% Fibonacci retracement of the early August rally and the ascending trendline from the January 13 low. Immediate resistance rests at 1.3460, and only a break above that level would neutralize the near-term bearish tone. If the pair pierces 1.3315 decisively, the path opens toward 1.3200 and potentially 1.3130, completing a deeper A-B-C-D bearish structure that has been unfolding since July.

The market’s message is blunt: sterling’s weakness is driven by fiscal credibility fears. With borrowing costs surging, Reeves’ need to raise funds has unsettled gilt buyers who demand higher yields for long-dated paper. In April, revenues collapsed by more than 20% compared to last year, and the UK budget deficit continues to widen. Investors now view the Autumn Budget as a flashpoint for renewed volatility, with questions over whether Reeves can stabilize debt trajectories without aggressive tax hikes or spending cuts. As of September 2, sterling remains the weakest among major currencies on a rolling one-day basis, with the dollar posting a 1.1% gain versus GBP.

Sterling’s slide is compounded by U.S. momentum. The Dollar Index (DXY) bounced back to 98.19, recovering from 97.54, bolstered by geopolitical safe-haven demand and anticipation of fresh PMI data. August’s ISM Manufacturing PMI is projected at 49.0, up from 48.0, with the Prices Paid component at 65.1 versus 64.8 prior. Friday’s nonfarm payrolls report looms even larger, with forecasts calling for a 75,000 job gain and unemployment at 4.3%. Traders assign an 89% probability of a September Fed rate cut, but strong employment could delay deeper easing. For now, the Fed’s trajectory and Trump’s attacks on the central bank’s independence add to dollar volatility, yet GBP/USD remains skewed to the downside as long as the UK’s fiscal credibility is under attack.

Trading signals reflect that the bearish camp has regained firm control. Short positions are favored between 1.3520 and 1.3550, with stops just above 1.3570. Profit-taking zones stretch toward 1.3400, 1.3315, and 1.3280, with the latter forming the fulcrum of the medium-term outlook. A counter-trend long trade would only become attractive if GBP/USD breaks and holds above 1.3560, a threshold that would re-target the 1.3590–1.3639 zone. Market internals, however, suggest that such a bullish reversal is unlikely given the bond market rout. Liquidity grab patterns and repeated failures to hold above August’s breakout levels underscore the dominance of sellers.

Sterling’s volatility is not isolated. Broader markets show gold rallying past $3,500 per ounce, the euro firming against the dollar, and U.S. yields bouncing on tariff headlines. In this global environment, GBP/USD lacks domestic support, with manufacturing PMI contracting at 47.0 for August compared with July’s 48.0. Meanwhile, dollar resilience is reinforced by global safe-haven flows as Eastern Europe tensions escalate. Unless UK policymakers restore credibility, the market will continue to test sterling’s lower bounds. The two-week high at 1.3540 posted earlier in the week has already been rejected, and key resistance at 1.3590 remains intact. With the fiscal story dominant, the near-term outlook remains bearish, pointing to continued downside pressure until gilt yields stabilize.

The euro has fallen pretty significantly during the early hours here on Tuesday, as we have seen a continuation of the sideways action. With that being said, this is a market that I think continues to be somewhat noisy and somewhat rudderless, if you will. But we do have a range that we seem to be following. We have the 1.16 level offering support right along with the 50-day EMA now. But we have significant resistance near the 1.1750 level, followed by the 1.18 level. While I don’t necessarily expect a big move, I do expect to see continued stubbornness out of the US dollar through the week, really, due to the jobs number coming out on Friday.

The US dollar has rallied quite nicely against the Japanese yen, slamming right back into that 148.50 level. The question is, can we take off from here? If we can, it opens up a move to the 151 yen region, perhaps even higher than that. This is a strong candle, and it is a good sign, but the question is, can we follow through on the momentum? That might be a bit more difficult than imagined, but it is worth noting that after we fell apart there, we went sideways. We just sat still. And sometimes markets are about where they won’t go. In this case, they don’t seem to want to go down.

The coffee price ended its last bullish rally by surpassing the barrier at 370.60, confirming its move to a new positive station by recording 390.30 level, which forces it to form some sideways trading due to stochastic exit from the overbought level as appears in the above image.

Therefore, we will keep waiting for the positive momentum, which allows it to settle above 370.00 level, then begin targeting extra positive stations by reaching 400.55 and 411.20.

The expected trading range for today is between 375.00 and 400.00

Trend forecast: Bullish

The GBP/USD price analysis indicates escalating concerns about the UK’s fiscal health, which is weighing on bonds and the pound. Meanwhile, traders are gearing up for the crucial US monthly employment report, which will shape the outlook for Fed rate cuts.

–Are you interested in learning more about forex indicators? Check our detailed guide-

The UK 30-year yield rose to its highest point since May 1998 amid worries about UK finances. As a result, the pound collapsed. The government has to balance heavy borrowing, a weak economy, and high inflation. However, investors have lost some confidence. Therefore, sterling could face a lot of downward pressure ahead of the next budget reading.

“While a repricing of Bank of England expectations had helped sterling last month, the UK is going to be vulnerable to fiscal risks as the autumn budget approaches, which is likely to remain a headwind for sterling,” said Rabobank’s head of FX strategy, Jane Foley.

Elsewhere, the US will release its nonfarm payrolls report on Friday, showing the state of the labor market. Further weakness could revive bets for a 50-bps cut. On the other hand, if the sector is resilient, rate cut expectations will ease.

On the technical side, the GBP/USD price has collapsed and is on the verge of breaking below the 1.3401 key support level. It trades well below the 30-SMA, showing bears are in the lead. At the same time, the RSI has dipped into the oversold region, indicating solid bearish momentum. Bears took over after bulls failed to continue the previous rally.

–Are you interested in learning more about next cryptocurrency to explode? Check our detailed guide-

Although price action showed solid bullish momentum, the price remained in a corrective move, chopping through the 30-SMA. Bulls struggled to detach from the SMA and retest the 1.3575 key resistance level. As a result, bears returned and made an impulsive move below the SMA.

A break below the 1.3401 support would solidify the bearish bias. Moreover, it would allow GBP/USD to retest the 1.3200 support level. On the other hand, if the support holds firm, bulls will return to target the 1.3575 resistance level.

Looking to trade forex now? Invest at eToro!

68% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Gold has quickly reversed an uptick to fresh all-time-highs above $3,500, gathering pace for a sustained move again above that level. All eyes now turn to the US ISM Manufacturing PMI due later in the day for further trading directives.

Gold extends its bullish momentum into a sixth straight day, but the further upside appears capped (for now), in the face of a resurgent buying interest in the US Dollar (USD).

The USD sees a short-covering bounce from over one-month troughs across the board, driven by profit taking, as traders cash in before the releases of crucial US business surveys and employment data due this week.

The US ISM Manufacturing PMI is on the radar next as speculations over a jumbo interest rate cut by the US Federal Reserve (Fed) this month grow. A 25 basis points (bps) September rate cut is fully baked in, with the CME Group’s Fed Watch Tool showing a 90% chance.

The headline ISM Manufacturing PMI is expected to advance to 49 in August from 48 in July, remaining in contraction.

On the data disappointment, the Greenback could come under renewed selling pressure, keeping the record rally in Gold alive.

Additionally, concerns over the Fed’s autonomy amidst US President Donald Trump’s continued efforts to rope in more dovish appointments to the US central bank remain a drag on the USD, while supporting the bright metal.

The geopolitical developments between Russia and Ukraine also remain in focus, underpinning the traditional safe-haven Gold. On Sunday, Ukraine’s President Volodymyr Zelenskiy said Ukraine plans new strikes deep into Russia after weeks of intensified attacks on Russian energy assets, per Reuters.

Trump noted last week that he was deeply disappointed, particularly in light of his recent attempts to mediate between Russia and Ukraine to bring an end to the war.

The daily chart shows that Gold eyes more upside as the 14-day Relative Strength Index (RSI) is still not heavily overbought. The leading indicator is currently near 71.

The Bull Cross of the 21-day Simple Moving Average (SMA) and the 50-day SMA also keeps the buoyant tone intact around the bullion.

The immediate topside hurdle is seen at the new record high of $,3509, above which the $3,550 psychological level will be challenged.

Conversely, any pullback will challenge the intraday of $3,475 initially, followed by this week’s low of $3,437.

The $3,400 round level will be attacked on a sustained break below the latter.

The Institute for Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI), released on a monthly basis, is a leading indicator gauging business activity in the US manufacturing sector. The indicator is obtained from a survey of manufacturing supply executives based on information they have collected within their respective organizations. Survey responses reflect the change, if any, in the current month compared to the previous month. A reading above 50 indicates that the manufacturing economy is generally expanding, a bullish sign for the US Dollar (USD). A reading below 50 signals that factory activity is generally declining, which is seen as bearish for USD.

Price Forecast: Extends Record Run, Targets Higher Levels Ahead")