The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

The main category of Forex News.

You can use the search box below to find what you need.

[wd_asp id=1]

For the second consecutive session, the 78.6% Fibonacci retracement at $4.41 has capped upside, just shy of the 161.8% projected target of the rising ABCD pattern at $4.45. This creates a defined $4.41–$4.45 resistance band. The extended top channel line runs straight through the heart of the current four-day consolidation range as well, adding another indicator showing of overhead supply.

The intraday reversal today strongly favors an inside day close heading into next week, fully contained within a developing four-day topping pattern. A drop below Friday’s $4.27 low would flash immediate weakness, but a bearish reversal only confirms on a decisive break beneath the four-day range support at $4.18.

Natural gas continues to demonstrate resilience near the highs while repeatedly challenging resistance, reflecting sustained buyer interest. This dynamic raises the possibility that one more push higher could materialize before any pullback unfolds. And when correction does arrive, it may remain shallow and short-lived. This is not a prediction, merely a scenario to keep in view.

Strength reasserts on any rally above the $4.42 trend high established Friday, with the $4.45 ABCD completion as the immediate next objective. A clean, decisive advance through $4.45 would signal the rising trend retains momentum and may have additional upside legs ahead.

First dynamic support arrives at the 10-day moving average, currently $4.01 and rising. Just below sits the 38.2% Fibonacci retracement at $3.94, converging with the original rising channel top line—previously resistance and now an untested potential support zone following the recent breakout above it.

The $4.41–$4.45 resistance zone holds the near-term key. Persistent failure here likely forces a deeper test of support the four-day range toward $4.18, with $4.01–$3.94 as the follow-on support cluster. A breakout above $4.45, however, validates continuation within the broader channel and opens higher targets. The inside day resolution may provide the next critical directional signal.

– Written by

Ben Hughes

STORY LINK Euro to Dollar Forecast: EUR/USD Nears 1.16 on US Job Market Worries

The Euro to Dollar (EUR/USD) exchange rate rebounded strongly above 1.15 after disappointing US jobs figures triggered renewed selling in the dollar.

ING analysts suggest a key low may have formed near 1.1470, though analysts warn that confirmation will depend on further clarity over the US labour market.

The Euro moved back above the 1.1500 level against the Dollar after weak US jobs data on Thursday and made further headway on Friday with 1-week highs close to 1.1560.

According to ING; “There is a chance that EUR/USD may have established an important low at 1.1470 this week. But for a rally to unfold, we will probably need to get more clarity on the slowing US jobs market. Let’s see whether intra-day support at 1.1500/1510 can now hold.”

UOB commented; “the EUR’s weakness from a week ago has stabilised, and we expect EUR to trade in a range of 1.1485/1.1610 for the time being.

Challenger reported that layoffs in October surged 175% from a year ago to 153,074, the highest October figure for 20 years. For the first 10 months of the year, layoffs increased 65% to near 1.1mn.

Get better rates and lower fees on your next international money transfer.

Compare TorFX with top UK banks in seconds and see how much you could save.

ING noted the weak data, but added; “with the US government shutdown ongoing, we are still in the dark about the true labour market picture.”

Jeffries economist Mohit Kumar noted the scarcity of data; “With the December Fed meeting more or less a coin toss which crucially depends on the labour market picture, the market is overreacting to any hints about the labour market.”

Markets are pricing in just over a 65% chance of a further Fed rate cut at the December meeting.

MUFG noted the impact of uncertainty; “The Fed has indicated that it would prefer to leave rates on hold in December if they are unable to gain more clarity on the health of the US economy and labour market by then.”

The US government shutdown has still not been resolved.

MUFG added; “The timing of when the record government shutdown comes to an end remains important for US dollar performance.”

The US currency will be vulnerable if there is convincing evidence of a weaker labour market.

The Euro could still face challenges surrounding the global economy with markets also digesting the outlook for US tariffs.

ING commented; “While we like the idea of a weaker dollar and a stronger EUR/USD, last night’s Chinese trade data is unwelcome news. It suggests China might not have as easily diversified its exports away from the US as first thought – or at least the ex-US demand is insufficient to offset the loss of the US market. That will only add to fears of increasing Chinese pressure in European markets.”

International Money Transfer? Ask our resident FX expert a money transfer question or try John’s new, free, no-obligation personal service! ,where he helps every step of the way,

ensuring you get the best exchange rates on your currency requirements.

TAGS: Euro Dollar Forecasts

Unicredit Tower A, Milan © Sergio Fabio Brivio, Flickr

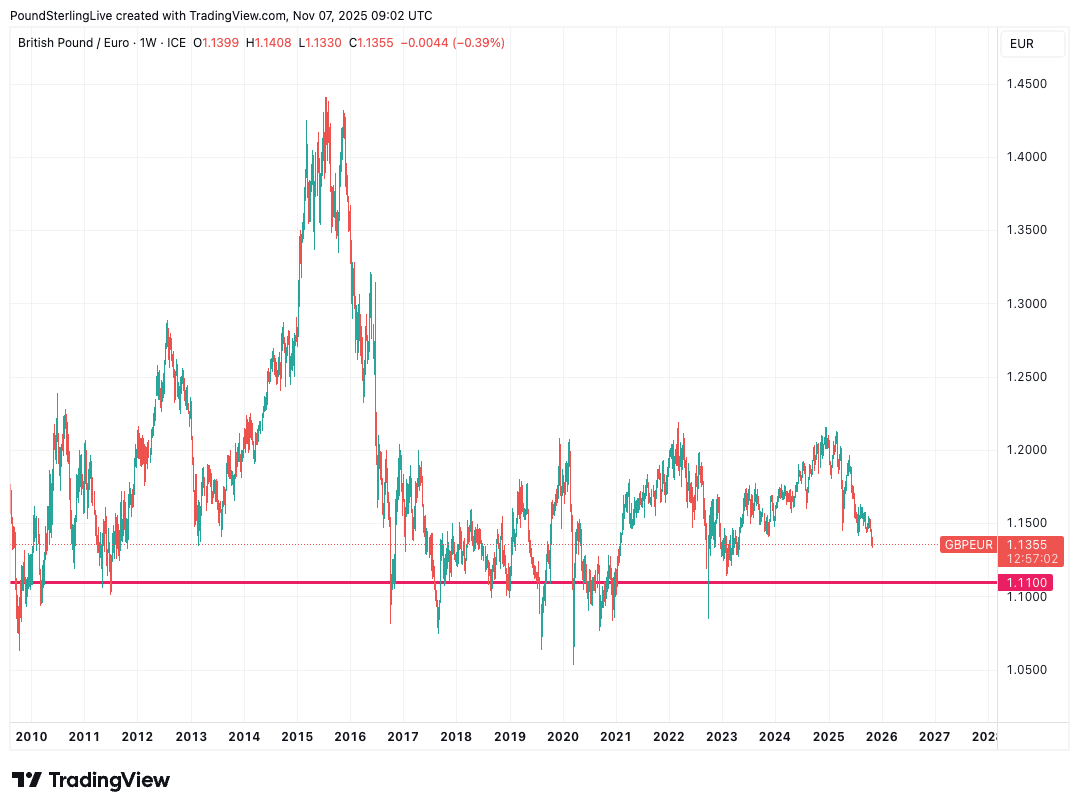

The market is underestimating how far and fast the Bank of England will cut interest rates, which will weigh materially on the pound to euro exchange rate, says a leading global investment bank.

“We see more and faster rate cuts than markets,” says Daniel Vernazza, Chief International Economist at UniCredit in London.

The market is currently anticipating two more reductions in Bank Rate during this cycle, taking it to 3.5%.

This expectation was reinforced by Thursday’s decision to leave interest rates unchanged at 4.0% but signal in clear terms that another cut was imminent. Most economists think the tone adopted by the Bank points to a cut at December’s meeting.

However, UniCredit expects the labour market to continue to weaken and consumption growth to remain soft, reinforced by the likely material tightening of fiscal policy in the upcoming Autumn Budget.

The government looks all but set to raise the basic rate of income tax for the first time since the 1970s, which economists say will squeeze the economy and pressure inflation.

“Inflation should move down to 2% next year. In this environment, we expect the MPC to cut rates in December, followed by a quarterly pace of rate cuts next year to 2.75%,” says Vernazza.

The Bank of England’s November Monetary Policy Report revealed forecasts showing it expects inflation to fall back to the 2.0% target much later, in late 2027.

The Bank’s latest forecasts also show it is modelling the economic outlook on the market’s assumption that Bank Rate will fall to a terminal rate at 3.5% next year.

Foreign exchange markets are responsive to interest rate expectations, meaning the pound would decline in the event that the market adjusts to UniCredit’s thinking on inflation and the more aggressive path of cuts that the Bank of England would respond with.

If the Milan-based lender is correct, a significant repricing in market interest rate expectations awaits, which will drag materially on the pound.

Given this, UniCredit holds a pound to euro forecast of 1.11, which is well below the consensus of predictions made by its peer investment banks.

Above: 1.11 is the bottom of a long-term range for GBP/EUR.

The Pound Sterling (GBP) extended its downtrend and reached seven-month lows near 1.3000 against the US Dollar (USD), before GBP/USD buyers quickly jumped in and recovered some ground.

Safe-haven flows returned with a bang and acted as a strong headwind to the risk-sensitive Pound Sterling while boosting the US Dollar to its highest in five months against its six major currency rivals.

“Sell everything” theme gripped the market as traders witnessed a wave of exhaustion following the Artificial Intelligence (AI) driven record rally in global stocks. US tech stocks tumbled, drowning the major indices, with investors selling Gold to cover their losses in equity markets.

Investors grew concerned over inflated technology stock valuations, particularly in the artificial intelligence (AI) space, fuelling the long-due correction in global indices.

That being said, the USD also found fresh support from reduced expectations that the US Federal Reserve (Fed) will deliver another interest rate cut in December. The December Fed rate cut bets were slashed after strong US private sector employment and services activity data.

Data published by the ADP showed that US private payrolls increased by 42,000 jobs in October, exceeding expectations of a 25,000 gain, while the ISM Services PMI increased more than expected to 52.4 last month due to a solid jump in New Orders.

This broad USD strength smashed the GBP/USD pair to challenge the 1.3000 psychological level before it staged a decent comeback in the latter part of the week.

Cable’s turnaround was mainly driven by a sharp pullback in the USD across the board and US Treasury bond yields, following Thursday’s private labor data and resurfacing concerns over a protracted government shutdown.

The executive outplacement firm Challenger, Gray & Christmas said on Thursday that corporations announced a 183.1% monthly surge in layoffs, the worst October in over two decades, per Reuters.

The latest jobs data refuelled concerns about the weakening US labor market conditions, slightly boosting the odds of the Fed rate cut next month to 69% versus a drop to 62% seen after the release of the US ADP Employment Change data.

The recovery in GBP/USD was unfazed by the Bank of England’s (BoE) dovish hold decision. The members of the BoE Monetary Policy Committee (MPC) voted 5-4 to maintain the key Bank Rate at 4%, in a narrower than expected split.

The BOE underscored that future rate cuts will depend on the evolution of the outlook for inflation. “If progress on disinflation continues, Bank Rate is likely to continue on a gradual downward path,” the Monetary Policy Statement (MPS) said.

Heading into the weekend, the USD came under renewed selling pressure and helped GBP/USD stretch higher. The monthly report published by the University of Michigan (UoM) showed that the Consumer Sentiment Index dropped to 50.3 in November from 53.6 in October.

Amid a holiday-shortened week, the data drought from the United States (US) will likely continue as no end in sight to the government shutdown.

The longest shutdown in American history will put the focus back on some private-sector statistics and speeches from Fed officials. In case the government funding is restored, the delayed US Nonfarm Payrolls and Jobless Claims will be eagerly awaited.

The US Consumer Price Index (CPI), Producer Price Index (PPI) and Retail Sales reports for October will also be in focus.

From the United Kingdom’s (UK) economic calendar, the employment data on Tuesday will offer some incentives to Pound Sterling traders.

On Wednesday, BoE Chief Economist Huw Pill is due to speak in a panel discussion titled “An assessment of the BoE’s reaction to Covid-19” at the Institute of International Monetary Research Conference hosted by the University of Buckingham.

Thursday will feature the monthly and preliminary reading of the British third-quarter Gross Domestic Product (GDP) data alongside the industrial figures.

As observed on the daily chart, GBP/USD is struggling at the previous strong support-turned-resistance at 1.3142 on the road to recovery.

The 14-day Relative Strength Index (RSI) has turned lower while below the midline, currently near 36, suggesting that more downside remains on the cards.

Adding credence to the bearish potential, the 21-day Simple Moving Average (SMA) is looking to close the week below the 200-day SMA, which will confirm a Bear Cross if that happens.

These technical indicators point to more pain for the GBP/USD pair heading into a new week.

If the abovementioned resistance is scaled decisively, powerful resistance will then align around the 1.3265 region, where the Aug 4 low, the 21-day and 200-day SMA close in.

A sustained move above that zone will unleash additional recovery toward the 50-day SMA barrier at 1.3393.

Conversely, if the downside regains momentum, a test of the multi-month troughs at 1.3010 will be inevitable.

Selling pressure will intensify below the latter, opening the door toward the April 11 low of 1.2967.

The last line of defense for Pound Sterling buyers is seen at the 1.2850 psychological level.

The Gross Domestic Product (GDP), released by the Office for National Statistics on a monthly and quarterly basis, is a measure of the total value of all goods and services produced in the UK during a given period. The GDP is considered as the main measure of UK economic activity. The QoQ reading compares economic activity in the reference quarter to the previous quarter. Generally, a rise in this indicator is bullish for the Pound Sterling (GBP), while a low reading is seen as bearish.

The gold market reclaimed ground on Thursday, with spot XAU/USD trading near $4,012 per ounce, up 0.8% intraday, after rebounding from an early Asian-session dip to $3,970. The yellow metal has stabilized above the $4,000 psychological threshold, defying recent profit-taking and positioning shifts, as macro forces—from a weakening dollar to record central bank demand—reassert gold’s dominance as the most resilient asset of 2025.

Gold’s immediate rebound was triggered by the U.S. Dollar Index (DXY) slipping 0.3% to 106.04, down from a four-month high earlier this week, and the 10-year Treasury yield declining over 5 basis points to 4.106%, while the 2-year yield slid to 3.578%. This easing in yields restored appetite for non-yielding assets such as gold, which surged back above $4,000 for the first time since late October.

The broader catalyst came from deteriorating U.S. labor data. The Challenger, Gray & Christmas report revealed 153,074 job cuts in October, the highest October total since 2003, amplifying concerns over a slowing U.S. economy and reinforcing speculation of renewed Federal Reserve easing into early 2026. Although the ADP report posted a surprise +42,000 job gain, the private data’s optimism was offset by a 37-day federal shutdown delaying official statistics. This combination of mixed labor signals and fiscal paralysis has created a volatile yet gold-supportive environment.

Technically, gold is attempting to clear a critical resistance area near $4,046.60, which corresponds to the October 31 swing high. A successful breakout above this zone would activate the 50%–61.8% Fibonacci retracement range between $4,133.95 and $4,192.36, unlocking potential upside targets at $4,200 (UBS base case) and $4,700–$5,000 in extended scenarios.

Support remains solid between $3,867.95 and $3,846.50, anchored by the 50-day moving average and prior double-bottom pattern formed at $3,928.68 and $3,886.46. As long as price action holds above these pivot levels, the primary trend remains bullish, even amid short-term consolidations.

From a momentum standpoint, RSI readings near 54–56 on the daily chart indicate a recovery from oversold conditions observed last week. Volume analysis confirms renewed accumulation, with COMEX futures open interest rising 2.4% after a week of heavy liquidation. This shift marks an early re-entry of institutional traders after October’s correction.

Institutional sentiment across global banks remains overwhelmingly bullish despite the recent drawdown. UBS, in its November 3 report, reaffirmed a base target of $4,200/oz and an optimistic path toward $4,700/oz in Q1 2026, citing lower real rates, weaker dollar prospects, and persistent geopolitical risk. Strategist Sagar Khandelwal emphasized that “outside of technical factors, there is no fundamental justification for the sell-off.”

ING’s Ewa Manthey echoed the stance, stressing that “key supports, including central bank and safe-haven demand, remain fully intact.” ING projects an average price of $4,000 in Q4 2025 and $4,100 in Q1 2026, with downside “limited and short-lived.” The Dutch bank sees 70% odds of a December Fed rate cut, which would enhance gold’s non-yielding appeal.

Meanwhile, Goldman Sachs expects $5,055 by Q4 2026, Bank of America targets $5,000 with $4,400 average, and HSBC forecasts $5,000 by end-2026, all citing de-dollarization and record physical demand. The World Gold Council (WGC) reported 1,313 tonnes of global demand in Q3 2025, a record quarter driven by 222 tonnes of ETF inflows and 316 tonnes of bar and coin investment—a 47% year-over-year surge.

Gold’s long-term floor is underpinned by massive institutional and sovereign accumulation. Central banks purchased over 800 tonnes of gold in 2024, following the record 1,136 tonnes in 2022, while UBS now forecasts 900–950 tonnes for 2025. This buying spree, led by China, India, and Turkey, reflects a broader structural trend of de-dollarization as nations hedge against U.S. fiscal uncertainty and sanctions exposure.

ETF participation confirms the same pattern. In Q3 alone, inflows reached $24 billion, the strongest quarter in history, with North America leading with 346 tonnes and Europe adding 148 tonnes. Cumulative 2025 inflows now exceed 619 tonnes ($64 billion). The World Gold Council’s data shows retail bar and coin demand at 316 tonnes, while jewelry demand, though down 19% YoY to 371 tonnes, increased 13% in value to $41 billion, underscoring how high prices are not deterring overall wealth allocation to gold.

Across Asia, physical markets remain firm. In India, gold prices climbed on November 6 to ₹11,225 per gram for 22K and ₹11,786 per gram for 24K, up ₹40–₹42 day-over-day, confirming that consumer demand remains strong despite elevated levels. In China, premium spreads between Shanghai and London gold prices exceeded $65/oz, indicating supply tightness amid record retail buying during Diwali and year-end festival demand.

This strength in Asia offsets temporary softness in Western ETF reallocation, keeping the global demand base balanced. With India’s imports surging and jewelry fabrication margins stable, analysts expect South Asian markets to remain pivotal in absorbing supply even if speculative flows waver in futures.

The U.S. government shutdown, now in its 37th day, has distorted economic data visibility and delayed official inflation and employment reports. Traders are forced to rely on private indicators like ADP and ISM, both of which have shown resilience. However, with core CPI still above 3.5% YoY and fiscal uncertainty persisting, real yields are trending lower—a historically bullish condition for gold.

Fed fund futures currently price a 63% probability of a December rate cut, down from 90% last week, but markets broadly agree that the Fed’s hiking cycle is over. Lower real yields combined with global geopolitical strains—from Middle East tensions to Europe’s energy crunch—create an environment favoring continued safe-haven demand.

Applying Fibonacci projections to the August–October uptrend suggests a 100% extension target near $5,000/oz and a 161.8% level at $5,600/oz, implying over 40% potential upside from current levels. The $3,800–$3,900 area remains a historically strong accumulation zone, confirmed by multiple retests and alignment with the 50-day EMA.

Volatility in COMEX gold options has contracted to 13.8% implied volatility, near a three-month low, signaling that the market may be coiling for a major directional move. Option traders are positioning for a volatility breakout, with call open interest surging at the $4,200 and $4,500 strikes—consistent with institutional forecasts of a year-end rally.

Sentiment analysis shows 70% of institutional portfolios remain underweight gold, leaving room for reallocation. UBS explicitly recommended “buying the dip,” advising 3–7% portfolio exposure to gold and select exposure to mining equities, which they expect to outperform bullion over the next six months due to operating leverage.

From a trading perspective, maintaining long exposure above $3,950 with stop-loss below $3,870 and profit targets at $4,130–$4,190 aligns with short-term bullish momentum. Options traders are accumulating December $4,100 calls and selling $3,900 puts, reflecting confidence that the downside remains contained.

All structural indicators point toward strength rather than fragility. The correction from $4,381 to $3,970 represented a mere 8.4% decline, well within normal retracement parameters following a 47% YTD surge. With Treasury yields falling, ETF inflows accelerating, and central banks accumulating, the medium-term trajectory remains decisively bullish.

Gold’s immediate bias: BUY above $3,950, target range $4,200–$4,700, and extended objective $5,600 by late 2026. The longer the government shutdown persists and liquidity tightens in equities, the stronger the magnet toward higher gold valuations becomes.

XAU/USD remains the cornerstone of global risk hedging—and as fundamentals align, it’s again proving why every dip in the world’s oldest asset becomes a launchpad for the next rally.

EUR/USD stays in a consolidation phase above 1.1500 in the European session on Friday after rising nearly 0.5% on Thursday. As market participants await the University of Michigan’s (UoM) Consumer Sentiment data for November, the pair’s technical outlook highlights buyers’ hesitancy.

The table below shows the percentage change of Euro (EUR) against listed major currencies this week. Euro was the weakest against the Japanese Yen.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.01% | 0.14% | -0.40% | 0.74% | 0.95% | 2.11% | 0.39% | |

| EUR | 0.01% | 0.16% | -0.28% | 0.75% | 0.95% | 2.13% | 0.40% | |

| GBP | -0.14% | -0.16% | -0.60% | 0.59% | 0.79% | 1.96% | 0.24% | |

| JPY | 0.40% | 0.28% | 0.60% | 1.09% | 1.32% | 2.49% | 0.90% | |

| CAD | -0.74% | -0.75% | -0.59% | -1.09% | 0.15% | 1.34% | -0.33% | |

| AUD | -0.95% | -0.95% | -0.79% | -1.32% | -0.15% | 1.17% | -0.51% | |

| NZD | -2.11% | -2.13% | -1.96% | -2.49% | -1.34% | -1.17% | -1.69% | |

| CHF | -0.39% | -0.40% | -0.24% | -0.90% | 0.33% | 0.51% | 1.69% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent EUR (base)/USD (quote).

In the absence of the official employment report, because of the ongoing government shutdown in the US, investors scrutinize data that could provide fresh insights into the labor market conditions.

On Thursday, Challenger, Gray & Christmas reported that US-based employers cut more than 150,000 jobs in October. This marked the biggest reduction for the month in over two decades. The underlying details of the publication showed that tech firms, retailers and the services sector led the job cuts in this period. With this report reviving concerns over worsening conditions in the labor market, the USD came under selling pressure on Thursday and helped EUR/USD push higher.

Early Friday, the USD corrects higher and limits EUR/USD’s upside. In the second half of the day, markets will pay close attention to the UoM Consumer Sentiment data. A noticeable deterioration in consumer confidence could make it difficult for the USD to stay resilient against its rivals heading into the weekend. On the other hand, an improvement in the headline print, combined with an uptick in the 1-year Consumer Inflation Expectations component of the report, could support the USD and weigh on EUR/USD.

The Relative Strength Index (RSI) indicator on the 4-hour chart declines toward 50, reflecting buyers’ hesitancy. Additionally, EUR/USD started to edge lower after coming within a touching distance of the 50-perios Simple Moving Average (SMA).

On the downside, 1.1500 (Fibonacci 78.6% retracement of the latest uptrend) aligns as the first support level before 1.1450 (static level) and 1.1425 (lower limit of the descending regression channel).

Looking north, resistance levels could be spotted at 1.1550 (50-period SMA), 1.1580 (Fibonacci 61.8% retracement) and 1.1600-1.1610 (100-period SMA, upper limit of the descending channel).

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Natural gas prices began forming new bullish waves, to settle near $4.415 level, affected by the bullish momentum of the main indicators, to keep its stability within the bullish channel that appears in the above image.

We expect attacking 38.2%Fibonacci correction level at $4.750, to form the initial main target in the current trading, noting that surpassing this barrier will open the way for recording extra gains in the near period by its rally towards $4.910 and $5.150.

The expected trading range for today is between $4.300 and $4.750

Trend forecast: Bullish

Platinum price didn’t change anything due to its fluctuation between the levels of the current sideways track, that are represented by $1605.00, and $1525.00, which represents a key support for reducing the chances of suffering extra losses.

Note that stochastic attempt to provide positive momentum might push the price to form bullish trading, to attempt to renew the pressure on the previously mentioned barrier, to find an exit to record extra gains in the upcoming period, while breaking the support and holding below it will force it to suffer several losses that begin at $1485.00.

The expected trading range for today is between 985.00 and 1040.00

Trend forecast: Bullish

Copper price remains affected by the negative factors, which forces it to delay the positive attempts and provide some corrective trading by its stability near $4.9000, reminding you the continuation of providing negative momentum by stochastic might force it to retest the extra support at $4.7500, and breaking this support will force it to suffer extra losses that might extend towards $4.5400 and $4.3200.

While activating the bullish track requires forming strong bullish waves, to settle above $5.2000 level, then attempts to record extra gains by its rally towards $5.3200 and $5.5100.

The expected trading range for today is between $4.7500 and $5.0500

Trend forecast: Bearish

Platinum price didn’t change anything due to its fluctuation between the levels of the current sideways track, that are represented by $1605.00, and $1525.00, which represents a key support for reducing the chances of suffering extra losses.

Note that stochastic attempt to provide positive momentum might push the price to form bullish trading, to attempt to renew the pressure on the previously mentioned barrier, to find an exit to record extra gains in the upcoming period, while breaking the support and holding below it will force it to suffer several losses that begin at $1485.00.

The expected trading range for today is between 985.00 and 1040.00

Trend forecast: Bullish