Category: Gold News

Gold Price RECAP February 26

Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices and other key correlated assets—and may continue to into the future.

Gold prices are ripping towards a week-over-week gain beyond +2% on Friday, as markets reassess expectations for the timing of the first FOMC rate-cut of 2024.

So, What Kind of a Week Has it Been?

If there’s one trend that’s been a reliable mainstay for the gold market in the first two months of 2024, it’s a mostly stable trading range of $2020 to $2040/oz in the spot market. If there are two trends that have been a reliable mainstay for the gold market in the first two months of 2024, the second has been weeks that trade with relative calm and are then capped by a burst of volatility. Here, on the first trading day of March 2024, that second trend has kicked into gear so hard that may eliminate the first, going forward.

Because the macro-data calendar was basically empty for the first half of the week and there was little in the way of headline news that might shift the US Dollar, Treasuries, or commodities markets in a meaningful way, gold spot prices again traded flat through the first three days of this week, showing little interest in pushing much beyond $2035/oz but also marking reliable support above $2025. The first real point of interest for traders and investors looked to be Thursday’s PCE Price Index release, an update on the Federal Reserve’s preferred metric for inflation in the US. There was little expectation of a big surprise in the January number—the primary inputs to the PCE data set are the Consumer and Producer Price Indexes for the same period, which printed earlier in the month. The market broadly knew to expect a slight increase in both the “core PCE” basket of prices, and in the more volatile headline PCE number. To this point, February’s data did not surprise or disappoint, printing in-line with the consensus projection. What nobody was really looking out for, however, was the downward revision of December’s month-over-month inflation data, to just +0.1% for both headline and core PCE. In reaction that, admittedly, felt overblown, investors across multiple asset classes appeared to immediately recalibrate their assessment of the odds that the Federal Reserve might consider cutting interest rates before June. Going into this week, thanks largely to the statement and Q&A from January’s FOMC meeting, the market had mostly written-off this possibility, but the slide in the US Dollar and climbing Treasury paper prices that followed Thursday’s PCE report indicate that investors are all too happy to reconsider those odds. As we would expect in that case, gold prices jumped on Thursday morning as well, to $2046/oz and higher, immediately testing the top boundary of the recent range.

It was also a little surprising that, as Thursday’s trading went on, we didn’t see a big rush to take profit on the morning’s rally, being the final trading day of the month. It wasn’t the be, as gold traded flat through the afternoon, consolidating the new gains. Moving into Friday’s US session—the yellow metal had continued to hold its serve through the Asia sessions and the European morning trading—there was some checking-again to see if the first session March 2024 would see prices correct lower.

Instead, the argument for the Fed to begin cutting interest rates sooner than later gained another argument in its favor. After some other data and anecdotal reporting around the US’ industrial sector suggested a level of strength that would give the FOMC cover to continue restricting economic activity with higher rates, Friday’s ISM Manufacturing Index was a clear letdown, missing expectations for a modest increase in the key number and instead indicating more contraction than the previous months. Whereas the PCE data set on Thursday suggested the Fed could get comfortable with ending the brief era of “elevated” interest rates in its battle against inflation, the signal that things may be faltering in the engine room of the US economy implies that the Fed maybe should consider easing monetary policy sooner.

In the gold market, this drove a repeat of Thursday’s jump, and then some. The initial surge brought spot prices for the precious metal above $2060/oz with very little resistance to be seen, and the rally that followed the open of cash market trading in New York has delivered spot prices north of $2085/oz, as the US Dollar has softened farther at the end of the week and yields on the US Treasury’s 10-year Note have slipped below +4.10%.

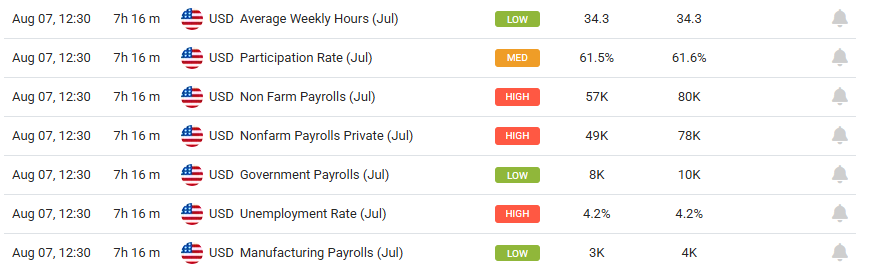

This sharp gain at the end of the week, and the start of the final month of Q3, has reset the table for gold prices and for expectations around FOMC policy decisions. Both will get a considerable test next week: first we’ll see (from the ISM again) if the “services sector” of the US economy is slowing like manufacturing, in a Tuesday morning report. And at the end of the week, we’ll see the February Jobs Report and a vital update on the health of the US labor market. In between the two, Fed Chair Jerome Powell will offer his semi-annual testimony to Congress, from which we expect to get a little more shading on the Fed’s forward planning.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here next week for another market recap.

Source link

Written by : Editorial team of BIPNs

Main team of content of bipns.com. Any type of content should be approved by us.

Share this article: