Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

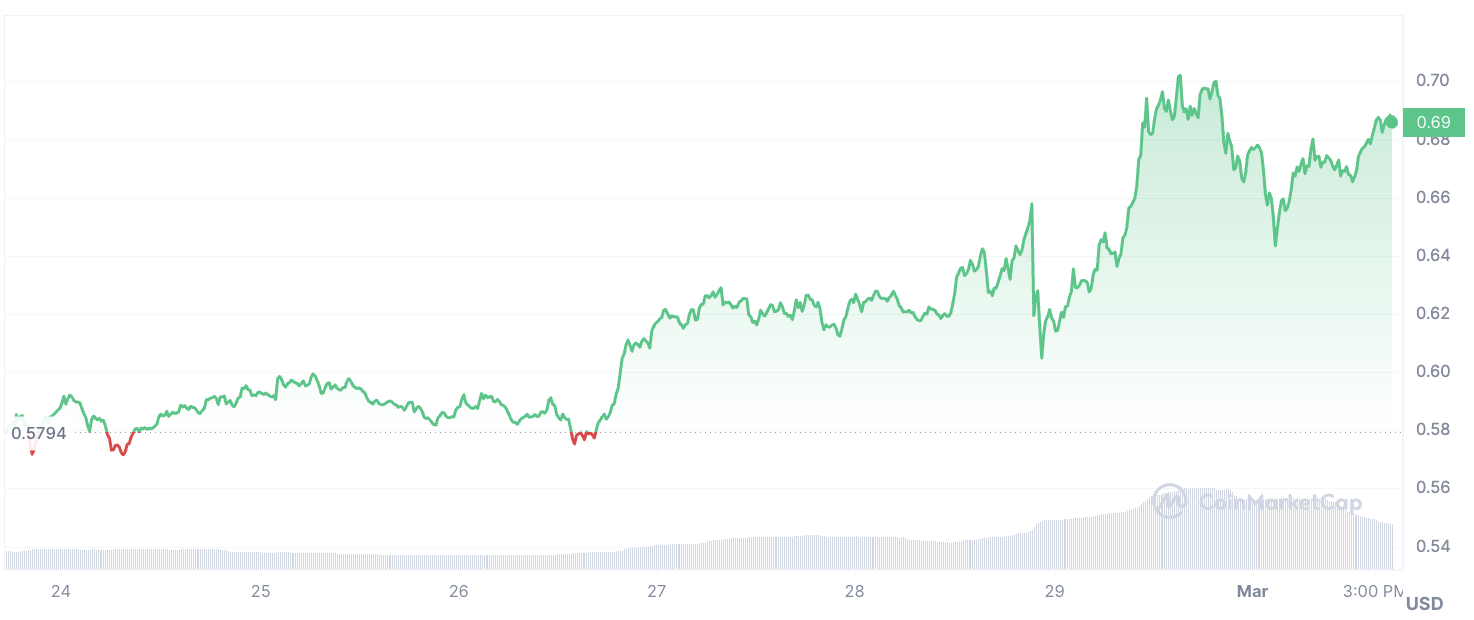

In a week marked by significant technological strides, Cardano’s native cryptocurrency, ADA, surged by an impressive 16.5%, reaching a peak of 20% in value. The price surge propelled ADA to $0.7, consolidating its position as the eighth-largest digital asset by market capitalization, which now stands at a formidable $24.45 billion.

The surge in ADA’s price was not an isolated event but rather a reflection of the substantial progress witnessed across the Cardano ecosystem. Major developments in core technology, smart contracts, scaling solutions and governance initiatives have set the stage for ADA’s remarkable ascent.

In terms of core technology, the ledger team made significant strides by introducing reference script support for Plutus V1 in Conway. This development, coupled with bug fixes addressing stake distribution inaccuracies, lays a robust foundation for the blockchain’s functionality.

Meanwhile, the Plutus team advanced smart contract implementation by initiating the Plutus contract blueprint for Plutus Tx and updating the quick start guide to streamline developer onboarding.

Scaling solutions received a boost as the Hydra team resolved critical bugs, optimized fee estimation mechanisms and implemented transaction metadata enhancements. Similarly, the Mithril team introduced a new distribution with critical updates, including improved stake distribution support and bug fixes.

On the governance front, the SanchoNet team launched a patch release to address compatibility issues and facilitate wallet upgrades. Additionally, Project Catalyst continued its momentum by onboarding 300 approved projects, emphasizing community-led accountability and transparency.

As ADA continues to attract attention and investment, the Cardano ecosystem appears poised for further growth and advancement on the burgeoning cryptocurrency landscape.

Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

Founder of SkyBridge Capital Anthony Scaramucci has taken to the popular X social media platform (known as Twitter in the past) to share his excitement about the pace at which BlackRock’s spot Bitcoin ETF (iShares Bitcoin Trust [IBIT]) continues to acquire Bitcoin.

This week, BlackRock’s Bitcoin-based exchange-traded fund crossed over the $10 billion line within the last seven days. Scaramucci reminded his followers that earlier this week, the crucial milestones of $7 billion, $8 billion and $9 billion were reached.

$iBIT crosses over $10 billion in AUM (after crossing $7 billion, $8 billion and $9 billion on consecutive days…….all this week!)

Scaramucci seems to be following particularly the progress of BlackRock’s milestones as if it means something for him personally. Two weeks ago, the financier also drew his followers’ attention to the fact that iBIT had surpassed the $5 billion mark of the acquired Bitcoin by then. Scaramucci is known to be a vocal cryptocurrency supporter, not only of Bitcoin but also Ethereum and several other major altcoins. The aforementioned fund founded by Scaramucci allows customers to invest in Bitcoin, Ethereum and other digital currencies.

Bitcoin ETFs keep scooping up BTC

According to the @lookonchain blockchain sleuth, on Feb. 29, eight spot Bitcoin funds purchased nearly $1 billion worth of the leading global cryptocurrency – 14,934 BTC valued at $940 million.

From this impressive amount, BlackRock sucked in 10,140 BTC worth $638 million. The second largest acquisition of Bitcoin on Thursday was made by the Fidelity Bitcoin ETF as it saw an inflow of 4,066 BTC (the equivalent of $255.9 million). Grayscale ETF sold 2,223 BTC on that day ($139.8 million).

On Feb. 28, slightly less BTC was acquired by the ETFs in total – 12,187 $BTC ($745 million). BlackRock’s share here constituted 9,114 BTC. As of now, BlackRock’s iBIT holds 151,536 BTC.

Bitcoin’s staggering price action

The continuous acquisition of Bitcoin by the aforementioned funds is believed to have led to the recent Bitcoin price surge as BTC gained a whopping 23.52% earlier this week, growing between Monday and Thursday to reach the $63,000 price level.

This explosive increase has now been broken, however, and within the last 24 hours, Bitcoin has shed some of its recent gains – 3.31% earlier today, falling back to the $60,000 zone. By now, though, Bitcoin has been restored to the $62,000 mark, having added 1.84%.

Five days ago, the total value locked (TVL) in decentralized finance (defi) protocols exceeded the $80 billion mark, and since that point, it has expanded by an additional $11.66 billion. As it hovers above the $91 billion threshold, the TVL is approaching the $100 billion milestone, a figure not observed since before the collapse of […]

Recent economic data has led to a decrease in U.S. Treasury yields, influencing Federal Reserve monetary policy speculations. The retreat of benchmark U.S. 10-year Treasury yields and the dollar index has bolstered gold’s appeal. Critical data points include the University of Michigan’s sentiment index and the personal consumption expenditures (PCE) index. Despite the PCE aligning with expectations, its annual figures still exceed the Fed’s 2% target, indicating persistent inflation.

Federal Reserve officials have expressed caution regarding premature rate cuts, emphasizing a data-driven approach. However, several have hinted at potential rate reductions later in the year. The U.S. Dollar Index’s 0.7% decline last week further supports this trend.

Economic Reports and Forecast

U.S. manufacturing downturn and weak consumer surveys underline the potential for a Fed rate cut. Gold’s prospects look positive, with expectations of easing monetary policy by mid-year. If economic data continues to underperform, gold prices could reach record highs in the next three to four months.

Central Bank Activity and Fed’s Stance

Strong central bank purchases of gold are a notable market support. Despite the Federal Reserve’s balance sheet decisions, their focus remains on controlling inflation and meeting their dual mandate. Fed Governor Chris Waller’s recent comments separate balance sheet policies from interest rate decisions, indicating a cautious approach to asset holding reductions.

The recent developments with New York Community Bancorp (NYCB), including the discovery of material weaknesses in loan review processes and increased commercial real estate exposure concerns, have significantly impacted its stock. This situation has triggered a defensive stance in the options market. NYCB’s shares plunged 24%, with a substantial increase in options trading volume. The bearish sentiment, however, seems confined to NYCB, with more balanced activity observed in broader regional banking ETFs.

Short-Term Market Forecast

Given the current economic backdrop, the outlook for gold remains bullish in the short term. The combination of dovish Federal Reserve signals, weakening economic indicators, and strong central bank buying presents a favorable environment for gold prices. The situation with NYCB further injects uncertainty into the market, potentially diverting more investment towards safe-haven assets like gold. The upcoming U.S. employment report and Fed’s future decisions will be critical in shaping the near-term trend of gold prices.

Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

The dog-themed cryptocurrency Shiba Inu (SHIB) has presented a compelling use case for its upcoming token, TREAT. Lucie, a Shiba Inu team member, shared this on X (formerly Twitter).

SHIB’s Solution Powered by Zama

“Initially, Shib’s solution powered by Zama will run on $TREAT, one of the Shiba ecosystem’s tokens developed to serve multiple purposes, including providing liquidity to the $SHI stablecoin, eventually replacing the $BONE token as the reward… pic.twitter.com/FexZhIsXWY

Shib recently announced a strategic collaboration with Zama, an open-source cryptography business that creates innovative Fully Homomorphic Encryption (FHE) solutions for blockchain and artificial intelligence.

This partnership marks a pivotal point in the evolution of Web3, setting new benchmarks in data privacy and security. As the Shib ecosystem grows and expands, incorporating Zama’s solutions presents a ground-breaking opportunity. As a result, the forthcoming TREAT’s use case comes into view.

Shib’s Zama-powered solution will first run on TREAT, a Shiba ecosystem token designed to fulfill numerous functions.

The upcoming TREAT is also intended to provide liquidity to the upcoming SHI stablecoin. Treat, a reward token, will eventually replace the BONE token as the reward token for ShibaSwap.

TREAT will also provide rewards for SHIB: The Metaverse and the blockchain version of the Shiba Inu-themed collectible card game Shiba Eternity.

In preparation for this new Web3 era ushered in by the SHIB Zama partnership, which will initially be powered by the upcoming TREAT token, an official X account for TREAT has been launched, which has garnered 5,271 followers as of press time.

As the excitement ramps up, the Shiba Inu community should bear in mind that TREAT has yet to be launched, the same as with the SHI stablecoin. Social media accounts or projects claiming otherwise might be scams intending to dupe users.

These are in no way associated with the Shiba Inu ecosystem. The official X Treat token handle is verified and has a Shiba Inu emblem right beside its blue tick. Thus, Shiba Inu holders are urged to be wary of fake TREAT tokens, avoid clicking suspicious links and follow official social media accounts for information.

Get your daily, bite-sized digest of blockchain and crypto news today – investigating the stories flying under the radar of today’s news.

In crypto news today:

Why is crypto down today?

Americans Lost $1.56B in Cryptocurrency to Fraud in 2023

Marathon Eyes $1.5B Offering

Advanced Phishing Kit Targeting Crypto Exchanges and US Federal Agency

__________

Why is crypto down today?

After several days of green fields, the crypto market is back in red – though just a bit.

The total crypto capitalization is down 1.7% over the past 24 hours.

It now sits at $2.41 trillion, according to CoinGecko.

As is to be expected, most of the top 100 coins by market capitalization are down.Looking at the top ten coins, we find that the price of only one of them has appreciated in the past day.

Solana (SOL) is up 8.5% to $133. This makes it the day’s best performer.

Yesterday’s winner,Dogecoin (DOGE), has seen the biggest loss today: 6.5% to $0.124.

Meanwhile,Bitcoin (BTC) is down 1.9%, still holding above the $60,000 level, at $61,649.

Notably, all coins in the top ten category are still green over the 7-day period.

Dogecoin leads the list with a 44% increase, Bitcoin is at 20%, and Ethereum at 14.5%.

Today’s slight market drop is not unusual. Actually, most analysts expect the bull to continue running.

Moreover, BTC’s latest rise is aligned with the introduction of spot Bitcoin exchange-traded funds (ETFs) by major financial institutions, including Bank of America’s Merrill Lynch and Wells Fargo.

This shows BTC’s acceptance and potential for significant growth.

Furthermore, analysts predict that Bitcoin could reach between $100,000 and $200,000, driven by institutional adoption and the halving anticipation.

However, Michael Novogratz, the CEO of digital asset services firmGalaxy Digital, warned investors that there may be a dip coming in Bitcoin’s value amidst its current rally.

“I wouldn’t be surprised to see some corrections and some consolidation,” said Novogratz. “If it corrects, it might correct to the mid-$50,000s, before taking off to the new high.”

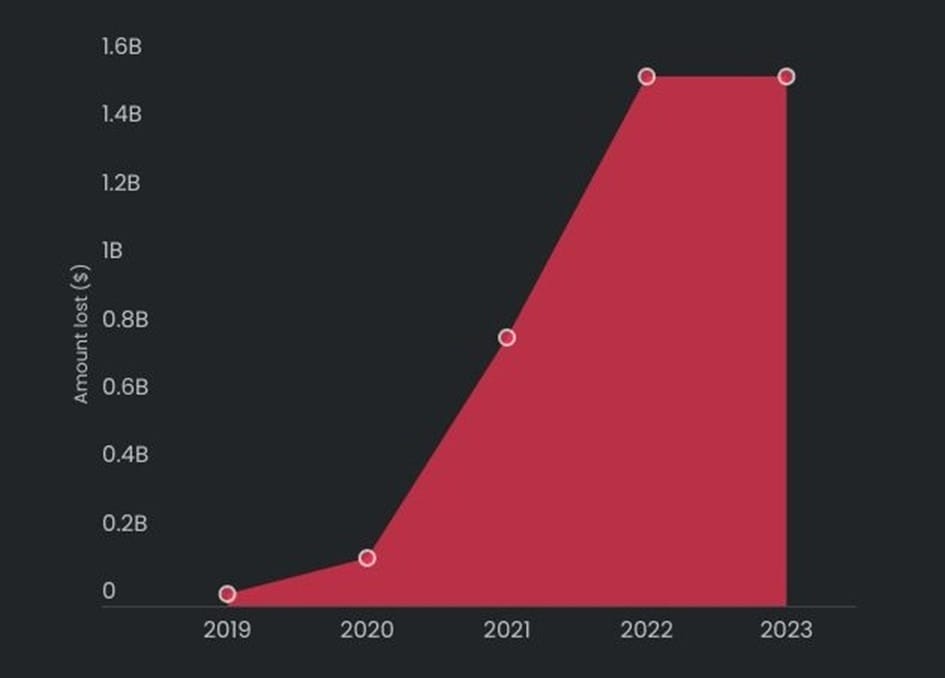

Americans Lost $1.56B in Cryptocurrency to Fraud in 2023

In top crypto news today, 15% of all fraud-related losses in the US in 2023 were in crypto, affecting 55,000 people, according to a recent report by the cybersecurity companySurfshark.

Surfshark collected data from the ‘Consumer Sentinel Network Data Book ‘by the Federal Trade Commission (2019-2023). Importantly, this data includes cases in which crypto was the payment method, but the scams themselves were not necessarily crypto-related.

That said, what the company found is that crypto fraud accounted for over $1.555 billion in losses in this country over 2023.

The report argued that,

“This positions cryptocurrency as the second-highest payment type in terms of monetary losses following bank transfers.”

Cybercriminals have been increasingly targeting crypto, said the report, but “losses have been especially dire since 2022.”

In 2022, the losses totaled $1.558 billion, marking a twofold increase from 2021.

Therefore, 2023 was the second consecutive year of crypto losses exceeding $1 billion.

Furthermore, the loss per victim has increased over these two years. While this number stood at $18,000 in 2021, it reached $26,000 in 2022, followed by $28,000 in 2023.

Source: Surfshark

Additionally, over half of all fraud losses in crypto in 2023 came from miscellaneous investments and investment advice fraud. There was $829 million in total losses, or $34,000 per victim.

Romance scams and business imposter scams follow with losses of $179 million and $140 million, respectively.

“The overall increase in losses has plateaued in 2023, showing minimal deviation from the figures in 2022,” the report stated. “Even if this trend of stalled growth continues into 2024, the scope of losses in cryptocurrency positions it as a significant threat for the year, warranting caution for all current and future crypto holders.”

According to Lina Survila, a spokeswoman at Surfshark, “to minimize the number of cryptocurrency victims, education and supported cryptocurrency adoption, coupled with investment in infrastructure improvements, are crucial.”

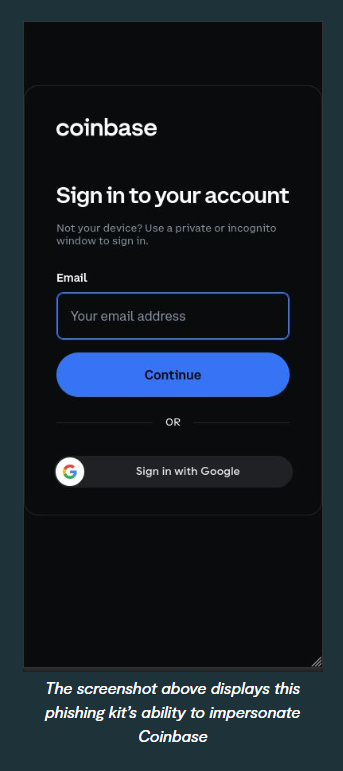

Advanced Phishing Kit Targeting Crypto Exchanges and US Federal Agency

Data-centric cloud security company Lookout, Inc. announced the discovery of an advanced phishing kit, calledCryptoChameleon, which targets crypto platforms and the Federal Communications Commission (FCC) via mobile devices.

According to the press release, the intended targets are mostly crypto users and single sign-on (SSO) services in the United States. However, these includeBinance andCoinbase employees.

Source: lookout.com

According to David Richardson, Vice President of Endpoint and Threat Intelligence at Lookout,

“We’re seeing a trend of financially motivated threat actors – who typically target cryptocurrency and direct financial fraud – move into breaching enterprise and government organizations for ransom. We urge cryptocurrency and single-sign-on users and organizations to take steps to protect their devices, work and personal data.”

The phishing kit first asks the victim to complete a captcha using hCaptcha. This prevents automated analysis tools from identifying the phishing site.

Notably, these scammers take their time. Unlike typical phishing kits that seek to harvest credentials as quickly as possible, CryptoChameleon is aware of modern security controls, such as multi-factor authentication, and allows bad actors to respond accordingly, said the report.

Also, bad actors utilize text messages and voice calls, personally reaching out to the victim to build a sense of trust and encourage them to follow the steps of the attack. Per the report,

“This has resulted in a high success rate, leading to the collection of quality data, including usernames, passwords, password reset URLs and even photo IDs.”

Moreover, CryptoChameleon uses phone numbers and websites that appear legitimate and reflect a real company’s support team. Lookout said that it has noticed an increase in the frequency of this style of attack – it has become more prevalent and is evolving.

The company warned that,

“With more corporate data residing in the cloud and a change in how users interact with that data, an increasing number of bad actors are now leveraging social engineering, targeting a user’s mobile phone to steal credentials that provide legitimate and immediate access to critical corporate data as part of the modern cyber kill chain.”

More than 250 phishing sites are using this kit, and their number is increasing.

Marathon Eyes $1.5B Offering

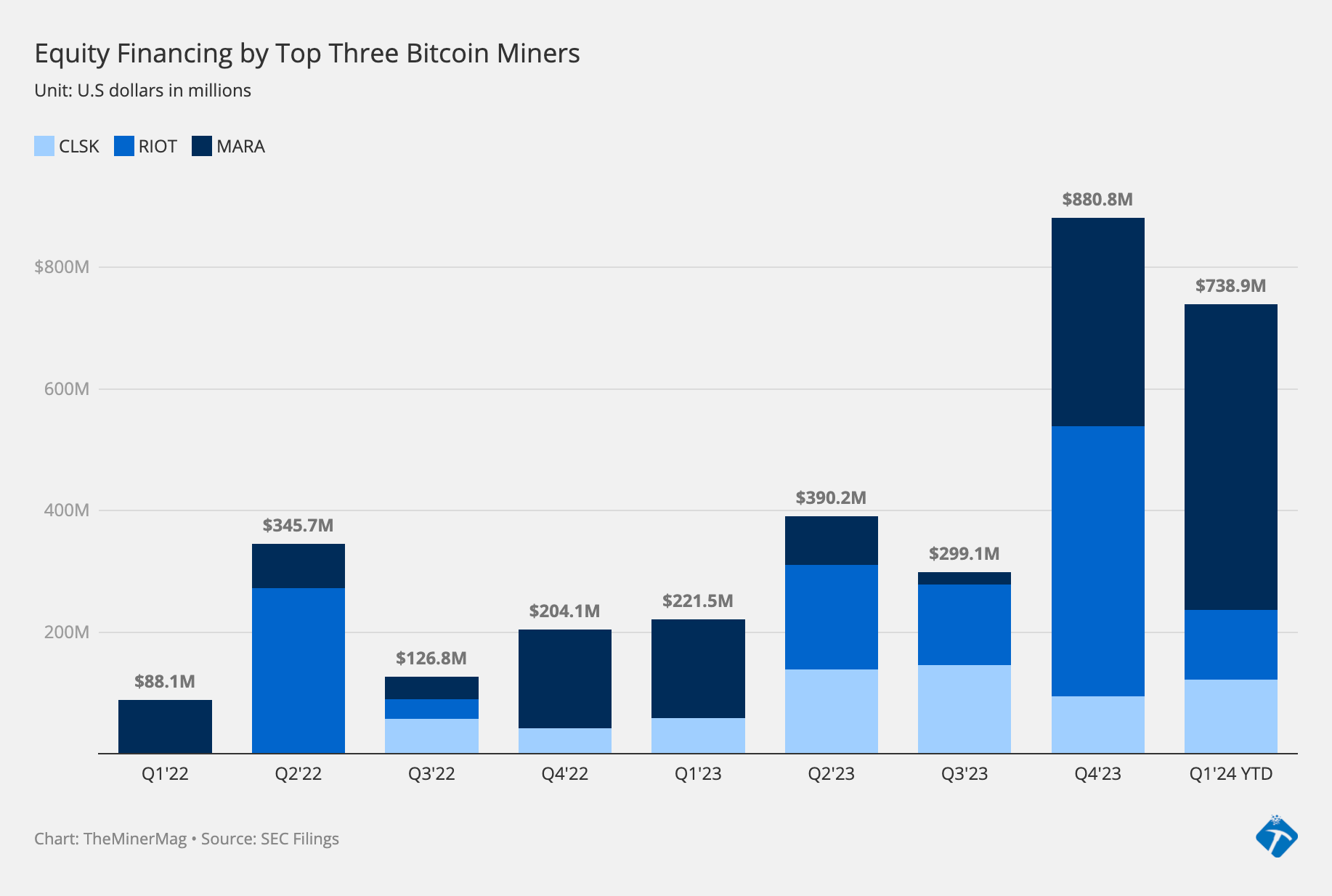

In other crypto news today, stock offerings by publicly traded mining companies are rallying, according to the latest Miner Weekly report byBlocksBridge Consulting.

Bitcoin mining firmRiot Platforms received $115 million in the first quarter so far. Meanwhile, it raised more than $500 million in equity in the last quarter of last year.

Furthermore, Bitcoin minerMarathon Digital reported that as of December 31, it had raised $248.1 million from its 2023 at-the-market (ATM) offering program since October. It had a cap of $750 million.

Then, since New Year’s Day, Marathon sold additional shares under the 2023 ATM to reach the maximum limit.

“[This implies] that it managed to raise an additional $500 million year-to-date.”

Moreover, the company said it planned to start a new ATM offering program with a maximum offering of $1.5 billion.

All in all, the top three bitcoin mining stocks per market capitalization – Marathon, Riot, andCleanSpark – raised $880 million in Q4 2023 and $739 million in the first two months of 2024.

Other companies, includingHIVE andIris Energy, also continued to raise additional funds since the New Year.

Source: blocksbridge.substack.com

A majority of the raised funds will be used to pay for miner commitments and infrastructure buildout during 2024 and 2025.

Meanwhile, CleanSpark continued its preorders ofBitmain’s Antminer S21s in early January.

Riot, on the other hand, seems to be switching toMicroBT’s products as some of its existing Antminers have been causing issues.

And while Marathon hasn’t made any major miner purchases from Bitmain or MicroBT, it paid $15 million in September to its portfolio company Auradine to secure certain rights to future purchases of its Bitcoin ASIC miners.

Mon: Swiss CPI (Feb), South Korean GDP (Q4), Japanese Tokyo CPI (Feb),

Tue: US Primary Super Tuesday, Chinese Caixin Services PMI Final (Feb), EZ/UK/US Services and Composite PMI Final (Feb), EZ PPI (Jan), US ISM Services PMI (Feb), South Korean CPI (Feb)

Wed: BoC Announcement, Australian GDP (Q4), German Trade Balance (Jan)

Thu: ECB Announcement, Japanese Wage Data, Chinese Trade Balance (Feb)

Fri: German Industrial Output and PPI (Jan), EZ GDP Revised (Q4), US Jobs Report (Feb), Canadian Jobs Report (Feb)

Sat: Chinese Inflation (Feb)

Sun: Japanese GDP (R)

Note: Previews are listed in day order

China two-sessions (Mon/Tue):

China’s political elite and lawmakers are poised to gather for the nation’s annual legislative sessions. The event, dubbed the “two-sessions”, will set budgets and lay down Beijing’s plans for the country’s economy, trade, diplomacy and military. Some also flag a potential re-evaluation of economic strategies with a clear focus on stimulating internal demand. From a market perspective, confidence in an investable China needs to be restored. FT reported that regulators are taking measures to keep the exchange rate stable in a bid to boost confidence in the Chinese currency and economy ahead of the meeting. Sentiment in Chinese stocks has also been bearish. Chinese authorities have recently stepped in with regulators telling quant funds to end a popular high-leveraged strategy – “The gradual exit would help prevent drastic selloffs, sources said. China’s Global Times, citing analysts, suggests this year’s event will likely focus on “discussing how to proceed with the high-quality development of the economy and how to further boost confidence in the Chinese economy.” Analysts at ING expect the Two Sessions to maintain the GDP target. ING forecasts: GDP around 5% (vs “around 5%” in 2023), Inflation around 3% (vs “around 3%” in 2023), New Urban Employment around 12mln (vs “around 12mln” in 2023), Urban Unemployment Rate around 5.5% (vs “around 5.5%” in 2023), Fiscal Deficit around 3.5% (vs “3%” in 2023), and Special Government Bond Issuance 4tln (vs “3.8tln” in 2023).

Swiss CPI (Mon):

February’s CPI data will draw slightly more scrutiny than normal as it will include the latest estimate of rental price pressures; on January 23rd, Jordan said he expects some inflationary pressure from rents, though he did also expect an acceleration in prices during January. However, the January print came in markedly cooler than forecast at 1.3% vs expected and previous of 1.7% (SNB Q1 forecast 1.8%) and sparked a significant dovish shift in market pricing to over a 50% chance of a March cut vs circa. 25% pre-release (currently 60%). February’s data will be scrutinised for any indication that January’s print was not indicative of the pricing backdrop (possible, given January is often a more volatile reporting period) and as mentioned for signs of any rental pressures. The last rental update was provided in November and saw the index increase by 1.1% Q/Q or 2.2% Y/Y, a level judged as acceptable and sparked a dovish shift in pricing heading into the December gathering.

Tokyo CPI (Mon):

Tokyo inflation data for February is due early next week which is seen as a leading indicator for the national price trend, while participants will be eyeing the data to see if there is a further slowdown after Core CPI in Japan’s capital slowed for a third consecutive month in January to its lowest in almost two years. As a reminder, Tokyo Inflation in January printed softer than expected with headline CPI at 1.6% vs. Exp. 2.0% (Prev. 2.4%) and CPI Ex. Fresh Food at 1.6% vs. Exp. 1.9% (Prev. 2.1%) which were their lowest readings since March 2022, while CPI Ex. Fresh Food & Energy printed its slowest pace of increase in 11 months at 3.1% vs. Exp. 3.4% (Prev. 3.5%). The softening in the Tokyo inflation data was helped by a decline in energy and utility costs, while the rise in the prices of accommodation had eased and there was also a moderation in the pace of increase of processed food prices which softened the blow from the largest upward driver of inflation. Furthermore, the national inflation data for Japan in January also showed a decline for the third consecutive month to reach its lowest in 22 months but was firmer than expected and matched the central bank’s price target with National Core CPI at 2.0% vs. Exp. 1.8% (Prev. 2.3%).

US Primary Super Tuesday (Tue):

Super Tuesday is the busiest day in the pre-convention election calendar. For the Democrats, the stakes are minimal given incumbent President Biden is essentially guaranteed to secure the nomination. For Republican’s the narrative isn’t quite as clear, as former President Trump still faces opposition from Nikki Haley. However, Trump has taken a commanding lead in the race and Super Tuesday’s primaries are unlikely to alter this narrative. Therefore, barring any significant Haley surprise, market reaction may well be minimal and in-fitting with primaries thus far. Post-Tuesday, attention turns to when Haley exits the race (she has committed to at least Super Tuesday) or failing that when Trump hits the 1215 delegate threshold needed to secure the nomination. Recently, Trump’s team estimated this could occur as soon as 12th March when four primaries are held. Thus far, Trump has won 119 delegates vs Haley’s 22.

US ISM Services PMI (Tue):

The headline is currently expected to pare a little to 53.3 in February vs the 53.4 in January. In its flash PMI data for the month, S&P Global noted that flash US services business activity fell to a fresh three-month low at 51.3 (from 52.5). The survey compiler said “services sector growth has slipped slightly, however, as has confidence in the year-ahead outlook among service providers, in part reflecting some pull back in the extent to which interest rates are expected to fall in 2024.” Still, S&P welcomes news that both manufacturing and services are back in expansion territory again for the first time in three months. It added that the expansion was being accompanied by subdued price pressures. “Although up slightly in February, the survey’s gauge of selling prices for goods and services continues to run at a level consistent with the Fed hitting its 2% inflation target, and a further fall in cost growth to the lowest since October 2020 hints at price pressures remaining subdued in the coming months.”

UK Budget (Wed):

Next week focus in the UK will mostly be on the fiscal, rather than the monetary side of policy as UK Chancellor Hunt presents his spring budget. From a political perspective, the Chancellor is under immense pressure from his party to lower taxes in an attempt to turn the Conservative party’s fortunes around ahead of this year’s general election. In terms of what the Chancellor can actually “pull out of the hat”, economists at Pantheon Macroeconomics anticipate a GBP 20bln tax package with the headroom afforded to the Chancellor based on the following two fiscal rules; 1) “government debt-to-GDP ratio must be forecast to be falling in five years’ time” and 2) “public-sector borrowing has to be below 3% of GDP in the same year”. Hunt has been afforded more “headroom” for spending on account of lower levels of borrowing since the Autumn Statement with PM expecting the OBR to lower its 2023/24 borrowing forecast to GBP 114bln from GBP 123.9bln. In terms of how the tax cuts will be implemented, PM anticipate a combination of a freeze in fuel duty, income tax reductions and some measures to support the housing market. Goldman Sachs suggest that the basic rate of income tax could be lowered by 2p, however, murmurings out of the Treasury have labelled an equivalent move for national insurance as “impossible at the moment”. As such, the Chancellor may be forced to raise taxes elsewhere via measures such as hiking taxes on vapes and tobacco. Whilst the politics of the situation will see prompt Hunt to do as much as he can to lower the burden on UK taxpayers, the events of September 2022 via the Truss mini-budget remain at the forefront of investor sentiment and therefore anything the resembles a lack of fiscal prudence could prompt outsized moves the UK rates space, which could then have some spill over to monetary policy. That being said, under the assumption that measures in the budget comply with fiscal rules, ING is of the view that sizeable tax cuts “would add further impetus for the Bank of England to keep rates on hold a little longer”. Finally, with regards to the Gilt borrowing remit, Morgan Stanley expects the 2024/25 Gross issuance figure to decline to GBP 252.7bln from GBP 257bln.

BoC Announcement (Wed):

The consensus expects the BoC to hold its policy interest rate at 5.00%, with analysts projecting the first rate cut will come at the central bank’s June confab, according to a poll by Reuters. The survey notes that while inflation has fallen back within the BoC’s 1-3% target rate (at 2.9% Y/Y last), policymakers are not yet convinced that high inflation has been resolved yet, particularly as shelter costs remain elevated. BMO said “the risk is the first rate cut will come later than June. If the bank is going to make an error here, it is that they’ll keep policy too tight for too long to make sure inflation is headed back towards their target or event lower,” adding that “they’re also concerned about a renewed pickup in the housing market, and just more recently, they’ve got the added wrinkle the Canadian dollar has started to weaken again. The Reuters poll added that there was no clear consensus around the number of rate cuts coming this year, but around 70% of the economists surveyed are looking for 100bps of cuts or less.

Australian GDP (Wed):

Australian GDP data for Q4 is scheduled next Wednesday which will provide a gauge into the health of the economy after the somewhat mixed readings in Q3. The previous economic growth data for Australia showed the economic growth missed expectations and slowed to 0.2% vs. Exp. 0.4% (Prev. 0.4%) to match its weakest quarterly growth in two years although GDP Y/Y topped forecasts and maintained the pace of expansion of 2.1% vs. Exp. 1.8% (Prev. 2.1%). The soft quarterly growth was helped by domestic final demand which contributed 0.5 percentage points to GDP growth and government expenditure rose 1.1% and accounted for a 0.2 percentage point increase to GDP with state and federal government social benefit schemes such as the Energy Bill Relief Fund and expansion of the Child Care Subsidy the main contributors, while capital and private investment also continued to increase. Conversely, goods industries weakened with the mining and agriculture industries declining by 1% and 3.5%, respectively, while utility services fell 2.6% amid less demand for heating during the quarter. Furthermore, GDP per capita had declined for a 3rd straight quarter and if it weren’t for population growth or government spending, the economy would have been in a contraction. Looking ahead, the expectations are for Australia’s GDP in Q4 to maintain its Q/Q expansion of 0.2% and for Y/Y growth to slow to 1.5% from 2.1%. Furthermore, the other metrics for economic activity in Q4 have been mixed as Retail Trade and Capital Expenditure topped forecasts but CPI and Construction Work Done were softer than expected, while monthly Manufacturing and Services PMI data were in contraction territory from October to December.

ECB Announcement (Thu):

Expectations are for the ECB to once again stand pat on rates with markets assigning a 94% chance of such an outcome. The previous meeting passed with little in the way of fanfare with the Governing Council very much in wait-and-see mode as policymakers track progress in inflation returning towards the 2% mandate. In terms of developments since the prior meeting, headline HICP pulled back to 2.6% in February from 2.8%, whilst the core metric fell to 3.3% from 3.6%. From a growth perspective, Q4 GDP printed at 0% vs. the 0.1% contraction seen in the prior month, whilst more timely PMI data saw the EZ-wide services PMI rise to 50.0 from 48.4, manufacturing slip to 46.1 from 46.6, leaving the composite at 48.9 vs. prev. 47.9. The accompanying report noted “The latest PMI print gives hope for a recovery in the eurozone”. Recent comments from ECB officials continue to point towards no imminent intention to lower rates with President Lagarde observing that the ECB is “not there yet” when it comes to inflation, whilst most officials wish to see the outcome of the April wage data (released after the April meeting). In terms of a timeline for the first cut, known-dove Stournaras of Greece does not anticipate one until June with markets broadly in-fitting with this viewpoint, assigning a 92% chance of such an outcome. In the analyst community, 46/73 surveyed by Reuters expect a reduction in June, 17 look for April and 10 expect a H2 reduction. With regards to the full year outlook, markets anticipate a total of 86bps of policy loosening, the median view of analysts looks for 100bps. For the accompanying macro projections, analysts at Danske Bank expect (for the first time in the hiking cycle) “staff projections to show that inflation will hit the 2% target in both 2025 and 2026”, with the 2024 HICP projection to be cut to 2.4% from 2.7% on account of “recent lower than expected inflation data, anchored inflation expectations, and lower energy futures”.

Japanese Wage Data (Thu):

There are currently no expectations for the data, but the release could attract some attention given the BoJ’s focus on wages coupled with recent hotter-than-expected CPI. Household spending figures will also be released the next day. However, the BoJ is keeping a closer eye on the upcoming Spring wage negotiations. Governor Ueda, at the BoJ’s January conference, suggested the number of firms that have decided to hike wages at this year’s Spring wage talks is higher than this time last year, and highlighted that even if real wages are negative and the outlook is positive, a policy change is possible. Former BoJ policymaker Sakurai on Feb 22nd said the BoJ could end negative rates in March if this year’s pay hikes exceed 4%, although there’s an equal chance it may wait until April. He added the BoJ appears to be fully prepared for an exit, it’s a question of when Governor Ueda makes a call.

Chinese Trade Balance (Thu):

There are currently no forecasts for the trade balance data but as usual the metrics will be used as a gauge of domestic and foreign demand. In terms of the release, the January data did not come out last month amid the Chinese New Year holiday. In terms of the release seen in Jan, Chinese exports grew at a faster pace in December 2.3% (exp. 1.7%, prev. 0.5%). However, imports missed forecasts at +0.2% (exp. +0.3%, prev. -0.6%), indicating fragile demand. It’s worth noting that the data will be released after the China Two-Sessions in which some flag a potential re-evaluation of economic strategies with a clear focus on stimulating internal demand.

US Jobs Report (Fri):

The US economy is expected to have added 188k nonfarm payrolls in February, with the pace of payroll additions cooling from the 353k reported in January. Analysts said that the Feb data is likely to be supported by the unseasonably milder weather conditions in the month. The unemployment rate is forecast to remain unchanged at 3.7% (the Fed’s December projections see unemployment ending this year at 4.1%, then remaining there over the course of its forecast range). Capital Economics is sceptical that the acceleration in employment growth in December and January marks a genuine resurgence in labour demand, noting that S&P Global’s PMI data, regional Fed surveys, and the NFIB survey’s hiring intentions indicator, and the downward trend in job openings allude to cooling conditions in the months ahead. Meanwhile, average hourly earnings are expected to rise by 0.2% M/M, cooling from the +0.6% rate seen in January. CapEco is beneath the consensus view on AHE, seeing gains of just +0.1% M/M, and sees the annual rate falling back to 4.3% Y/Y from 4.5% in January. It explains that January’s slump in hours worked was concentrated in low paid retail and leisure sectors, and argues that January’s jump in average earnings was a weather-related distortion, observing that during past three weather disruptions, average hourly earnings increased by an average of 0.44% in the weather-hit month and then only 0.13% in the following month.

Ethereum (ETH) Age Consumed vs. Price | Source: Santiment

Declining values of the Age Consumed typically means that investors are generally holding their coins longer. More so, if it occurs while an asset is trading at a 3-year peak as observed above, it signals an overwhelming bullish conviction among long-term investors that prices will rise even higher.

Evidently, the positive narratives surrounding the widely-anticipated Ethereum ETF approval, and the Dencun upgrade launch now slated for March 13, may have influenced the investors outlook.

Prediction: Can ETH price reach $4,000 in March 2024?

As things stand, Bitcoin investors redirecting capital towards altcoins, and existing investors are reluctant to sell. These two factors could combine to form a major catalyst for Ethereum price to move above $4,000 in March 2024.

This bullish Ethereum price prediction is further affirmed by IntoTheBlock’s Global In/Out of The Money metric, which groups all existing Ethereum investors according to their entry prices.

However, it shows that the bulls must scale the initial resistance at $3,600. As seen below, 235,680 existing holders had bought 593,350 ETH at the minimum price of $3,624, forming the largest cluster of potential profit-takers within 20% boundaries of the current prices.

But if the bulls capitalize on the two potential catalysts analyzed above, ETH price will likely smash through the $3,600 resistance in March 2024 and advance towards $4,000.

Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

As February fades in the rearview, the crypto market stands witness to unprecedented shifts. Bitcoin’s remarkable surge, with a 43.57% gain propelling it to $64,000, set the stage for a dynamic month. Not to be outdone, altcoins excluding BTC and ETH surged, collectively adding nearly $121 billion in capitalization.

But what about the future? XRP, Cardano (ADA) and Shiba Inu (SHIB) holders eagerly anticipate March’s unfolding.

XRP, having added 17.1% in February, stands poised for potential growth. While historical data reveals a median profitability of -1.65% for March, recent years hint at a favorable upswing.

Cardano, basking in a 32.2% surge last month, paints a similarly optimistic picture. With a historical pattern showcasing equal growth and decline, recent years have favored a bullish trend, setting a median profitability of 2.7% for March.

Meanwhile, the meteoric rise of Shiba Inu to 16th place in market capitalization, courtesy of a 42% surge, has investors buzzing. Yet, with its short history, forecasting remains uncertain. Although SHIB experienced a modest gain in 2022 and a slight dip in 2023, March’s median profitability of 0.43% provides scant guidance.

However, caution is warranted. Price history serves as a compass rather than a guarantee in the volatile crypto realm. While trends offer insights, they do not dictate future outcomes.

For XRP, ADA and SHIB holders, March holds promise, buoyed by recent gains and historical patterns. Yet, as the adage goes, past performance is not indicative of future results. As the new month dawns, investors tread cautiously, mindful of both potential and uncertainty in the ever-evolving crypto landscape.

Bitcoin (BTC) Age Consumed vs. Price | Source: Santiment

The chart above depicts that BTC Age Consumed recorded its upswing on Feb 29, right after prices hit $64,000. This move that unsurprisingly tipped the momentum in the bears’ favor momentarily as prices dipped

In specific terms, Bitcoin saw 78.4 million coin days consumed on Feb 29. And within 48 hours, BTC price took a tumble from 5% tumble from $64,000 to $60,644

Notably, this was the highest value of coin days destroyed, since the post-ETF sell-the-news wave around Jan 15, when BTC Age Consumed rose to 104.3 million.

This signals that after 51% gains in February, BTC long-term holders are now making strategic moves to book some profits and diversify their portfolio.

BTC Dominance Has Trended Downwards Since Feb 28

In further confirmation of this stance, market data trends shows that since the major sell-off recorded among BTC long-term holders on Feb 29, Bitcoin share of the crypto market has been in decline.

TradingViews’ Bitcoin Dominance chart (BTC.D), shows the value of Bitcoin’s market capitalization in comparison to the rest of the crypto market. Since hitting $64,000 on Feb 28, BTC.D has declined by 2% to hit a weekly low of 53.5% on March 2, as depicted in the chart below.

Price to Break ,000 After Bitcoin’s Latest Move?")

Price at Crossroads —0k Breakout or k Reversal?")