The main category of All News Articles.

You can use the search box below to find what you need.

[wd_asp id=1]

The main category of All News Articles.

You can use the search box below to find what you need.

[wd_asp id=1]

XRP is stabilizing after a sharp multi-week decline pushed the token into the $1.81–$1.90 support band, an area that has repeatedly triggered rebounds since early autumn. At $2.04 today, XRP is up 5.18% over the past 24 hours, supported by stronger buying interest and growing signs that sellers may be losing momentum.

The asset’s market cap now stands at $123.1 billion, keeping it firmly ranked #4 in the crypto market.

The latest 4-hour candle structure shows XRP breaking back above $2.00 with conviction. This recovery followed a deep rejection wick near the recent low — a classic signal that bears are exhausting and liquidity is shifting toward buyers.

XRP’s broader structure is still defined by a descending triangle, with each rally capped by a persistent downward trendline stretching back to September. Yet the tone is changing. The RSI has bounced sharply from oversold territory and is now forming the early stages of a bullish divergence, a pattern that often precedes meaningful trend reversals.

XRP/USD

Candlestick behavior supports this shift. A bullish engulfing pattern formed at the base, coming after several long-wick candles that showed absorption of sell pressure.

XRP has also reclaimed the 20-EMA on the 4-hour chart for the first time in nearly two weeks. The next major technical barrier is the 200-EMA near $2.30, which aligns with the descending trendline.

Key short-term observations include:

• Bullish engulfing confirmation near support

• RSI turning higher from oversold levels

• Price reclaiming the 20-EMA for the first time in weeks

If buyers can hold XRP/USD above $2.06, the recovery could extend toward $2.30 and later $2.50. A daily close above the descending trendline would mark the first genuine shift in structure and open the door to a broader breakout toward $2.70–$2.97.

A simple trade framework for newer traders is to wait for a confirmed close above $2.06, with a stop below $1.90. If momentum continues to build, XRP may revisit the $2.50 and $2.97 zones — levels that acted as major pivot points earlier in the cycle.

Despite recent volatility, the price action now reflects early signs of stabilization. If liquidity rotates back into altcoins, XRP could be among the first to regain upside traction.

Maham Arslan

Crypto News Writer | Blockchain & Web3 Reporter

Maham is a crypto news writer and market analyst specializing in breaking down the latest developments across blockchain, digital assets, and decentralized finance (DeFi). With hands-on experience covering high-impact stories—from regulatory shifts and token launches to macro-driven price movements—she delivers timely, accurate, and SEO-optimized content for fast-growing crypto media platforms.

Her expertise lies in producing daily news reports, price predictions, technical summaries, and coverage of market-moving events. Maham tracks real-time updates across global newswires, X (Twitter), and on-chain data to provide actionable insights tailored for retail traders, crypto enthusiasts, and institutional readers.

With a strong grasp of crypto fundamentals and Web3 trends, she delivers content that’s informed, accessible, and always on time.

For players navigating the fast-growing Ton Station ecosystem, the Daily Combo has become one of the most anticipated and profitable activities of the day. As the game continues to expand across Telegram and Web3 communities, more users are seeking reliable information about daily rewards, shortcuts to leveling up, and ways to turn in-game points into real $TONS tokens.

Today, November 21, 2025, we break down everything you need to know about the Ton Station Daily Combo, how it works, and why thousands of players check for the updated code each morning. Whether you’re a seasoned Web3 gamer or a newcomer trying to build momentum, this guide explains the essentials clearly and helps you claim your rewards faster than ever.

Ton Station is a Telegram-based interactive game where players earn points that can later be converted into $TONS, the game’s digital token operating within the TON blockchain ecosystem. Unlike traditional mobile games, Ton Station merges social gameplay with economic incentives, capturing the attention of millions of players across various Telegram communities.

For more bonuses, keep checking Binance Word of the Day Answer 20 November 2025, and check out more exciting tasks!

Among its many daily quests, the Daily Combo stands out as one of the most rewarding. The challenge is simple: players must guess the correct combination of four cards, and if they get it right, they immediately earn bonus points. These points contribute directly to in-game progression and future token claims.

What makes the Daily Combo particularly attractive is that players don’t always have to guess. Active communities often share the correct combination, allowing newcomers and casual players to earn rewards without risk or additional effort.

This combination of simplicity and high reward potential has quickly made the Daily Combo a core part of the game’s daily routine.

Promo Code: Coming Soon

The official promo code for today will be updated once released through Ton Station’s community channels and partner websites. According to Ton Station’s usual pattern, the combination is made available early in the day and resets at midnight. That means players only have a limited window to claim the reward.

HokaNews will update today’s combo code instantly once it becomes available.

For many Ton Station players, the Daily Combo is more than just a mini-game. It’s one of the fastest ways to:

The Daily Combo offers immediate points without completing lengthy missions or spending hours in the game. The mechanic encourages consistent logins, helping players maintain their progress and maximize their daily bonuses.

Fast points mean faster level progression—and that leads to earlier access to token claims. Because Ton Station enables users to convert earned points into $TONS, completing the Daily Combo becomes a direct path to increasing your crypto balance.

Each successful combo accelerates your growth and shortens the time needed to reach reward milestones.

The Daily Combo doesn’t work in isolation. Players often tackle multiple daily tasks from Ton Station and other Telegram-based Web3 games. By completing these activities together—such as missions from Metropolis World or Kokodi Game—you create a compounding effect on your points.

This strategy allows ambitious players to earn more in less time, creating a significant boost to their overall token earning potential.

The Ton Station Daily Combo changes every 24 hours. The correct combination is typically released through:

Ton Station’s official Telegram community

TON-related Web3 gaming channels

Partner news outlets

Gaming discussion groups

Web3 content creators

HokaNews’ daily update feed on hokanews.com

Because the combo resets at midnight, players are encouraged to redeem the code early to avoid missing out. Claims must be submitted before the countdown refreshes, or the opportunity for the day is lost.

Redeeming the daily reward is straightforward:

Open the Ton Station App or Telegram Game Page

Navigate to the official Ton Station interface where the Daily Combo section is located.

Enter the Four-Card Combination

Type the exact four-card sequence provided by reliable sources such as HokaNews.

Receive Your Instant Bonus Credits

Your points are added to your account immediately, requiring no additional steps.

Merge With Other Daily Tasks

Pair this reward with other missions to maximize your total daily earnings.

This simple process takes only seconds yet contributes significantly to your long-term in-game success.

Ton Station capitalized on a rising trend: turning Telegram into a global gaming hub. With the growth of tap-to-earn games and blockchain-powered micro-missions, the gaming landscape shifted dramatically. Ton Station distinguished itself through:

Players no longer needed powerful devices or traditional apps. A simple Telegram account was all they needed to participate in a global reward system.

This evolution transformed Ton Station into a daily ritual for many Web3 users, making the Daily Combo one of the most consistently searched features across gaming networks.

To fully leverage Ton Station’s ecosystem, consider the following strategies:

The earlier you redeem each Daily Combo, the less likely you are to miss the deadline. Players who develop a morning routine often outperform those who log in later in the day.

Being part of Telegram channels that consistently share the Daily Combo ensures you never miss the latest code. These communities also exchange tips, strategies, and shortcuts that help accelerate progress.

Many TON-based games offer daily missions. Merging these tasks lets you build a strong earning cycle that compounds throughout the week.

Ton Station will periodically update its token claim features. Monitoring your points helps you anticipate when you’ll be able to convert them into real $TONS.

HokaNews provides verified combo codes and guides daily. Bookmarking the site ensures you always have the latest information.

The Ton Station Daily Combo continues to be one of the most valuable tools for players looking to boost their progress, earn tokens quickly, and stay competitive within the Telegram gaming ecosystem. As the game evolves and new features are introduced, the importance of daily rewards remains central.

With today’s combo for November 21, 2025 expected soon, players should prepare to redeem it once it goes live. Staying updated through trusted platforms like hokanews.com ensures accuracy, speed, and maximum daily benefits.

Whether you’re aiming for higher levels, faster token rewards, or simply an optimized gaming experience, the Daily Combo remains a must-complete task.

hokanews.com – Not Just Crypto News. It’s Crypto Culture.

Writer

@Erlin

Erlin is an experienced crypto writer who loves to explore the intersection of blockchain technology and financial markets. She regularly provides insights into the latest trends and innovations in the digital currency space.

Check out other news and articles on Google News

Matcha is set to be the beverage of 2025, with its unique Japanese green tea flavour winning over Brits. However, its distinct taste might take some getting used to, which is why adding a syrup can make it even more scrumptious.

Just because we’re on the brink of autumn doesn’t mean you have to bid farewell to your favourite iced drinks. Autumnal flavours like carrot cake and apple butter are causing a buzz among matcha enthusiasts, with Blank Street launching these tasty matcha drinks just this week.

They’ve also reintroduced the viral banana bread matcha, but if you don’t fancy splashing out on one of these daily, it’s so easy to whip up your own at home.

READ MORE: I add one weird ingredient to my hot chocolate – it makes it taste heavenlyREAD MORE: NHS GP says when drinking too much tea and coffee can become ‘toxic’

TikTok user Olivia Adriance shared her banana bread matcha recipe last autumn, but now that it’s trending again, it’s the best time to try making it.

Thanks to the easy homemade banana syrup, it’s sweet and spiced, mixed perfectly with the fresh matcha flavour. It also works out to be cheaper than buying a matcha, which can sometimes set you back nearly £5, reports the Express.

Taking a sip, Olivia shared that it tasted ‘so good’, with the subtle hint of banana bread working ‘really well’ in the drink. Here’s how you can make it at home.

For more stories like this subscribe to our weekly newsletter, The Weekly Gulp, for a curated roundup of trending stories, poignant interviews, and viral lifestyle picks from The Mirror’s Audience U35 team delivered straight to your inbox.

Ingredients

Method

Help us improve our content by completing the survey below. We’d love to hear from you!

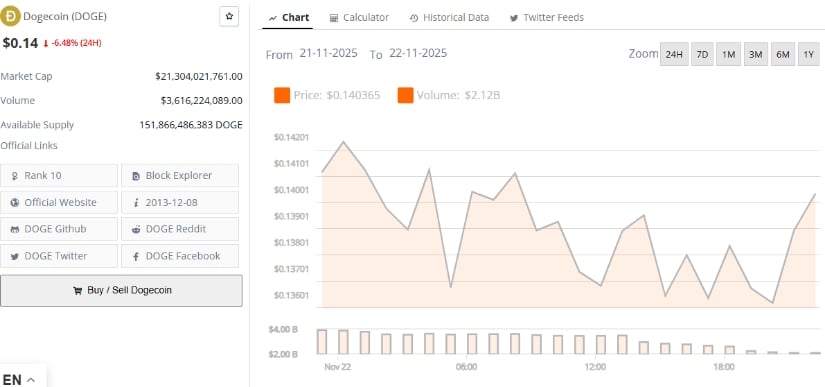

Dogecoin (DOGE) is navigating a critical consolidation phase as prices remain below $0.15, testing long-term support levels while investors assess whether a rebound toward $0.18 is feasible amid ongoing market volatility.

This analysis combines technical indicators, historical price structures, and expert commentary to provide a measured perspective on DOGE’s near- and medium-term outlook.

After falling beneath the $0.14–$0.15 range, Dogecoin has been trading near $0.138, representing a roughly 3% daily decline. According to CoinMarketCap data, DOGE’s 24-hour trading volume stands at $6.17 billion, with a market capitalization of $20.78 billion and dominance of 0.72%. The recent decline reflects broader cryptocurrency market pressures, including high-volume selling across major assets. Volume currently remains slightly below its 30-day average, suggesting moderation in trading activity compared with prior weeks.

A sustained drop below $0.14 could trigger a cascading decline for Dogecoin (DOGE), opening the door toward the $0.07 level. Source: Ali Martinez via X

Ali (@ali_charts), a technical analyst specializing in cryptocurrency pattern analysis, noted that “a sustained weekly close below $0.14 could open the path toward the $0.07 macro support.” Analysts highlight that this downside projection assumes continued selling pressure and a failure to hold higher lows on the weekly chart, while oversold RSI levels below 30 could provide conditions for a potential rebound if the $0.07 support holds.

On the weekly chart, DOGEUSDT has formed a long-term symmetrical triangle since 2021, defined by declining swing highs and progressively higher lows. Observations include:

Price is retesting the triangle’s rising support line, measured from 2021 swing lows.

Trading volume has gradually contracted over recent months, consistent with consolidation phases.

The structure has maintained higher lows, suggesting ongoing accumulation rather than immediate breakdown.

Price Prediction: Consolidation Below alt=")

DOGE/USDT is trading within a long-term triangle, testing rising support, with a breakout or downside retest possible. Source: sika0409 on TradingView

Market participants note that if DOGE breaks out above the triangle apex with confirming volume, a sharp upward move could follow. Conversely, failure to hold the lower support line could validate a decline toward macro support near $0.07.

On daily charts, Dogecoin is currently oscillating between $0.1300 and $0.1350, forming a potential accumulation base.

Technical patterns suggest a bearish accumulation scenario in the near term, while resistance levels around $0.1500–$0.1550 remain key for any upside momentum. In the worst-case scenario, DOGE could retest the $0.0900–$0.0950 range on a monthly scale, though a break above $0.1800 would indicate a recovery trend is forming.

Cantonese Cat (@cantonmeow), known for providing long-term trend analysis using Ichimoku and Fibonacci models, notes that on the monthly Ichimoku model, DOGE is approaching the lower boundary near $0.04—a level historically aligned with multi-year dynamic support.

On the monthly chart, DOGE is currently testing the lower edge of the Ichimoku cloud—a key zone for long‑term support and momentum confirmation. Source: Cantonese Cat via X

Analysts also highlight the 0.5 logarithmic Fibonacci retracement and 200-week simple moving averages (SMAs) as additional long-term supports that could underpin rebounds toward $0.133 if broader market conditions improve. Cantonese Cat added a characteristically light remark—“Dog’s still in the house”—while emphasizing that DOGE remains within long-term structural support.

Analysts suggest the next potential resistance for DOGE could appear around $0.2000, provided critical support above $0.1500 holds.

On the downside, a sustained weekly close below $0.14 could open the path toward $0.07, contingent on volume expansion and confirmation below multi-year trendlines. Investors are advised to monitor consolidation patterns, trading volumes, and broader macro conditions, as these factors heavily influence the likelihood of both bullish and bearish outcomes.

Dogecoin remains in a cautious consolidation phase, with technical and historical support zones defining key thresholds.

Dogecoin was trading at around 0.14, down 6.48% in the last 24 hours at press time. Source: Brave New Coin

While upside targets of $0.18–$0.20 are possible, they remain dependent on a confirmed breakout and market momentum. Conversely, failure to hold support could lead to testing lower macro levels. Traders and long-term investors should consider both scenarios while accounting for volume, volatility, and historical pattern behavior.

The cryptocurrency sector is undergoing a significant transformation as

Dogecoin

(DOGE) experiences declining interest, prompting investors to shift their focus to up-and-coming ventures like Mutuum Finance (MUTM). This decentralized finance (DeFi) platform is gaining traction amid the evolving market landscape. Despite 21Shares introducing a leveraged Dogecoin ETF, overall market sentiment indicates that both retail and institutional investors are increasingly seeking out newer, high-potential projects.

The 21Shares 2x Long Dogecoin ETF (TXXD), which debuted on NASDAQ on November 20,

allows investors to gain twice the daily returns of DOGE

. This offering

highlights the growing institutional interest in Dogecoin

, especially following collaborations with Tesla and AMC Theatres. Nevertheless, DOGE’s value has

hovered around $0.175

, and experts point out that ambitious bullish targets—such as $1.20—remain out of reach without a decisive upward move.

Mutuum Finance, a DeFi lending protocol, is drawing significant interest in the current market environment.

Over 90% of tokens in Phase 6 have already been allocated

, with more than $18.9 million raised and a community of over 18,200 holders.

The current Phase 6 price of $0.035 per token

marks a 250% rise from its original launch price of $0.01.

Mutuum’s swift momentum is driven by key achievements and strong security protocols.

Halborn Security has started auditing the platform’s smart contracts

, further strengthening trust in its decentralized lending system.

Previously, the project earned a 90/100 score from Token Scan

by CertiK, and a $50,000 bug bounty is motivating security experts to find any weaknesses.

These initiatives are in line with the project’s roadmap

, which features a testnet launch for its V1 protocol in Q4 2025.

The sense of demand around Mutuum is heightened by its fixed-allocation approach.

With just 5% of the total 4 billion MUTM tokens

made available to the public, the project’s scarcity angle has fueled demand. The shrinking supply in the current phase has intensified FOMO, especially as the token nears its $0.06 listing price.

Unlike Mutuum’s methodical expansion,

Dogecoin’s prospects depend on speculative triggers

, such as the possible approval of a spot ETF—a scenario many analysts view as uncertain. Although

21Shares’ leveraged ETF introduces new possibilities

for

DOGE

exposure, the market at large seems to prefer projects that offer real-world utility and robust security.

As the digital asset space continues to develop, Mutuum Finance demonstrates the increase in demand for DeFi platforms that emphasize openness and innovation. With Phase 6 almost finished and Halborn’s audit in progress, the project is positioning itself as a notable contender in the 2025 crypto landscape.

Last Updated:

Matcha is a powdered form of Japanese green tea that has been gaining global

Whether it is K-pop singer BTS’ Kim Taehyung, aka V, going viral for drinking a strawberry matcha latte or Bollywood actor Sanya Malhotra launching her own brand, Bree, matcha has people in a chokehold. In fact, this has even caused a global shortage as the demand for this green tea soars. In 2024, the matcha market was valued at USD 3.66 billion, and it is expected to more than double.

Matcha, a powdered form of Japanese green tea, which has to be carefully grown in special weather conditions, also has various health benefits. It has an enhancing effect on cognitive function, cardiometabolic health, and anti-tumorogenesis. Some studies show that it may help protect the liver, and it is rich in catechins, a type of natural antioxidant. This can help stabilise harmful free radicals, compounds that can damage cells and cause chronic disease.

While everyone seems to be sipping on matcha lattes, Chef Tejasvi Chandela, founder and chef, Dzurt Jaipur, believes in going a step further. She has worked on a dessert menu that includes this tea. “Matcha is one of those ingredients that invites both respect and creativity. I’ve loved using it in ways that challenge the idea of matcha being limited to lattes and beverages. Its earthy profile pairs beautifully with citrus, berries, and even white chocolate, so we explore those combinations in tarts, cookies, lamingtons, and more. Our goal is always to introduce matcha in a way that feels exciting, modern, and accessible for the Indian palate,” she says.

Here are 3 different ways to try matcha, which is a step ahead of the typical beverages:

Matcha Strawberry Tart

A modern interpretation of a classic tart, this dessert pairs a silky ceremonial-grade matcha cream with fresh seasonal strawberries. The tartness of the berries lifts the earthy umami notes of matcha, creating a balanced, clean flavour profile. The idea was to bring a refreshing, bright contrast to matcha, a flavour often seen in warm beverages but rarely showcased in cold-set patisserie.

Matcha Lemon Macaron

The macaron takes the familiarity of matcha and pairs it with a bold citrus edge. The shells are infused with fine Japanese matcha, while the filling is a tart lemon curd cream cheese that cuts beautifully through the richness. This combination was created to highlight how matcha can work in sharper, more playful formats, far beyond the typical creamy pairings.

Matcha Strawberry Lamington

A nostalgic lamington reimagined with a green-tea twist. Soft vanilla sponge is dipped in a matcha glaze, rolled in coconut, and layered with a homemade strawberry compote. It celebrates the meeting of Australian café culture and Asian tea traditions – something you rarely see in Indian patisserie.

November 23, 2025, 11:15 IST

Acquiring insight into the future value of XRPUSD is crucial for investors navigating the unpredictable waters of cryptocurrency. Recent forecasts for XRP hover between conservative predictions of £16 by 2030 to exceedingly daring estimates of £800, rising to heights of nearly £3,850. Intense interest stems from expected institutional adoption and Ripple’s ongoing legal dramas. Currently priced at £1.58, XRPUSD is facing a daily dip of 2.3%. As we explore XRP’s potential, we’ll unpack key market indicators and expert opinions.

When discussing XRP price prediction, analysts provide a wide scope of possibilities. Conservative estimates suggest XRP could reach £16 by 2030, a figure driven largely by Ripple’s firm position in cross-border payment solutions. More optimistic forecasts see the cryptocurrency reaching between £800 and nearly £3,850. Such bullish predictions are fueled by a potential increase in institutional adoption and expected regulatory clarity.

Ripple’s ongoing legal battle against the U.S. Securities and Exchange Commission (SEC) is a significant factor. A favorable outcome could unlock new growth pathways for XRP. Regardless of the eventual legal ruling, Ripple continues to secure partnerships that strengthen its ecosystem, further boosting long-term investor confidence.

A closer look at XRPUSD’s technical indicators reveals a challenging environment. The Relative Strength Index (RSI) stands at 33.77, suggesting oversold conditions. However, an ADX of 36.77 indicates a strong trend presence, despite negative momentum seen through a MACD of -0.14.

Bollinger Bands show price volatility, with the current rate near its lower band. The Awesome Oscillator reflects a bearish short-term outlook. Nevertheless, a growing market interest, marked by an MFI of 22.62, hints at potential shifts. Investors should consider these aspects carefully when evaluating their positions.

Institutional adoption plays a crucial role in XRP’s trajectory. Ripple’s strategic alliances with financial institutions continue to bring credibility and new operational use cases to XRP.

The resolution of Ripple’s legal challenges could be pivotal. If Ripple successfully defends against SEC charges, it may bolster XRP, potentially leading to significant price appreciation. Whether these positive developments will materialize remains speculative, but their impact on XRP’s value is undeniable. This anticipation keeps investor interest intact, aligning with the evident growth in XRPUSD’s long-term potential.

Here’s a closer look at potential future scenarios for XRP in 2030.

The future of XRPUSD involves a complex interplay of legal, industry, and market forces. Predicted values ranging from £16 to over £3,850 demonstrate the wide spectrum of possibilities. Institutional uptake and the pending legal resolution are two critical facets that could drive substantial changes in XRP’s value.

For investors, it’s vital to monitor these developments attentively. Each passing event shapes the market’s predictions and the cryptocurrency landscape as a whole. As always, conducting detailed analysis and staying informed will be key to navigating these waters effectively.

Meyka, an AI-driven platform, offers real-time financial insights and predictive analytics to assist investors in making informed decisions amidst such volatility.

As of now, XRPUSD trades at £1.58. It experienced a daily decline of 2.3% but remains up 295% year-over-year, reflecting significant volatility and growth potential.

Ripple’s legal battles with the SEC significantly influence XRP’s price. A positive ruling could unlock new growth opportunities, while a negative outcome might hinder its market expansion.

Long-term predictions for XRP vary widely, from £16 to upwards of £3,850 by 2030. These estimates account for potential institutional adoption and legal outcomes affecting its usage and demand.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes.

Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

The Hamster Kombat Daily Cipher continues to rise as one of the most engaging and fast-expanding play-to-earn (P2E) events across the Telegram gaming landscape. As millions of Web3 gaming enthusiasts look for new ways to earn tokens without traditional financial investment, Hamster Kombat has carved out a substantial space with its innovative mix of classic code-breaking and real-time crypto rewards. Every day, thousands of players flock to the Telegram-based ecosystem to decode Morse-like puzzles and earn $HMSTR, the game’s native token, strengthening the game’s role within the rapidly developing world of Web3 entertainment.

Today, the focus shifts to the Hamster Kombat Daily Cipher for November 23, 2025—a much-anticipated event where players decode the day’s secret sequence, submit their answer, and claim instant rewards. Below, we take an in-depth look at how the Daily Cipher works, why it has become a cornerstone of the Hamster Kombat experience, and how players can maximize their earnings inside the expanding $HMSTR ecosystem.

The Hamster Kombat Daily Cipher, commonly referred to simply as the “Daily Cipher,” is a 24-hour decoding event where players must translate a Morse-style sequence composed of dots and dashes. Once successfully decoded, the sequence reveals a word or phrase that players input to receive rewards.

Unlike traditional mobile games that rely on complicated mechanics or heavy in-app purchases, the Daily Cipher focuses on simplicity and universal accessibility. Anyone with a Telegram account can join instantly. The challenge is designed to blend nostalgia—through the Morse code concept—with digital interactivity, creating a bridge between historical cryptographic gameplay and modern tokenized reward systems.

Also, read this article: Dropee Question of the Day 21 November 2025 to discover more exciting tasks and rewards for challenges!

Each correct answer grants players bonus coins, which can then be used for:

Level upgrades

In-game enhancements

Mining accelerators

Additional reward paths

The Daily Cipher stands as one of the most unique elements of Hamster Kombat because it merges puzzle-solving with token accumulation, turning daily participation into a rewarding habit.

Hamster Kombat’s success lies in its fusion of three powerful factors: accessibility, gamified economics, and Telegram integration. While many Web3 games struggle to attract audiences due to complex onboarding processes, Hamster Kombat makes entry effortless.

Telegram serves as both the gaming platform and the crypto wallet interface. No external apps or login credentials are required, giving the game instant reach to millions of users worldwide.

Players can earn, hold, mine, and spend $HMSTR tokens automatically. By merging gaming and wallet systems into a single interface, Hamster Kombat eliminates barriers that commonly discourage new crypto users.

Unlike Web3 games that require intensive grinding or high-stakes competitive play, Hamster Kombat keeps gameplay simple, consistent, and enjoyable.

Puzzles can be solved by anyone, regardless of age or background. The challenge feels timeless yet modern, allowing Hamster Kombat to attract not just gamers but puzzle enthusiasts and crypto learners.

With this foundation, the Daily Cipher has become a daily ritual for many players—and a key driver behind Hamster Kombat’s viral growth.

Status: Coming Soon – Stay Tuned for the Full Cipher Update

As of this publication, the official Morse-code sequence for November 23, 2025 has not yet been released. Once verified, the updated Cipher and correct answer will be published immediately on hokanews.

Players are encouraged to check back frequently, as Cipher releases typically occur without prior announcement to ensure fairness across global time zones.

The Daily Cipher process is structured into three key steps: activation, decoding, and claiming rewards. Below is a clear breakdown of the correct procedure for beginners and seasoned players alike.

To begin the day’s decoding challenge:

Open your Telegram app.

Navigate to the Hamster Kombat bot or interface.

Find the Cipher icon—a symbol that players will recognize once familiar with the interface.

Tap the icon to activate Cipher mode.

A red screen will appear, confirming that the Cipher challenge has officially begun.

This activation enables the game to register your decoding attempts and reward claims correctly.

Morse-style decoding is at the heart of the Daily Cipher experience. Here’s how it works:

A short tap represents a dot (●).

A long press represents a dash (▬).

A 1.5-second pause separates characters.

Players must carefully observe the sequence displayed on their screen and replicate the timing accurately. The key is consistency—incorrect timing can change the meaning of the decoded message.

Success requires focus, precision, and occasionally reattempts, which is part of the challenge’s appeal.

Once the message has been decoded:

Type the correct word or phrase into the answer field.

Submit your answer.

Upon verification, your account will instantly receive the associated bonus coins.

The entire process takes only a few minutes, but for many players, the reward feels substantial—especially when combined with other daily activities that boost earnings.

Beyond the Daily Cipher, Hamster Kombat offers multiple earning pathways that help players expand their token balance efficiently. Here are the most effective strategies:

Daily missions are among the highest-yielding opportunities within the game. These tasks refresh every 24 hours and often provide multiple layers of rewards, encouraging regular logins.

Weekly or seasonal events can yield even larger bonuses, making them essential for rapid progression.

The Toxin Challenge is a high-reward event where participants have the opportunity to earn up to 1 million coins. Despite its difficulty, the reward makes this challenge one of the most sought-after activities within the ecosystem.

Hamster Kombat includes a range of mini-games and elite missions that offer additional rewards for skilled gameplay. These features provide variety and entertainment while also contributing to the player’s coin balance.

Hamster Kombat rewards consistency. Logging in daily, participating in multiple events, and engaging with various in-game features all contribute to long-term token growth.

The Daily Cipher blends puzzle-solving, crypto mining, and instant rewards in a way that appeals to both traditional gamers and crypto newcomers. It serves three critical roles within the Hamster Kombat ecosystem:

Players return daily to crack the Cipher, building habit-forming engagement patterns.

The Cipher ensures that tokens circulate fairly among active, committed users.

Players unknowingly practice timing, pattern recognition, and basic cryptography—skills foundational to blockchain literacy.

This combination positions Hamster Kombat ahead of many other P2E titles that rely solely on tapping or grinding without deeper interaction.

The Hamster Kombat Daily Cipher for November 23, 2025 continues to capture attention across the P2E landscape. As one of the most innovative features in the game, the Daily Cipher merges classic code-breaking mechanics with modern token incentives, empowering players to earn $HMSTR tokens with nothing more than their skill, focus, and a Telegram account.

Whether you’re a seasoned crypto gamer or a newcomer exploring Web3 experiences for the first time, Hamster Kombat provides an accessible, rewarding, and dynamic ecosystem.

Daily decoding, mining, missions, and events form the core of the game’s appeal—and checking hokanews for the latest Cipher updates ensures you never miss an opportunity to earn.

hokanews.com – Not Just Crypto News. It’s Crypto Culture.

Writer

@Erlin

Erlin is an experienced crypto writer who loves to explore the intersection of blockchain technology and financial markets. She regularly provides insights into the latest trends and innovations in the digital currency space.

Check out other news and articles on Google News

As Bitcoin (BTC USD) traded near $83,900, the market witnessed numerous price prediction observations from analysts and market watchers.

On November 21, the price briefly touched $80,000 on derivatives exchange Hyperliquid before stabilizing in the low-$80,000 range.

This triggering widespread liquidations across cryptocurrency markets. At the time of writing the leading crypto was trading at

Analyst Stacy Muur aggregated predictions from five market observers on November 21, presenting a range of potential local bottom targets.

The forecasts spanned from $75,000 to $94,500, with varying methodologies and timeframes for Bitcoin price support levels.

Chris Burniske of Placeholder VC identified $75,000 or lower as a re-entry level rather than a formal bottom call.

On October 17, Burniske stated he took profits after the sharp October crash, noting “cracks” in the monthly charts for Bitcoin and Ethereum.

He indicated he would watch Bitcoin’s reaction to $100,000 but would only consider buying again when Bitcoin reached $75,000 or lower, framing this as part of a gradual de-risking strategy.

Arthur Hayes of BitMEX projected a near-term target of $80,000 to $85,000, followed by $200,000 to $250,000 by year-end.

In his November 17 essay “Snow Forecast,” Hayes argued that Bitcoin’s drop from approximately $125,000 to the $90,000 area, while US equity indices remained near highs, signaled a looming credit event.

According to his Bitcoin price prediction, it could fall to roughly $80,000-$85,000 during a “soft period” before Federal Reserve or Treasury money-printing schemes could drive prices to $200,000-$250,000.

Chinese analyst Ban Mu Xia forecast a first stop at $94,500, with an ultimate bottom near $84,000.

His view is of a “complex sideways adjustment,” in which Bitcoin first dipped to around $94,500, then entered an oscillation that could rebound above $116,000 before forming an ultimate bottom near $84,000, potentially 6-8% lower at extremes.

JPMorgan analysts, led by Nikolaos Panigirtzoglou, discussed the forced selling risk related to a potential removal of MicroStrategy from the index, rather than publishing a specific Bitcoin price target.

The bank estimated that roughly $2.8 billion in passive flows could be forced to sell MicroStrategy stock if MSCI removed the company from major equity benchmarks, with as much as $8.8 billion at risk if other index providers followed suit.

The $75,000-$80,000 range corresponded to common technical support zones identified in this analysis.

CoinShares’ James Butterfill focused on flow data and cycle behavior rather than numeric bottom predictions.

In Bloomberg coverage, Butterfill stated crypto suffered “heavy selling by whales who follow the four-year cycle narrative.”

He noted CoinShares data showed large holders sold more than $20 billion in crypto since September, calling the pattern “somewhat self-fulfilling” even though CoinShares did not fundamentally endorse the four-year-cycle thesis.

Coinglass data showed $2.2 billion in positions liquidated in the crypto market over the past 24 hours, as of press time.

Bitcoin USD accounted for approximately $1 billion of total liquidations, with long positions representing $887 million. Roughly 391,000 traders faced liquidations across exchanges.

The cascade of forced selling created a feedback loop that accelerated downward price pressure as leveraged traders were forced to close positions.

The total cryptocurrency market capitalization dipped below $3 trillion for the first time since April 2025, currently at $2.96 trillion, down 7.5% over the past 24 hours.

US-listed spot Bitcoin ETFs recorded approximately $3.79 billion in net outflows during November, the largest monthly outflow since the products launched in January 2024.

Open interest in Bitcoin perpetual futures fell 35% from October’s peak near $94 billion, reducing liquidity across derivatives markets.

The combination of reduced open interest, extreme fear sentiment, and massive liquidations created conditions where relatively small sell orders moved the Bitcoin price significantly.

It remains to be seen whether the current range will provide support for a bounce or if Bitcoin is preparing for a move into a bearish period.

The post Will Bitcoin (BTC USD) Price Slump To $75,000? appeared first on The Coin Republic.

The crypto market has been hit by a sharp sell-off, with memecoins plunging to their lowest valuation in 2025. This widespread panic, wiping out over $5 billion in a single day, has created a climate of “Extreme Fear.”

As investors re-evaluate the Dogecoin price prediction, the focus is shifting to high-utility, early-stage projects like DeepSnitch AI. Its presale has already surged past $565,000, with the token price at $0.02429.

The memecoin sector suffered a brutal sell-off, dropping to a combined market capitalization of $39.4 billion, according to CoinMarketCap. This marks the lowest point for the sector in 2025. In just 24 hours, over $5 billion was wiped out, a sharp reversal from the year’s peak of $116.7 billion in January. This 66.2% drawdown highlights the extreme volatility of the sector.

The crash mirrored a broader decline across the entire digital asset market. CoinGecko data shows the total crypto market cap fell from $3.77 trillion on November 1 to $2.96 trillion, wiping out $800 billion in just three weeks. Traders are pulling back from speculative assets across the board, including NFTs, as market sentiment turns fearful.

The current market fear is a massive opportunity. With the Fed easing policy and ETF demand providing a backstop for major coins, this dip is the perfect entry for “high-beta” assets.

DeepSnitch AI could be the best option. It’s an audited, stakable presale that is still priced at the ground floor. This is a “picks-and-shovels” chance for the $1.5 trillion AI gold rush that Gartner projects for 2025.

It is building AI agents, including SnitchFeed, which is your 24/7 market radar, filtering noise to give you clear signals on whale movements. Others, like SnitchScan, are your personal security guard, digging into smart contracts to find rug-pull code before you invest.

While established coins like the Dogecoin price prediction struggle with their massive market caps, DeepSnitch AI offers asymmetric upside and the potential for exponential gains from a low base.

The Dogecoin forecast 2026 is currently clouded by the intense market sell-off. The token has dropped 12% in the last seven days, underperforming the broader market. The Fear & Greed Index is at 14, and the sentiment is bearish. The token is trading below its key 50-day and 200-day moving averages, confirming the downtrend.

Despite this, the long-term picture isn’t entirely bleak. The Dogecoin price prediction suggests a mild 5% recovery by mid-2026. However, without a major catalyst like new Elon Musk Dogecoin updates, the projections are average.

In a sea of red, Aster (ASTER) has been a remarkable outlier, surging 12% in the last week while the rest of the market collapsed. This incredible relative strength shows strong, independent buying interest.

However, the sentiment remains bearish, and the Fear & Greed Index is also at 14. The technical outlook is incredibly bullish, forecasting a potential 120% rise by late 2026. This suggests that while the market is fearful, investors see long-term value.

The $5 billion memecoin wipeout is a painful but necessary reset. It clears out the froth and creates an entry point for smart money.

While Dogecoin price prediction faces a slow recovery, DeepSnitch AI offers the high-growth potential of an early-stage AI utility project. With over $565k raised and a clear “picks-and-shovels” value proposition, this is the best crypto to buy now for asymmetric returns in the next cycle.

Visit the official DeepSnitch AI website, join the Telegram, and follow on X (Twitter) for the latest updates.

The crash dampens short-term sentiment but doesn’t necessarily destroy the long-term Dogecoin price prediction. But it has limited upside compared to newer, utility projects like DeepSnitch AI.

DeepSnitch AI provides AI tools, like SnitchScan for security and SnitchFeed for market intelligence. Investors need this to navigate the crypto market safely and profitably.

DeepSnitch AI is a “high-beta” bet because it is an early-stage asset in a high-growth sector. It carries more risk than Bitcoin but offers significantly higher potential returns.